Understand Cyprus's 2026 tax reform, including the new 15% corporate tax rate, dividend exemptions, and implications for Canadian holding companies.

Cyprus changed its tax rules on 1 January 2026 - and if you're relying on an old “12.5% Cyprus” article, you're out of date. Here's the current picture for a holding company, including what went up, what came down, and what stayed the same.

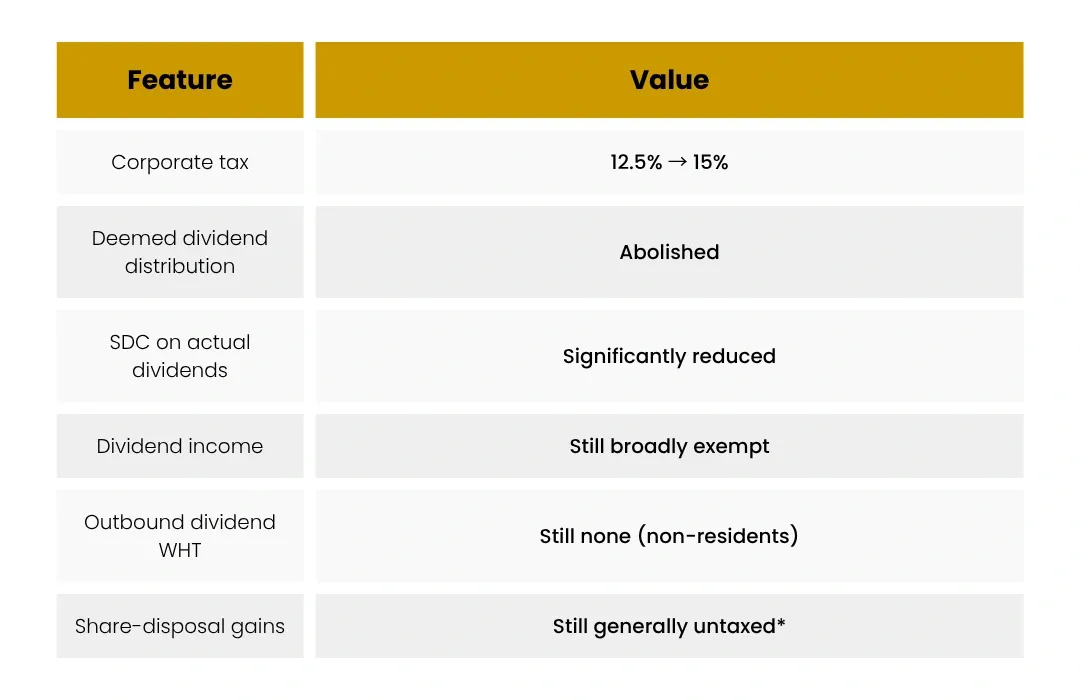

The headline: 15%, not 12.5%

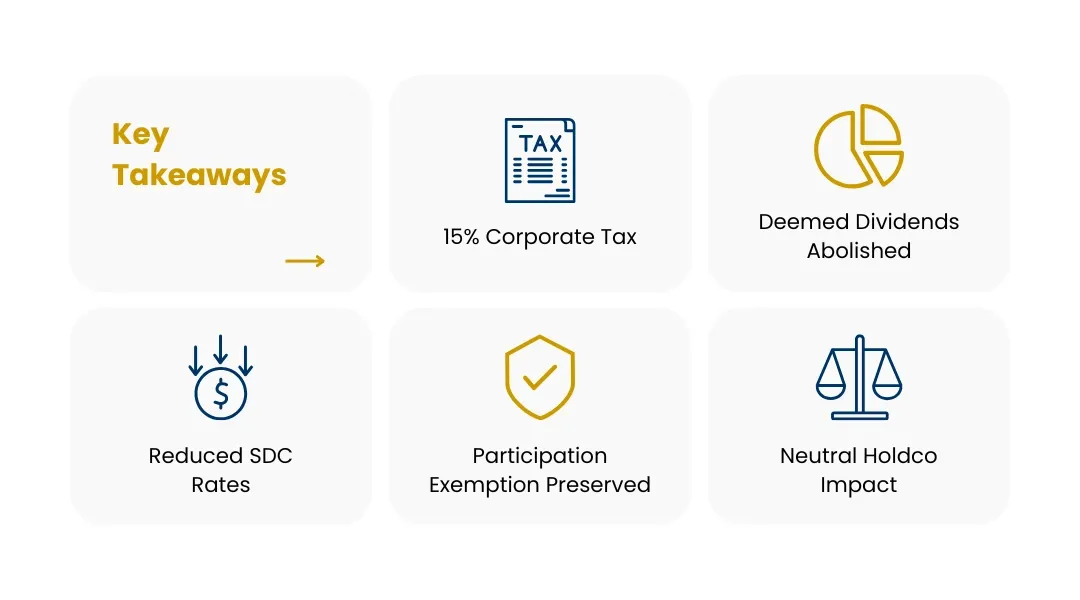

The reform raised the corporate income tax rate from 12.5% to 15%, aligning Cyprus with the OECD global-minimum-tax standard. It's still one of the lower headline rates in the EU - but the old 12.5% selling point is gone, so plan on 15%.

What the reform gave back

The increase came with offsetting changes that often help holding structures:

- The deemed dividend distribution regime was abolished - removing a long-standing trap that taxed undistributed profits of Cyprus-resident shareholders.

- Special Defence Contribution (SDC) on actual dividends was significantly reduced.

- Enhanced R&D incentives and other modernising measures.

What didn't change for a holdco

The core holding-company benefits survived: dividend income remains broadly exempt from corporate tax, there's no withholding tax on dividends to non-residents, and gains on share disposals are generally untaxed (absent Cyprus real estate). The reform refreshed the rate, not the fundamental holding regime.

Net effect for a Canadian owner

For most Canadian-owned Cyprus holdcos, the reform is close to neutral-to-positive: a slightly higher headline rate (which they may pay little of, given the dividend exemption) traded for the removal of the deemed-distribution trap and lower SDC. The case for Cyprus as a lean EU base is intact.

The Canadian angle

The rate rise barely touches the Canadian calculus: as a treaty country, Cyprus active income still reaches exempt surplus. A modestly higher (15%) genuine local tax can even strengthen the “subject-to-tax” character of the income. What matters for Canadians is unchanged - keep income active, maintain substance, file the T1134, and watch FAPI on any passive accumulation.

Frequently asked questions

Why did Cyprus raise its corporate tax?

To align with the OECD's 15% global minimum tax standard. Many low-tax jurisdictions made similar moves; Cyprus paired the increase with offsetting reliefs.

Is the dividend exemption still available?

Yes - dividend income received by a Cyprus company remains broadly exempt from corporate tax, subject to anti-abuse conditions. This is central to its holding-company appeal.

What was the deemed dividend distribution and why does abolishing it help?

It previously taxed a portion of undistributed profits attributable to Cyprus-resident shareholders. Abolishing it removes a complexity and potential cost, simplifying profit retention.

Does the 15% rate make Cyprus less competitive than Ireland?

Ireland's 12.5% is a trading rate; for holding companies the dividend and gains treatment matters more than the headline. Cyprus remains competitive, especially on running cost.