Discover why Canadian technology and IP-driven businesses use Ireland for EU expansion, access to incentives, and international growth opportunities.

For a Canadian software, life-sciences or IP-heavy business eyeing Europe, Ireland is almost always on the shortlist. The reasons go well beyond the famous 12.5% rate - and a few of them matter more than the tax number.

More than a low rate

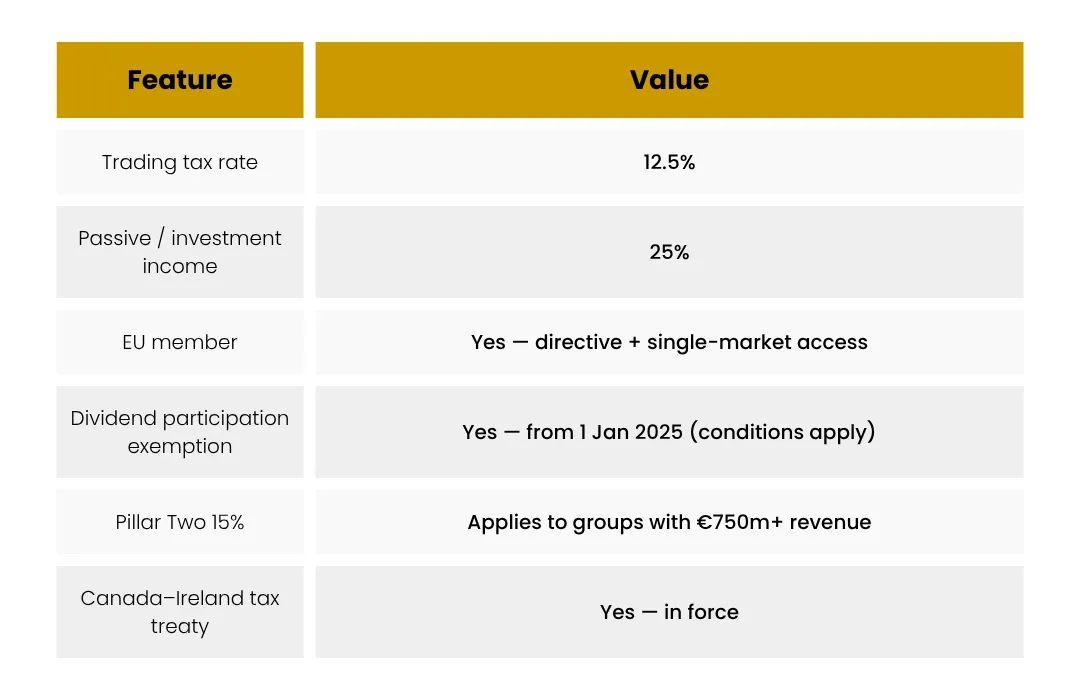

Ireland pairs a 12.5% trading tax rate with something rarer: it's an English-speaking, common-law, EU member state with a deep multinational ecosystem. For Canadian founders, that means familiar legal concepts, a workforce used to North American business norms, and a genuine doorway into the European single market.

Built for intangibles

Ireland has spent decades attracting IP-rich business. It offers a Knowledge Development Box (a reduced rate on income from qualifying IP), capital allowances for acquired intangibles, and an R&D tax credit. If your value sits in software, patents or brands, Ireland's regime is designed with you in mind - though each relief has detailed conditions.

A real gateway, not a mailbox

Because Ireland is in the EU, an Irish company can access the EU Parent-Subsidiary and Interest & Royalties Directives and Ireland's wide treaty network - reducing withholding tax on flows from European subsidiaries. But modern Ireland expects substance: people, premises and real decision-making. The mailbox era is over.

Where Ireland fits a Canadian group

- You're expanding into Europe and want one credible EU base.

- Your business is IP- or services-led and benefits from the trading rate and IP reliefs.

- You want an English-speaking, common-law jurisdiction your lawyers and bankers already understand.

The Canadian angle

Ireland is a treaty country with Canada, so active business income earned through an Irish foreign affiliate generally reaches exempt surplus - repatriable tax-free to a Canadian corporate parent. Combine that with Ireland's EU access and you get a clean, defensible European layer. Just remember the Canadian reporting: Form T1134 for the affiliate, every year.

Frequently asked questions

Is the 12.5% rate available to any Irish company?

No - 12.5% applies to trading income. Passive or investment income is taxed at 25%. The distinction between trading and passive is central to Irish tax and is fact-specific.

Do I need staff in Ireland?

For a genuine trading or holding presence, yes - substance matters for both Irish tax and to support treaty positions. The level depends on what the company actually does.

Does Ireland have a minimum tax now?

Ireland applies the OECD Pillar Two 15% minimum to large groups (consolidated revenue of €750m or more). Most owner-managed Canadian groups are below that threshold and keep the 12.5% trading rate.

Can I use Ireland just to hold European subsidiaries?

Yes - that's a common use. The participation exemption and EU directives can make dividends and exits efficient, provided the holding conditions and substance are met.