Discover how the absence of a Canada, Marshall Islands treaty or TIEA impacts exempt surplus eligibility, taxable surplus, and Canadian tax efficiency.

Every other jurisdiction in this series shares one thing with Canada: a tax treaty or a TIEA. The Marshall Islands doesn't. That gap quietly turns the RMI's biggest selling point - zero tax - into a Canadian tax catch. Here's exactly why.

The rule that does the damage

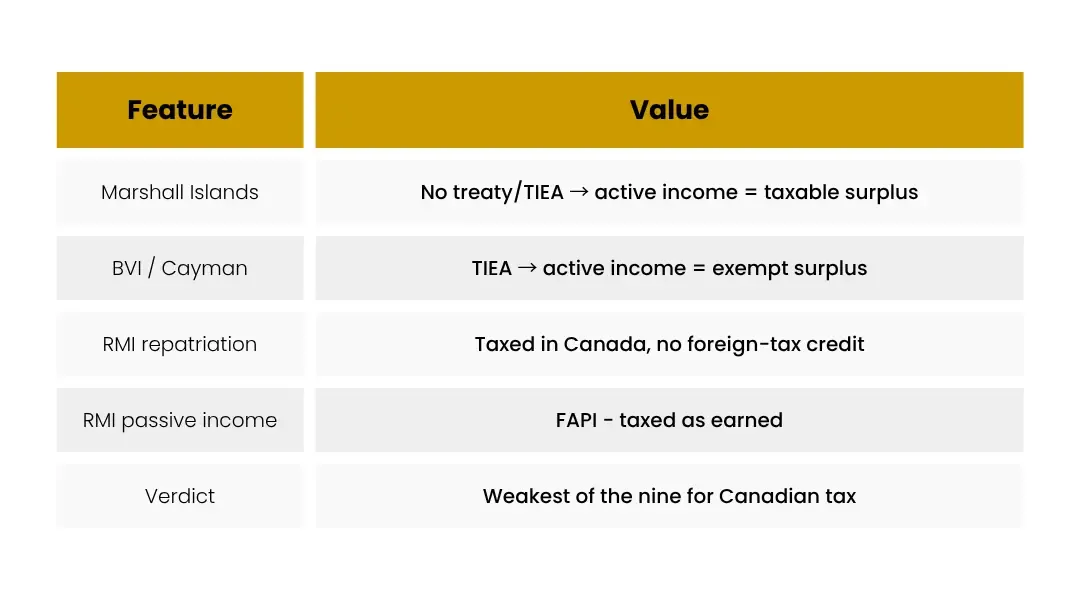

Canada's foreign-affiliate system rewards income earned in a “designated treaty country” - one with which Canada has a treaty or a TIEA. Active business income from such a country flows into exempt surplus and can be repatriated to a Canadian corporate parent tax-free. The Marshall Islands has neither a treaty nor a TIEA with Canada.

What that means in practice

So even genuine active business income earned through a Marshall Islands affiliate lands in taxable surplus. When paid up to the Canadian parent, it's taxed in Canada - and because the RMI charges no tax, there's no foreign-tax credit to soften the blow. You get full Canadian tax on repatriation, with nothing to offset.

Compare that to a TIEA island

This is the crucial contrast with the BVI and Cayman. Those are also zero-tax - but they each have a TIEA with Canada, so active income reaches exempt surplus. The Marshall Islands, lacking a TIEA, can't. Two zero-tax islands, completely different Canadian outcomes - purely because of an agreement one has and the other doesn't.

And passive income is still FAPI

On top of all that, passive income in a controlled RMI affiliate is FAPI - taxed in Canada as it accrues. So neither active nor passive income gets favourable treatment. For a Canadian corporate owner, the RMI is the least tax-efficient of the nine jurisdictions. The honest conclusion: don't use it for Canadian tax efficiency.

The Canadian angle

This is the whole point: a treaty or TIEA - not the local tax rate - is what unlocks exempt surplus. The Marshall Islands has no such agreement with Canada, so its zero tax buys a Canadian corporate owner nothing on repatriation, and FAPI still applies to passive income. If a Canadian group needs offshore neutrality, a TIEA island (BVI/Cayman) or a treaty country is almost always the better choice. Reserve the RMI for genuine maritime needs.

Frequently asked questions

Why does the lack of a TIEA matter so much?

Because exempt-surplus treatment depends on Canada having a treaty or TIEA with the country. Without one, even active business income is taxable surplus - taxed when repatriated, and with no foreign-tax credit where the country charges no tax.

Isn't zero tax always good?

Not for a Canadian owner. Zero foreign tax with no treaty/TIEA means full Canadian tax on repatriation and no credit to offset it. A modest tax in a treaty country can produce a far better after-tax result.

So why does anyone use the Marshall Islands?

Chiefly for commercial reasons - above all, the ship registry - and for non-Canadian-resident owners for whom the Canadian rules don't apply. For Canadian tax purposes, it's rarely the efficient choice.

Could a treaty/TIEA be signed in future?

Possibly, but you should plan on current law. As of June 2026 there is no Canada–RMI treaty or TIEA, so its income does not qualify for exempt surplus.