Learn what a zero-tax BVI holding company means for Canadian business owners, including FAPI, taxable surplus, TIEA rules, and reporting obligations.

“The BVI has zero tax” is true - and one of the most misunderstood sentences in cross-border planning. For a Canadian owner, the BVI's zero tax doesn't mean your income is tax-free. It means the tax happens somewhere else: Canada. Here's the honest picture.

What the BVI does - and doesn't - charge

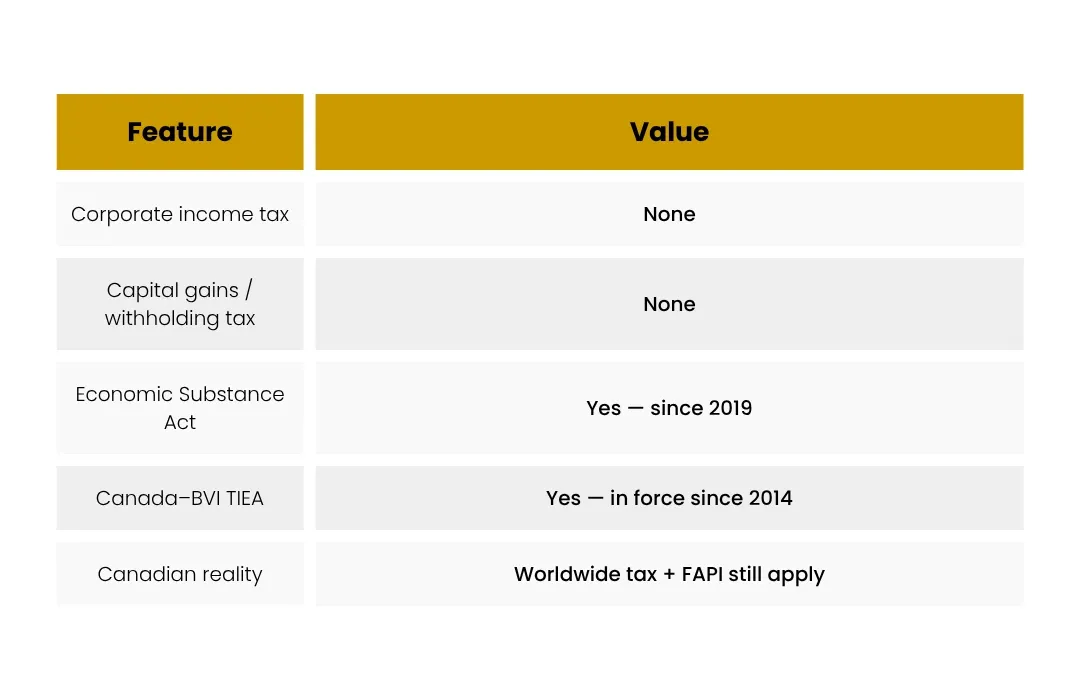

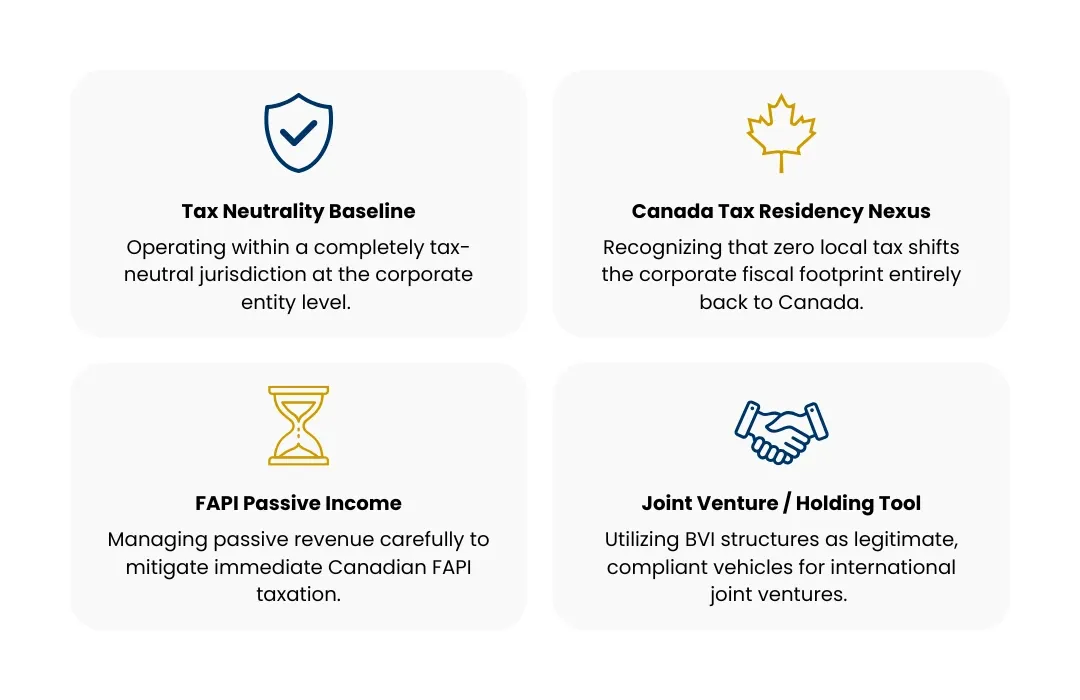

A British Virgin Islands company pays no corporate income tax, no capital gains tax, and no withholding tax. There's genuinely no BVI tax on a holding company's profits. That's the appeal - a neutral, tax-free wrapper recognised worldwide.

Why zero tax can be a trap for Canadians

Here's the catch most promoters skip. Canada taxes its residents on worldwide income, and has powerful rules for foreign companies owned by Canadians. A BVI company's passive income is typically FAPI - taxed in Canada as it accrues, at full rates, whether or not you take a distribution. Zero BVI tax simply means no foreign tax credit to offset the Canadian bill.

The surplus problem

Even active business income gets sorted into Canadian surplus pools. Crucially, the BVI is a zero-tax jurisdiction - so without the Canada - BVI TIEA, its income would be taxable surplus (taxed on the way home, with no credit). The TIEA changes this for active income (see our dedicated article) - but the structure has to be genuine to use it.

When a BVI holdco still makes sense

- As a neutral joint-venture or co-investment vehicle between parties from different countries.

