Explore how a Marshall Islands holding company works, where it is commonly used, and the key Canadian tax considerations business owners should know.

The Marshall Islands is one of the world's quietest offshore hubs - light-touch, low-cost, and famous mainly to the shipping industry. For a Canadian owner it can be useful in narrow situations, but it carries one caveat that changes everything. Let's start with the basics.

What it is

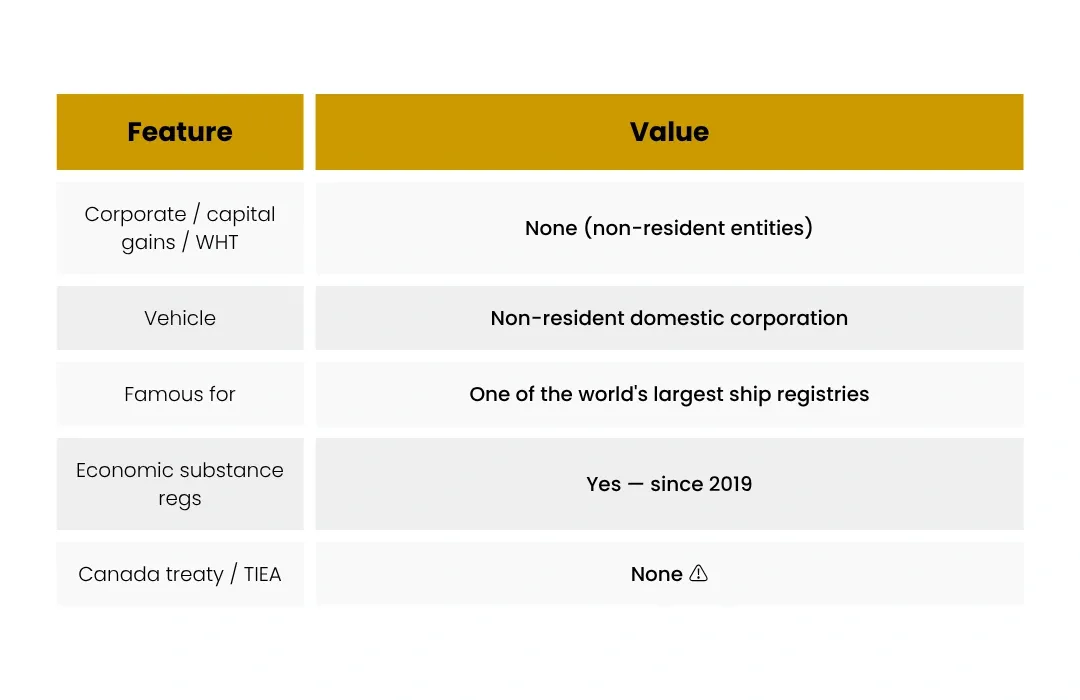

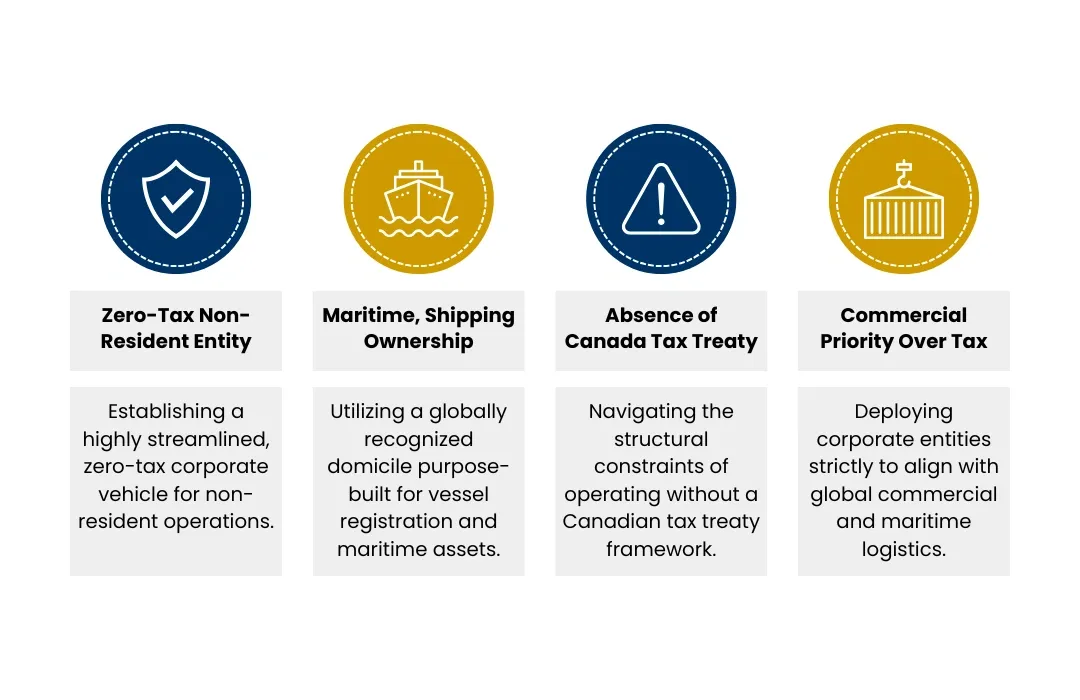

The Republic of the Marshall Islands (RMI) offers a non-resident domestic corporation - a flexible, zero-tax international business vehicle based on US-influenced corporate law. There's no corporate income tax, no capital gains tax and no withholding tax on non-resident entities, fast formation, and minimal local filing. It's a genuinely light-touch regime.

Where it's traditionally used

The RMI's natural home is shipping and maritime: it runs one of the world's largest ship registries, and maritime owners have incorporated there for decades. Beyond shipping, it's used for asset holding and as a neutral, low-cost corporate vehicle in international structures.

The caveat that defines it for Canadians

Here's what sets the Marshall Islands apart from the other eight jurisdictions in this series: Canada has no tax treaty and no TIEA with the Marshall Islands. That single fact removes the “exempt surplus” advantage that makes treaty and TIEA jurisdictions attractive. We devote a whole article to it - because for a Canadian corporate owner, it's the deciding factor.

So when does it make sense?

