Learn why Canadian businesses use a Hong Kong holding company for China and Asia expansion, treaty benefits, exempt surplus treatment, and tax efficiency.

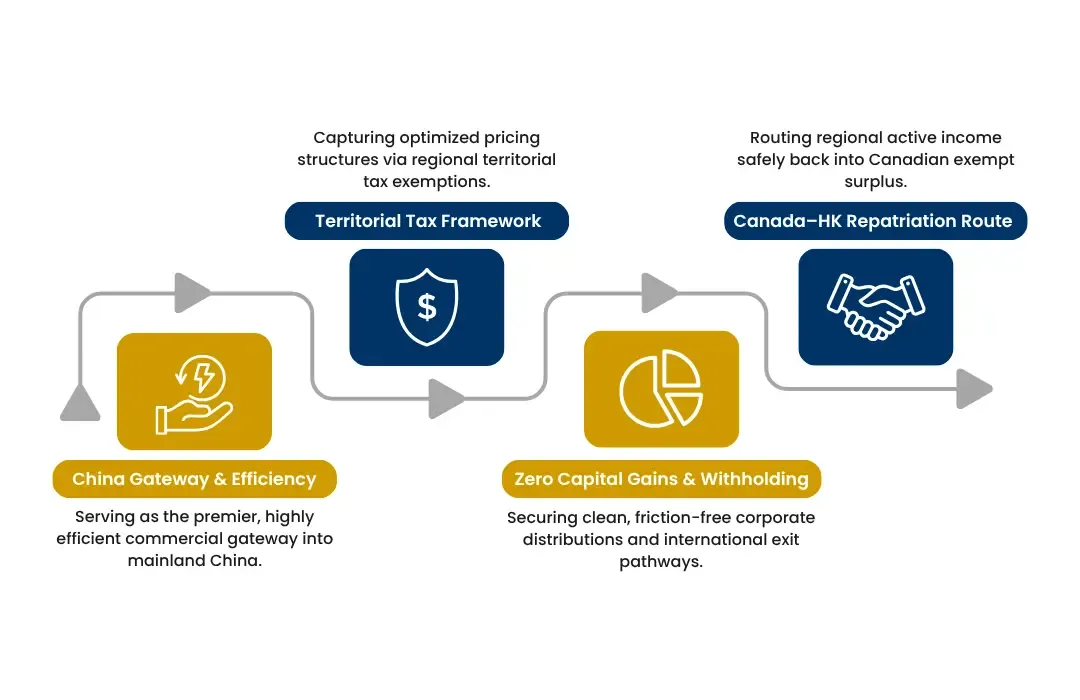

If your business touches mainland China - sourcing, manufacturing, selling - Hong Kong is the holding jurisdiction built for exactly that journey. It's the most efficient on-ramp into China that the rest of the world can actually use.

The China connection

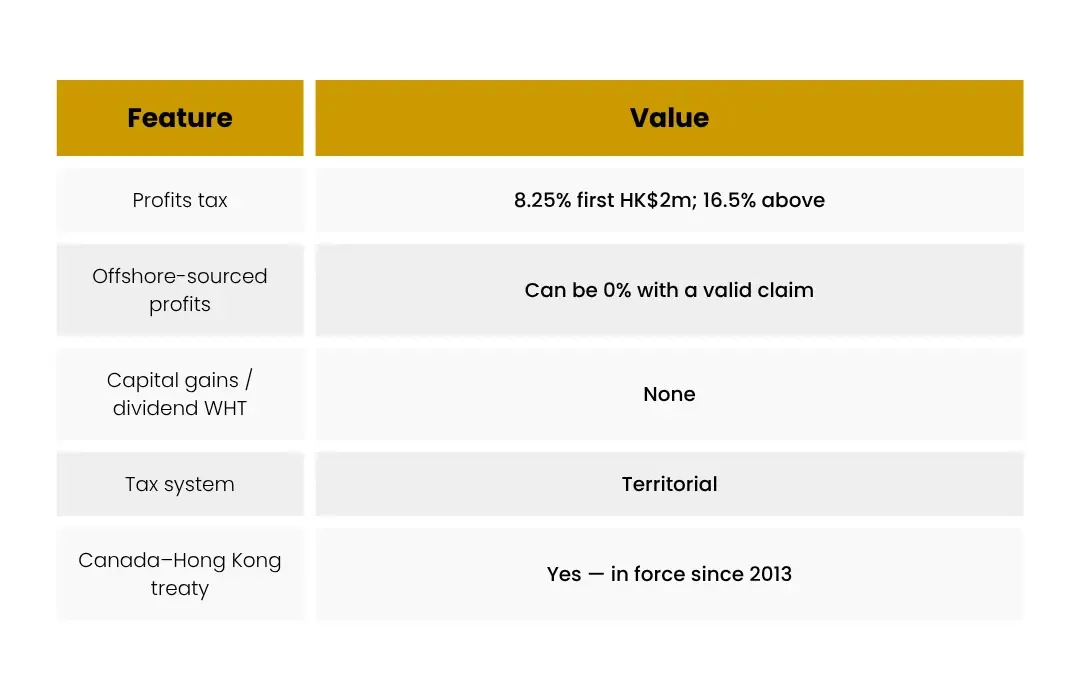

Hong Kong's defining advantage is its relationship with the mainland. The China - Hong Kong tax arrangement delivers some of the lowest withholding-tax rates available on dividends, interest and royalties flowing out of China - better than most countries can obtain directly. For a Canadian group with Chinese subsidiaries, a Hong Kong layer can dramatically reduce that leakage.

A genuinely low-tax, simple system

Hong Kong taxes profits on a territorial basis. The profits-tax rate is two-tiered - 8.25% on the first HK$2 million of assessable profits and 16.5% above - and profits genuinely sourced offshore can, with a valid claim, be taxed at 0%. There's no tax on dividends, no capital gains tax, and no withholding tax on dividends paid out.

World-class infrastructure

- A deep, sophisticated banking sector and free flow of capital.

- Common-law legal system familiar to Canadian advisors.

- Fast, low-friction incorporation.

- A natural regional base for Asia-Pacific operations.

When Hong Kong fits

Hong Kong is strongest for groups whose operations point at China and North Asia. For pan-Asian or globally neutral structures, Singapore often competes closely (see our comparison). Let the destination of your business - not fashion - pick the hub.

The Canadian angle

Since 2013, Canada and Hong Kong have a tax treaty, so active business income through a Hong Kong foreign affiliate reaches exempt surplus - repatriable tax-free to a Canadian corporate parent. That treaty status is what makes Hong Kong's low rate genuinely useful to a Canadian owner, rather than just a number. Passive income remains FAPI, and the affiliate needs annual T1134 reporting.

Frequently asked questions

Do I need to visit Hong Kong to set up?

No. Incorporation can be handled remotely with proper KYC. You'll need a company secretary and registered office in Hong Kong, and bank onboarding may require more diligence.

Is Hong Kong really tax-free?

No - it's low-tax and territorial. Hong Kong-sourced profits are taxed at up to 16.5%; only genuinely offshore profits, with a valid claim and adequate substance for certain income, reach 0%.

Is Hong Kong good for non-China business?

It can be, but its standout advantage is China access. For pan-Asian or neutral structures, compare it against Singapore before deciding.

Will Canada tax the Hong Kong company's profits?

Active income reaches exempt surplus and is repatriable tax-free to a Canadian corporate parent; passive income is generally FAPI, taxed in Canada as earned.