- As a clean holding wrapper in a larger group where Canadian rules are properly managed.

- Where flexibility and speed of a well-understood offshore company are valued.

What it is not is a way for a Canadian resident to make income disappear.

The Canadian angle

This is the Canadian angle, so be blunt about it: a BVI company owned by a Canadian resident does not escape Canadian tax. Passive income is FAPI, taxed currently; active income depends on substance and the TIEA. And you must file T1134 (foreign affiliate) and possibly T1135 (foreign property) - with real penalties for missing them. Used honestly within Canadian rules, the BVI is a legitimate tool; used to “hide” income, it's a liability.

Frequently asked questions

If the BVI has no tax, why would I still pay Canadian tax?

Because Canada taxes residents on worldwide income and has anti-deferral rules (FAPI) for foreign companies they control. Zero BVI tax doesn't remove the Canadian charge - it just means no foreign tax to credit against it.

Is a BVI company illegal for a Canadian?

No - owning a BVI company is entirely legal if properly reported (T1134, T1135 and income inclusions where required). What's illegal is failing to report it or using it to conceal income.

When is a BVI company genuinely useful?

As a neutral joint-venture vehicle, a clean holding wrapper, or part of a larger group where the Canadian rules are managed. Its value is structural flexibility, not tax disappearance.

Does the Canada - BVI TIEA help?

Yes - for active business income it can enable exempt-surplus treatment, because the TIEA makes the BVI a designated treaty country. Passive income remains FAPI regardless.