Understand how exempt surplus rules allow active business income earned through a Singapore holding company to be repatriated tax efficiently to Canada.

"Exempt surplus" is the most important phrase in Canadian international tax that almost no founder has heard of. Get it right and your foreign profits come home tax-free. Get it wrong and the same dollars get taxed twice. Here's the plain-English version.

How Canada sorts foreign profits

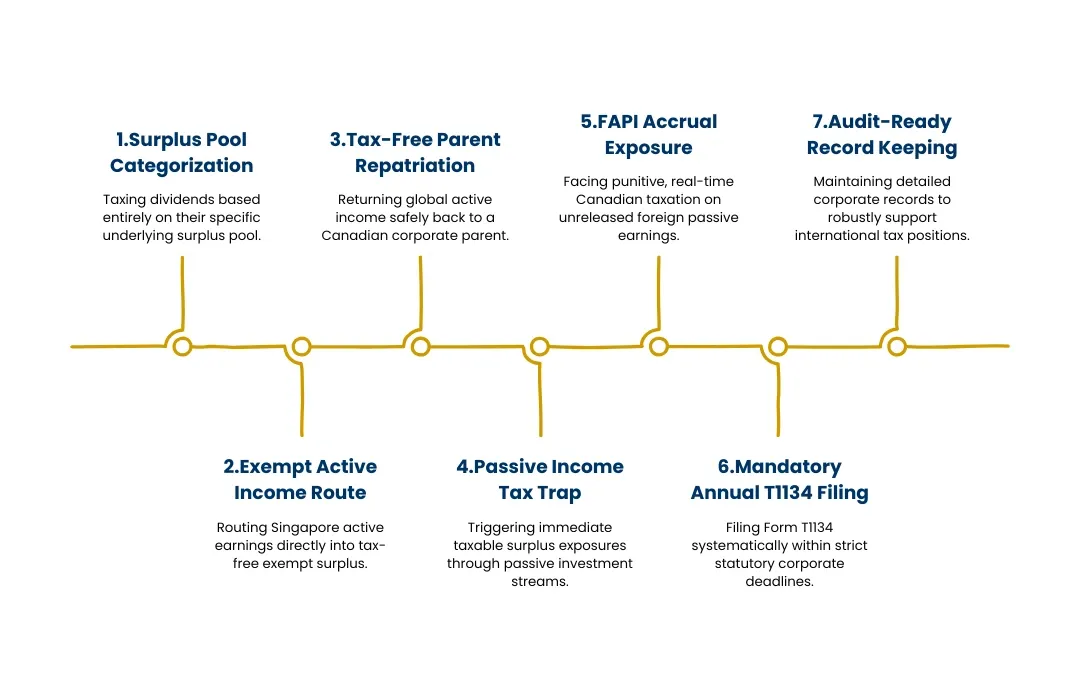

When a Canadian corporation owns a foreign company, Canada doesn't tax the foreign profits as they're earned (with one big exception - FAPI, below). Instead it sorts the foreign company's after-tax earnings into "surplus pools." How a dividend is taxed back in Canada depends entirely on which pool it comes from.

The three pools that matter

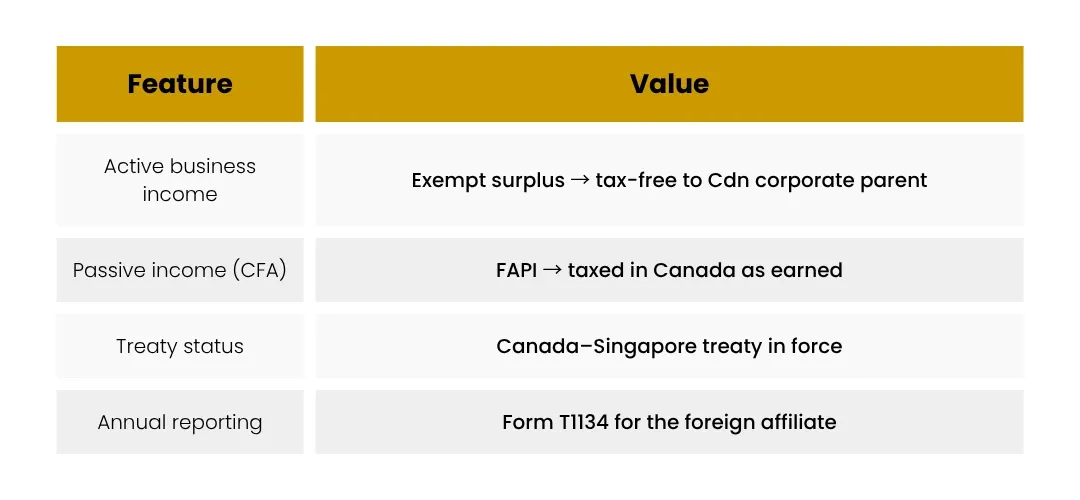

- Exempt surplus - active business income earned in a country Canada has a tax treaty or TIEA with. Dividends from this pool are received by a Canadian corporate parent effectively tax-free (via an offsetting deduction).

Taxable surplus - generally passive income, or active income from a non-treaty/non-TIEA country. Taxed in Canada when paid up, with credit for foreign tax already paid.

Hybrid surplus - mainly certain capital gains, with its own rules.

Singapore is the headline act because Canada has a tax treaty with Singapore. That single fact lets active business income earned through a Singapore foreign affiliate flow into exempt surplus.

The catch: "active" is doing all the work

Exempt surplus is reserved for active business income. If your Singapore company simply holds investments and collects passive income - portfolio dividends, interest, royalties, rents - two problems appear:

That income generally lands in taxable surplus, not exempt surplus, even though Singapore is a treaty country; and

If the company is a controlled foreign affiliate, the passive income is likely FAPI (foreign accrual property income) - taxed in Canada as it's earned, before any dividend is paid.

A Singapore holdco running a real regional business is powerful; one that just parks an investment portfolio usually isn't worth the cost.

Don't forget the paperwork

Owning a foreign affiliate triggers Form T1134 reporting in Canada each year. It's an information return, not a tax bill - but missing it carries real penalties. Exempt surplus is a benefit you claim correctly, with records, not something that happens automatically.

Why this beats a zero-tax island

Founders often assume a 0% jurisdiction is the holy grail. But a zero-tax country with no treaty and no TIEA produces taxable surplus - taxed on the way home - with no foreign tax credit to offset it (because no foreign tax was paid). A 17% treaty country like Singapore, earning active income, can deliver a better after-tax result to a Canadian parent than a 0% island. Treaty status often beats a low rate.

Frequently asked questions

Does exempt surplus mean I pay no tax at all, ever?

It means the dividend to your Canadian corporation is effectively tax-free. Personal tax still applies later when you take money out of your Canadian company as salary or dividends. It removes a layer of tax - it doesn't make money tax-free in your hands.

What's the difference between a treaty and a TIEA?

Both let active business income reach exempt surplus. A full tax treaty also reduces withholding taxes and allocates taxing rights; a TIEA is narrower but still earns "designated treaty country" status for surplus purposes. Singapore has a full treaty.

Do I get exempt surplus if I own the Singapore company personally?

No. The exempt-surplus deduction is for dividends received by a corporation. Personal ownership is taxed differently and usually less efficiently for active foreign business income.

Is interest my Singapore company earns active or passive?

Usually passive - and therefore FAPI if the company is a controlled foreign affiliate. Limited exceptions exist (e.g., interest from the active business of a related affiliate). Get it reviewed before relying on it.