Mostly when the commercial reason dominates - above all, flagging and owning vessels through the RMI registry - rather than when you're chasing a Canadian tax benefit. As a pure tax play for a Canadian group, it's usually the weakest of the nine. As a maritime tool, it's world-class.

The Canadian angle

Read this before anything else: because there is no Canada–RMI treaty or TIEA, active business income of a Marshall Islands affiliate goes into taxable surplus, not exempt surplus - so it's taxed in Canada when repatriated, with no foreign-tax credit (the RMI charges nothing). Passive income is FAPI. For a Canadian owner, the RMI's zero tax offers no repatriation advantage. Its value is commercial (shipping), not fiscal.

Frequently asked questions

Is a Marshall Islands company legitimate?

Yes - it's a long-established, widely used corporate vehicle, especially in shipping. Legitimacy isn't the issue; the issue for Canadians is that the lack of a treaty/TIEA removes the tax efficiency that other jurisdictions offer.

Why is it so popular in shipping?

The RMI runs one of the largest, most respected ship registries in the world, with quality standards recognised internationally. Owning vessels through an RMI corporation aligns the company with the flag.

Does the RMI really charge no tax?

Non-resident entities are not subject to RMI corporate income, capital gains or withholding tax. But for a Canadian owner, Canadian tax applies - and without a treaty/TIEA, less efficiently than elsewhere.

When should a Canadian avoid the RMI?

When the goal is tax-efficient repatriation of active business income. Without a treaty/TIEA, a treaty country (Singapore, Hong Kong, Ireland, etc.) will almost always serve a Canadian corporate group better.