Understand Cayman economic substance requirements for Canadian-owned entities, including holding companies, investment structures, reporting obligations, and compliance.

Like the BVI, the Cayman Islands answered international pressure with an Economic Substance Law - and like the BVI, it scales the requirement to what your company actually does. Here's the substance picture by activity type.

Why Cayman has substance rules

To meet OECD and EU standards (and stay off blacklists), Cayman's Economic Substance Law requires entities carrying on a “relevant activity” to demonstrate adequate substance in Cayman - or, for some, to report instead. The relevant activities mirror the global list: fund management, financing and leasing, headquarters, holding-company business, IP, shipping, distribution and service centres, and more.

The spectrum of requirements

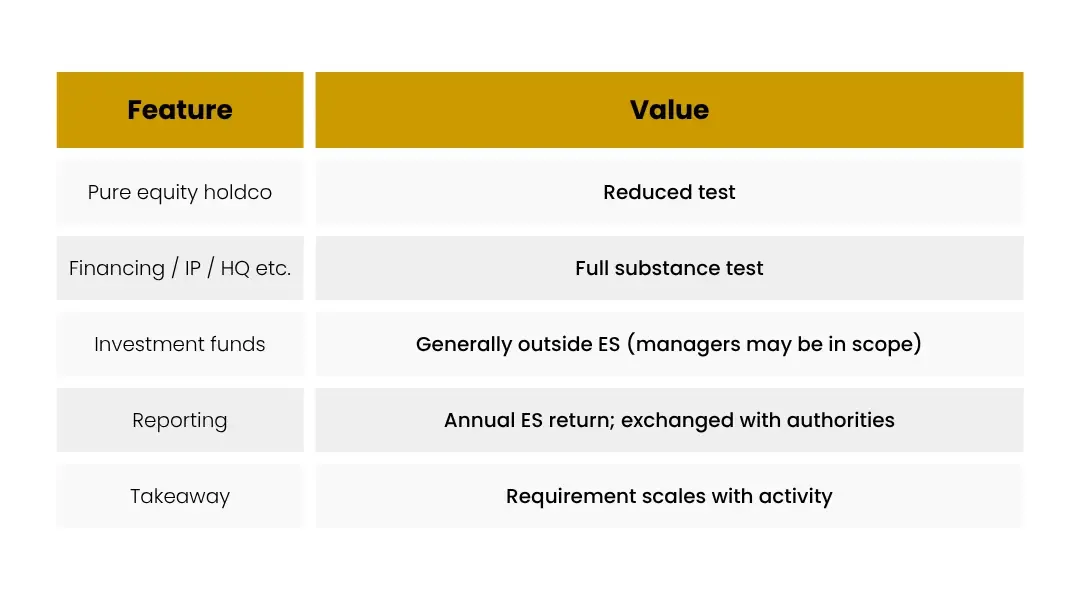

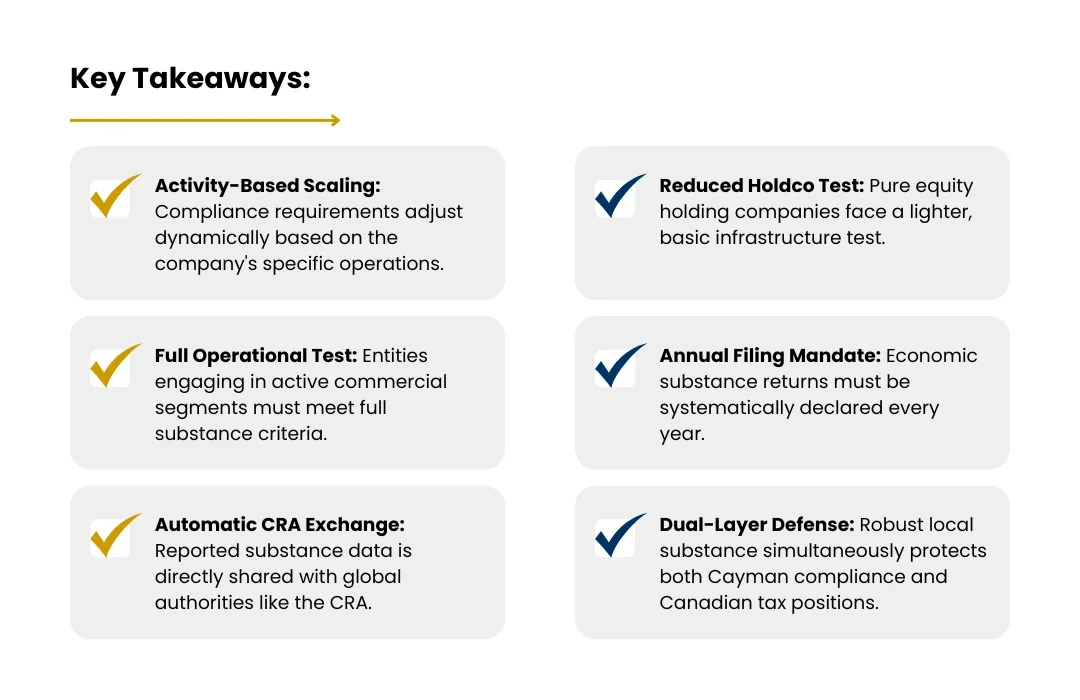

- Pure equity holding companies - a reduced test: comply with Cayman company-law filing obligations and have adequate human resources and premises to hold and manage equity participations.

- Higher-risk activities (e.g., financing, IP) - the full test: core income-generating activities in Cayman, direction and management there, and adequate people, premises and expenditure.

- Investment funds - generally outside the ES regime as “investment funds,” though their managers may be in scope.

Reporting and exchange

In-scope entities file an annual ES return, and substance information can be exchanged with foreign tax authorities, including the CRA. The data you report in Cayman can inform what Canada sees.

The bottom line

Cayman is tax-neutral, not obligation-free. A holding company faces a lighter test, but it's a real one - and any company with active relevant activities must genuinely operate in Cayman to comply. Build accordingly.

The Canadian angle

Cayman ES data is shared with the CRA - and a substance-light Cayman company controlled from Canada is doubly exposed: it may fail Cayman's test and be treated by Canada as resident here (managed and controlled from Canada). For active-business affiliates relying on the TIEA for exempt surplus, genuine Cayman substance is what makes the position defensible on both sides.

Frequently asked questions

Does a Cayman holding company need staff on the islands?

A pure equity-holding company faces a reduced test, often satisfied through its registered office/agent and by meeting filing obligations. Active relevant activities require genuine people, premises and management in Cayman.

Are investment funds caught by the ES Law?

Investment funds are generally treated as outside the relevant-activity regime, but entities providing services to them (such as managers) can be in scope. Each entity is assessed on its role.

Is Cayman substance information shared with Canada?

Yes - under information-exchange frameworks, substance and related data can be shared with foreign tax authorities, including the CRA. Consistency between Cayman and Canadian filings matters.

What if my Cayman company fails the ES test?

Penalties and potential strike-off apply, and information may be exchanged abroad - which can prompt scrutiny in Canada, including of the company's true place of management.