Learn how Ireland taxes trading and passive income differently, and what Canadian companies need to know about corporate tax, exempt surplus, and FAPI rules.

Everyone quotes Ireland's 12.5% corporate tax rate. Far fewer know it only applies to one kind of income. Get the trading-versus-passive distinction wrong and your “12.5% company” can quietly be a 25% company.

Two rates, not one

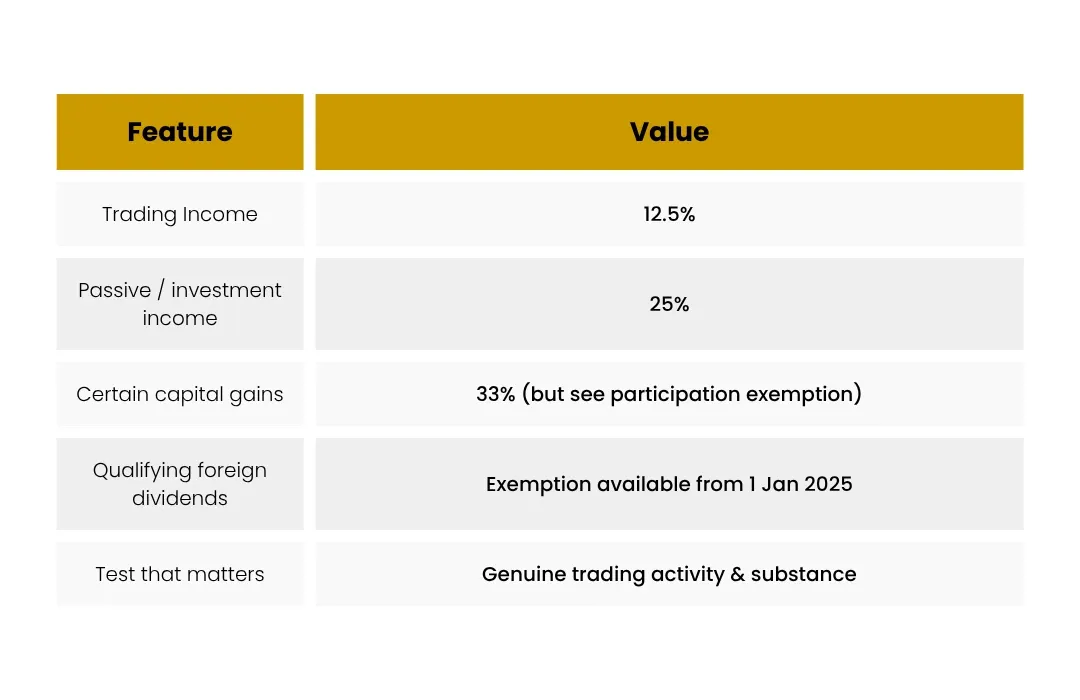

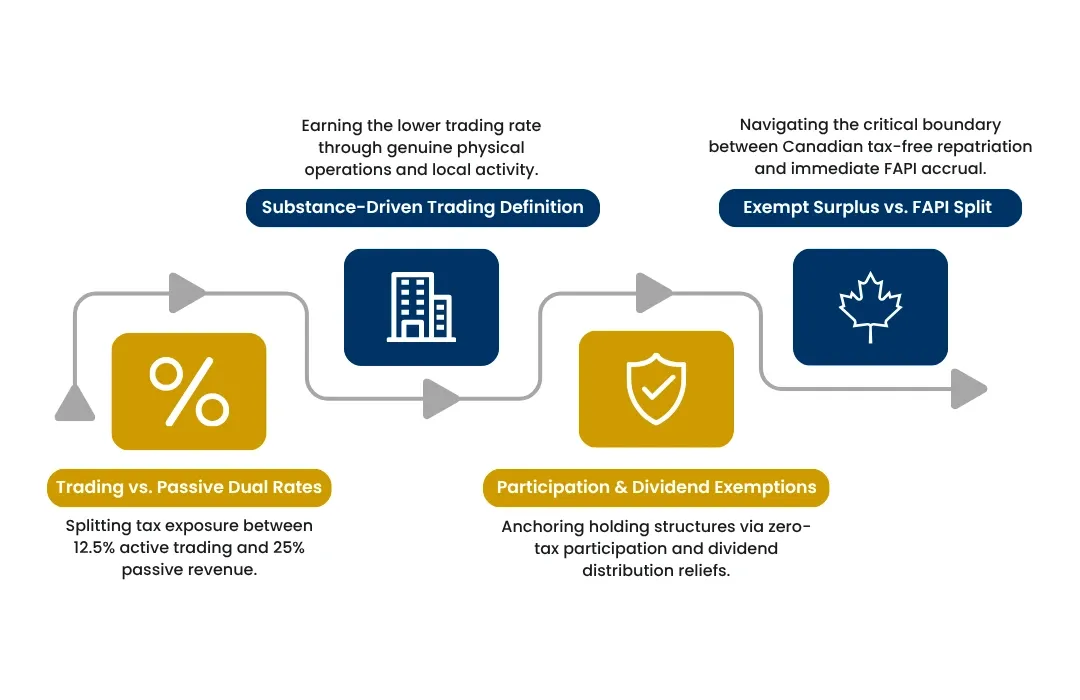

Ireland has two main corporate rates: 12.5% on the trading income of an active business carried on in Ireland, and 25% on passive or investment income - interest, rents, royalties not connected to a trade, and most foreign dividends historically. A third 33% rate applies to certain capital gains.

What counts as “trading”?

“Trading” means an active business with genuine commercial activity - people making decisions, adding value, and bearing risk in Ireland. A company that merely holds assets and collects passive returns is not trading, no matter how it's labelled. Irish Revenue looks at the substance of the activity, not the wording in the accounts.

Why this matters for a holdco

A pure holding company often earns passive income, so the 12.5% headline may not apply to it directly. The good news is that Ireland's participation exemption (see our dedicated article) and the new foreign-dividend exemption from 1 January 2025 can take qualifying dividends and share-sale gains out of charge entirely - which is usually better than worrying about 12.5% versus 25%.

The honest takeaway

Don't buy the “12.5%” line without asking which income it applies to. For an active Irish trading business, 12.5% is real and powerful. For a passive holding vehicle, the participation and dividend exemptions - not the trading rate - are what make Ireland efficient.

The Canadian angle

For a Canadian-owned Irish affiliate, the Irish rate split mirrors a Canadian concern. Active trading income reaches Canadian exempt surplus; passive income is likely FAPI, taxed in Canada as it accrues. So the trading-vs-passive line matters twice - once in Dublin, once in Ottawa. Designing the Irish company to earn genuinely active income keeps both sides clean.

Frequently asked questions

How do I know if my Irish company is “trading”?

It turns on genuine commercial activity carried on in Ireland - employees, decision-making, value creation and risk. It's a facts-and-circumstances test; get it reviewed rather than assumed.

Is investment income always 25%?

Passive income generally attracts the 25% rate, but specific exemptions (such as the participation and foreign-dividend exemptions) can remove qualifying dividends and gains from charge altogether.

Can one company have both trading and passive income?

Yes. Income is categorised by type, so a single company can pay 12.5% on its trade and 25% on separate passive income. Clean records matter.

Does the 12.5% rate help my Canadian tax bill?

Indirectly. A low Irish rate on active income, combined with exempt-surplus treatment in Canada, can produce an efficient overall result - but personal tax still applies when you extract funds in Canada.