Compare UAE free zone and mainland company structures for Canadian businesses, including QFZP eligibility, substance requirements, and 0% tax rules.

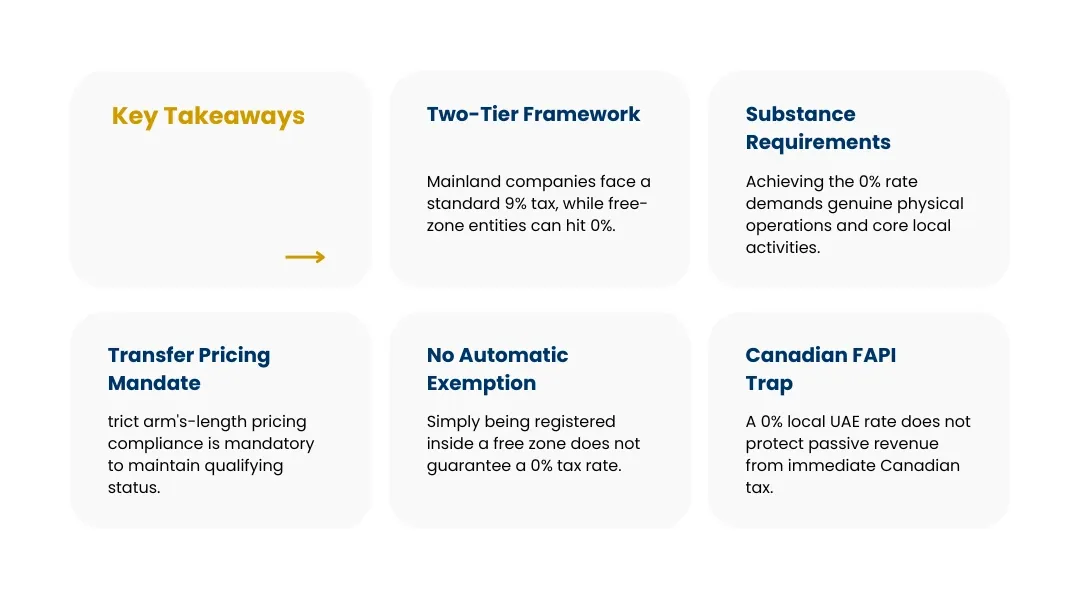

In the UAE, the choice between a free zone and the mainland used to be about ownership and licensing. Now it's also about tax: a Qualifying Free Zone Person can still pay 0%, while the mainland pays 9%. But “qualifying” has real conditions.

Two routes, two tax outcomes

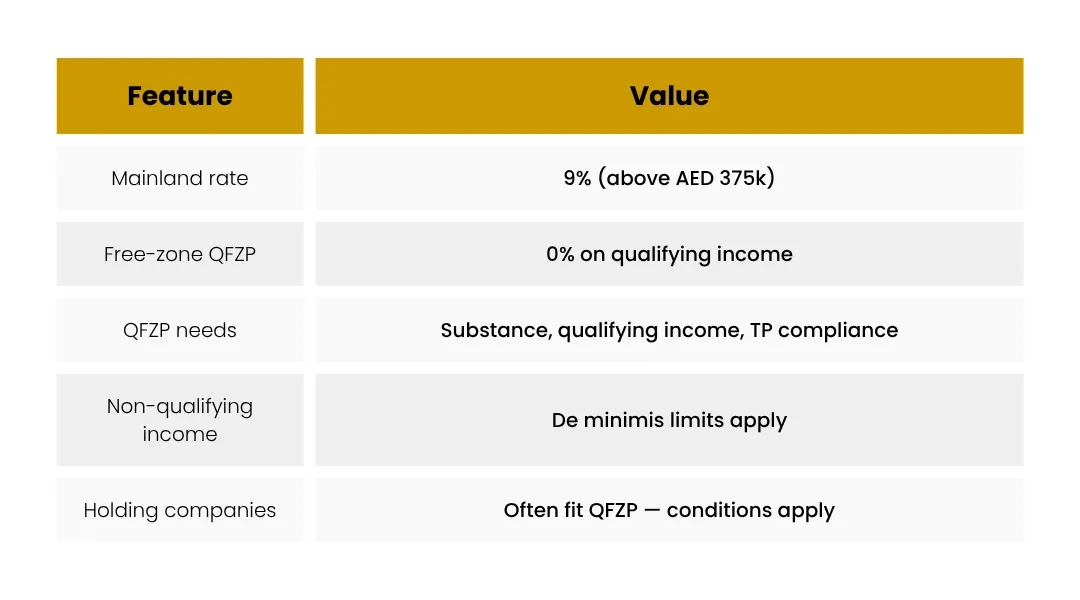

Mainland companies can trade freely across the UAE and are taxed at the standard 9% (above AED 375k). Free-zone companies sit in one of the UAE's many economic zones and can, if they qualify, enjoy 0% on qualifying income - the heart of the UAE's continuing appeal.

What makes a Qualifying Free Zone Person

To get the 0% rate, a free-zone company must be a QFZP, which broadly requires:

- Being a registered free-zone entity with adequate substance in the zone (people, premises, expenditure);

- Earning qualifying income (defined categories - e.g., transactions with other free-zone persons and certain qualifying activities);

- Not electing into the standard regime, and meeting de minimis limits on non-qualifying income; and

- Complying with transfer-pricing and documentation rules.

Fall outside these and the company is taxed at 9% on all its income.

Holding companies in a free zone

A pure holding company in a free zone can often fit the 0% regime - holding shares and receiving qualifying income - but the substance and qualifying-income tests still apply. The detail matters: “free zone” alone does not guarantee 0%.

Choosing for a Canadian group

For most Canadian-owned holding structures, a free-zone QFZP is the natural choice - low local tax plus a clean holding base. If you need to trade directly with the UAE mainland market, weigh the 9% cost against the commercial benefit.

The Canadian angle

A 0% free-zone result is attractive, but remember the Canadian lens: active income (with substance) reaches exempt surplus, while a free-zone company that simply accumulates passive income risks FAPI in Canada regardless of the UAE's 0%. The free-zone status optimises the UAE side; the Canadian active-vs-passive analysis runs in parallel. Design for both.

Frequently asked questions

Can any free-zone company get 0%?

No - only a Qualifying Free Zone Person earning qualifying income and meeting substance, de minimis and transfer-pricing conditions. Non-qualifying free-zone companies are taxed at 9%.

What is “qualifying income”?

Broadly, income from transactions with other free-zone persons and from defined qualifying activities, subject to detailed rules and exclusions. The Federal Tax Authority's guidance governs the categories.

Should a Canadian holdco choose a free zone or mainland?

For pure holding, a free-zone QFZP is usually preferable for the 0% rate. Mainland makes sense if you need to trade directly within the UAE domestic market.

Does free-zone 0% remove the need to file?

No. QFZPs still register for corporate tax and file returns, and must maintain substance and documentation to keep the 0% rate.