Understand Hong Kong's offshore claim rules, territorial tax system, substance requirements, and how Canadian tax rules affect offshore profits.

Hong Kong's most famous feature is that profits earned outside Hong Kong can escape Hong Kong tax entirely. It's real - but it's an evidence-based claim, not an automatic switch. Here's how the offshore claim actually works.

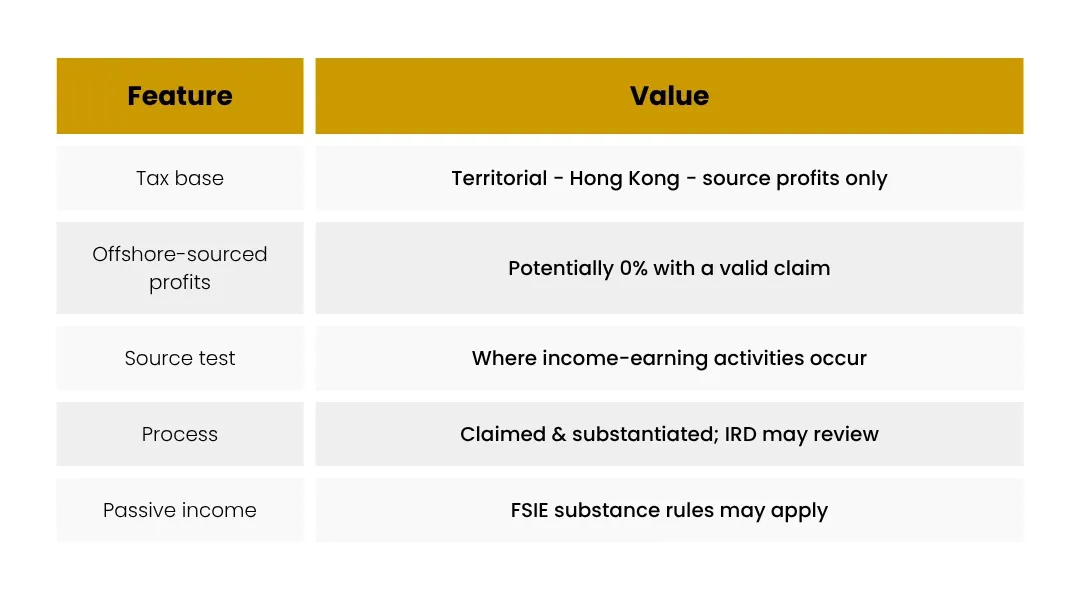

Territorial, not worldwide

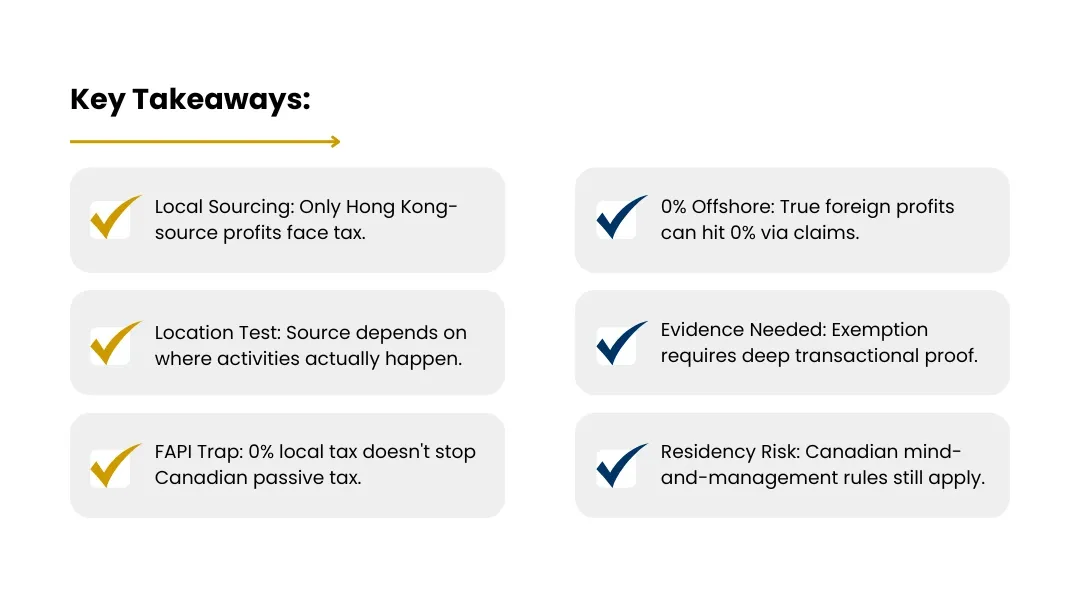

Hong Kong only taxes profits that arise in or are derived from Hong Kong. Profits genuinely sourced elsewhere are, in principle, outside the charge - the basis of the “offshore claim.” This is fundamentally different from Canada's worldwide system, and it's why Hong Kong can produce a 0% result on the right facts.

How source is determined

Source is decided by looking at what the business actually did to earn the profit, and where. For trading profits, the focus is typically where the purchase and sale contracts were effected; for services, where the services were performed. It's a facts-driven test - the Inland Revenue Department (IRD) examines operations, not labels.

The claim is a process, not a default

An offshore position must be claimed and substantiated: you file on the basis that profits are offshore, and the IRD may ask detailed questions. Sloppy or contrived claims fail. And since the FSIE reform (next article), certain offshore passive income now needs economic substance in Hong Kong to stay exempt.

The honest caveat

A 0% offshore claim is powerful but must be genuine and well-documented. The structures that survive an IRD review are the ones with real records showing where the income-earning activities took place. Treat the claim as a position you can defend - because you may have to.

The Canadian angle

Be careful what you wish for. A Hong Kong company with a 0% offshore claim, owned by Canadians, may earn income that Canada treats as FAPI (if passive) - taxed currently in Canada regardless of the Hong Kong result. And a structure with no real Hong Kong activity risks being seen as managed from Canada. The offshore claim helps your Hong Kong bill; it doesn't switch off Canadian rules. Plan both.

Frequently asked questions

Is the offshore claim automatic?

No. You must claim it and be able to prove the profits were sourced outside Hong Kong. The IRD frequently issues detailed enquiries, so contemporaneous evidence is essential.

What evidence supports an offshore claim?

Records showing where contracts were negotiated and concluded, where services were performed, where staff operated, and where decisions were made. The more complete and contemporaneous, the stronger the claim.

Does the offshore claim work for passive income too?

Since the FSIE reform, certain offshore passive income (dividends, interest, IP income, disposal gains) needs adequate Hong Kong substance to stay exempt. See our FSIE article.

Can my Canadian-owned HK company rely on 0% with no real activity?

That's risky on both sides - the offshore/FSIE rules and Canada's residence and FAPI rules can each undo it. Genuine substance is the safeguard.