Learn how Ireland's participation exemption helps Canadian holding companies receive qualifying dividends and sell subsidiary shares with no Irish capital gains tax.

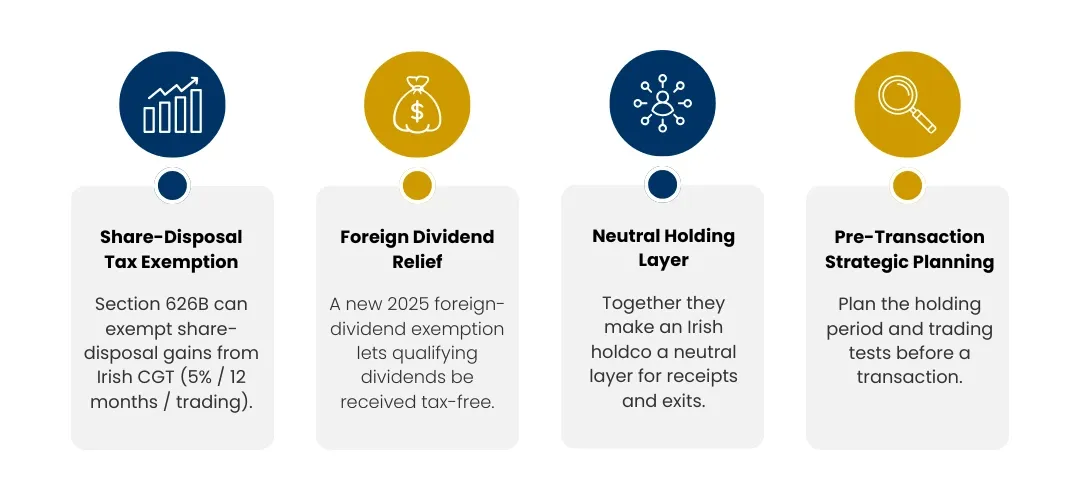

The cleanest reason to put an Irish company at the top of a European group is the exit. Ireland's participation exemption can let your holdco sell a qualifying subsidiary with no Irish capital gains tax - and a new 2025 rule does the same for foreign dividends.

The share-disposal exemption

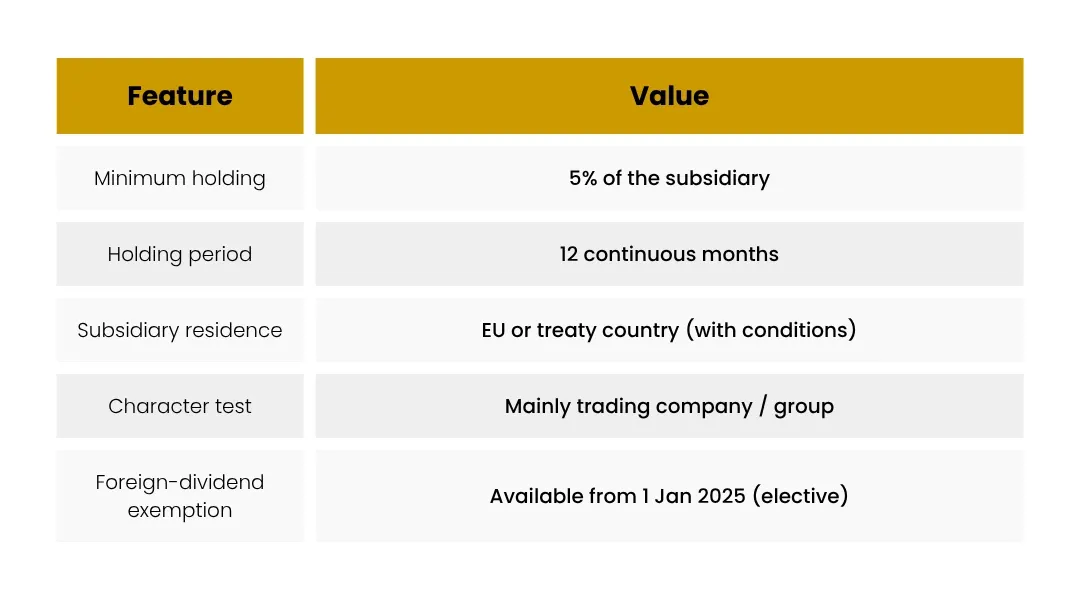

Under Ireland's long-standing participation exemption (section 626B), a gain on the disposal of shares in a subsidiary can be exempt from Irish CGT where the key conditions are met - broadly, the holding company has held at least 5% of the subsidiary for a continuous 12-month period, and the subsidiary is resident in the EU or a treaty country and is mainly a trading company (or part of a trading group).

The new foreign-dividend exemption (2025)

From 1 January 2025, Ireland introduced a participation exemption for foreign dividends. Qualifying distributions from 5%-plus holdings in EU/treaty companies (with the scope extended to certain other jurisdictions) can be received exempt, with an annual election. This simplifies what used to be a credit-based calculation and makes Ireland markedly cleaner as a dividend recipient.

Why this is the holdco's superpower

Together these exemptions mean an Irish holding company can receive profits up from European subsidiaries and sell those subsidiaries without an Irish tax leak at the holdco level. That's exactly what an acquirer or investor wants to see above the operating businesses - a neutral layer that doesn't add tax on the way out.

Conditions are everything

Each exemption has detailed requirements - holding percentage, holding period, residence and trading tests. They reward planning ahead: the 12-month holding clock and the trading character of the target need to be right before the deal, not patched up afterwards.

The Canadian angle

An Irish-level CGT exemption is only half the story for a Canadian owner. The gain on selling the Irish holdco's shares may flow through Canada's hybrid surplus and foreign-affiliate rules, and the cash coming home is taxed based on its surplus pool. The Irish exemption keeps the Irish tax at zero; the Canadian treatment needs its own planning. Design the exit on both sides at once.

Frequently asked questions

Does the exemption cover any subsidiary sale?

No. The subsidiary must generally be EU/treaty-resident and mainly trading, and the 5% / 12-month holding conditions must be met. Investment-only or non-qualifying subsidiaries may not qualify.

What if I've held the shares for less than 12 months?

The 12-month holding can in some cases be met by looking back over a window around the disposal, but timing is critical. Review it before signing anything.

Is the 2025 dividend exemption automatic?

No - it's an annual election that applies to all in-scope distributions for that period. Whether to elect depends on your facts; it's not always the better option versus the credit method.

Will I still pay Canadian tax on the exit?

Possibly. Irish exemption removes Irish tax, but Canadian foreign-affiliate, surplus and (for individuals) other rules still apply. The two systems must be planned together.