Learn how the Dutch participation exemption allows qualifying dividends and capital gains to flow through a Netherlands holding company with reduced tax exposure.

If you ask European tax advisors which holding-company regime is the benchmark, many will say the Dutch participation exemption. It's the feature that made the Netherlands a holding hub for a century - and it still does the heavy lifting.

What the exemption does

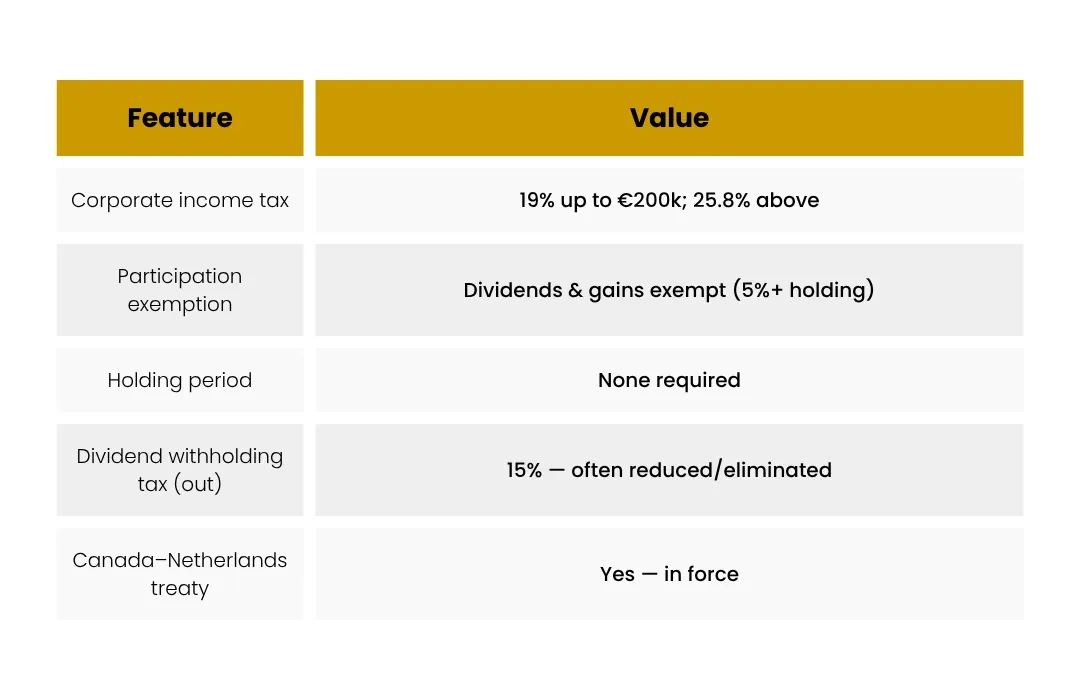

The Dutch participation exemption (deelnemingsvrijstelling) makes both dividends and capital gains from a qualifying shareholding fully exempt from Dutch corporate tax. No tax on dividends received from the subsidiary; no tax on the gain when you sell it. For a holding company, that's the whole game.

When it applies

Broadly, you need a shareholding of at least 5% in the subsidiary, and the participation must not be a passive, low-taxed portfolio investment (the regime has “motive,” “asset” and “subject-to-tax” tests to screen those out). Meet the conditions and the income is simply outside the Dutch tax base.

Why advisors call it the gold standard

- It covers both dividends and gains - many regimes cover only one.

There's no holding-period requirement like some countries impose.

It's well-established and predictable, with decades of guidance behind it.

It pairs with the EU directives and a vast treaty network.

The headline rate is almost beside the point

The Dutch corporate rate (19% up to €200,000, 25.8% above) rarely touches a pure holding company, because the participation exemption removes its main income from charge. The Netherlands competes on the exemption, not the rate.

The Canadian angle

The Netherlands is a treaty country with Canada, so active income through a Dutch foreign affiliate reaches exempt surplus for a Canadian corporate parent. The Dutch exemption keeps tax off dividends and gains inside the Netherlands; the treaty handles the trip home. As always, passive income risks FAPI in Canada, and the affiliate needs annual T1134 reporting.

Frequently asked questions

Does the exemption apply to any 5% shareholding?

Not automatically. The participation must clear the motive, asset and subject-to-tax tests designed to exclude low-taxed passive portfolio holdings. Active operating subsidiaries typically qualify.

Is there a minimum holding period?

No - unlike some countries, the Netherlands does not impose a fixed holding period for the participation exemption, though anti-abuse rules still apply.

What corporate tax will my Dutch holdco actually pay?

Often very little, because its main income (qualifying dividends and gains) is exempt. Tax may arise on non-exempt income such as certain service fees or interest.

Is the Netherlands still a credible choice after the crackdowns?

Yes. It tightened conduit and anti-abuse rules, but the participation exemption itself remains intact and widely used for genuine holding structures.