Understand BVI economic substance requirements for Canadian-owned holding companies, including reporting obligations, compliance rules, and CRA visibility.

The phrase “offshore” used to mean “no questions asked.” Not anymore. The BVI's Economic Substance Act means even a zero-tax company has obligations - and while pure holding companies get a lighter test, “lighter” is not “none.”

Why a zero-tax place has substance rules

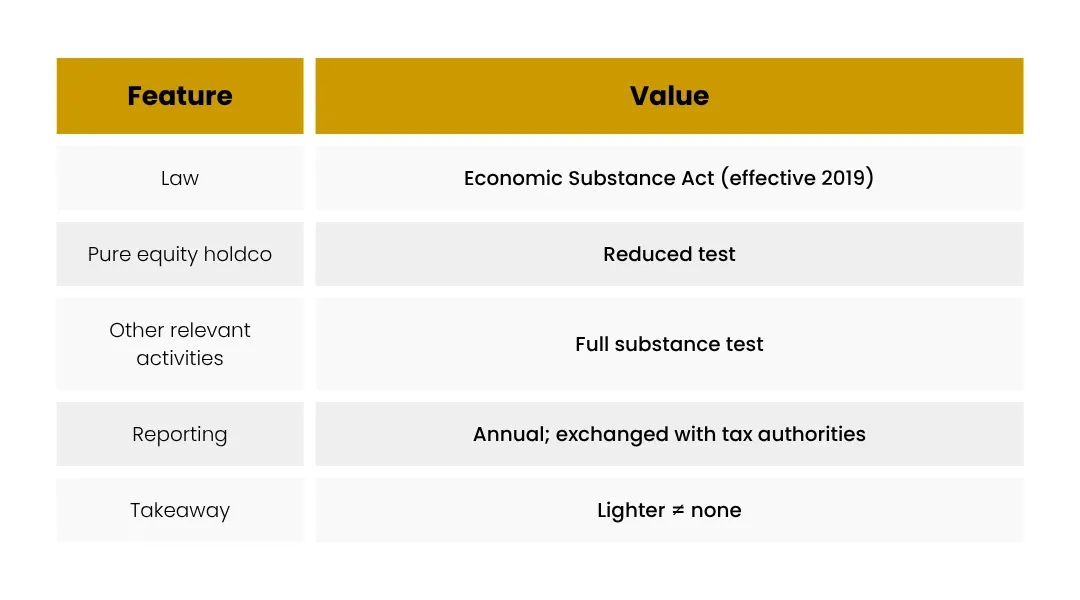

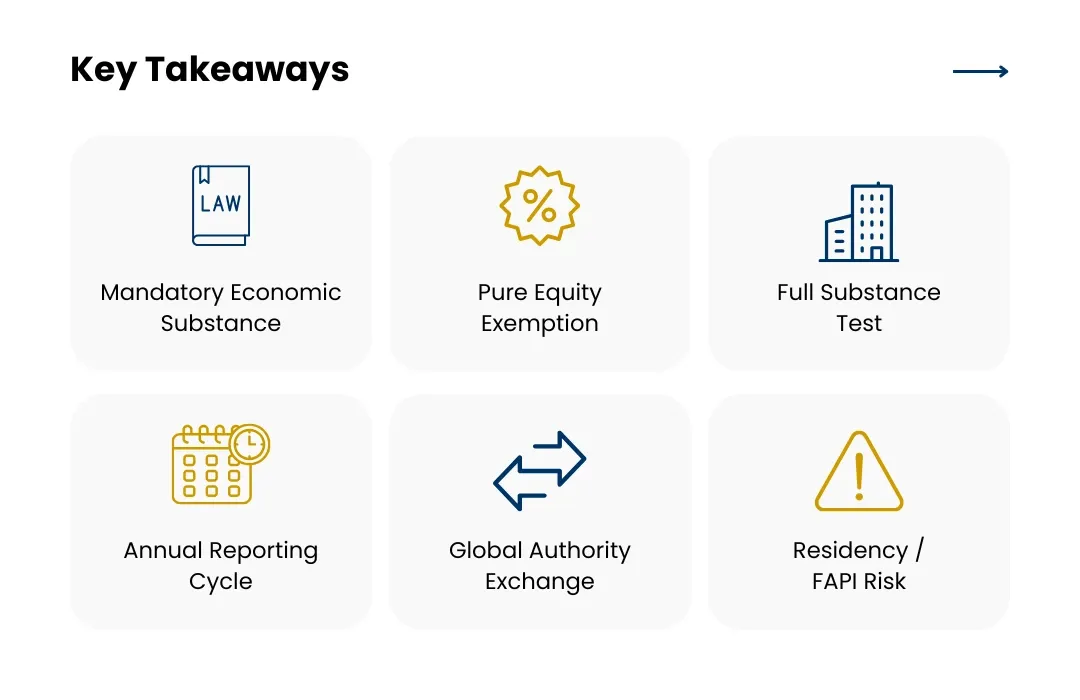

Under international (EU and OECD) pressure, the BVI enacted the Economic Substance Act (effective 2019). Companies carrying on defined “relevant activities” - including holding-company business, financing, IP, distribution and others - must demonstrate adequate substance in the BVI or report accordingly. The era of the pure paper company is over even where there's no tax.

The reduced test for pure equity holdcos

A pure equity-holding company (one that only holds equity participations and earns dividends and gains) faces a reduced substance test. Broadly, it must:

- Comply with its statutory filing obligations under BVI company law; and

- Have adequate employees and premises for holding and managing those equity participations - which can be satisfied through its registered agent in many cases.

Companies with more active relevant activities (e.g., financing or IP) face the full test: core activities, direction and management, and adequate people/premises/expenditure in the BVI.

Reporting is mandatory

All in-scope companies must report substance information annually (now via the BVI's integrated registry system). Substance data can be exchanged with foreign tax authorities - including the CRA - so what you file in the BVI can surface in Canada.

The practical message

Don't treat the BVI as consequence-free. Even a holding company must meet its (lighter) substance test and file. And from a Canadian perspective, thin substance plus Canadian-based control is the combination that invites a residence or FAPI challenge.

The Canadian angle

BVI substance reporting is shared with the CRA. A BVI company with no real substance, controlled from Canada, is exposed on two fronts: it may breach BVI substance rules and be treated by Canada as resident here (managed and controlled from Canada) - collapsing any offshore benefit. Genuine substance, or honest reporting of the lack of it, is the only safe path.

Frequently asked questions

Does my BVI holding company need employees in the BVI?

A pure equity-holding company faces a reduced test that can often be met through the registered agent and by meeting filing obligations. Companies with active relevant activities need genuine people, premises and management in the BVI.

What are “relevant activities”?

Defined categories including holding-company business, banking, insurance, fund management, financing and leasing, headquarters, shipping, IP and distribution/service-centre business. Each has its own substance expectations.

Is the substance information public?

No, but it is reported to the BVI authority and can be exchanged with foreign tax authorities under international agreements, including with Canada.

What if I ignore the substance rules?

Penalties, potential strike-off, and information exchange that can trigger scrutiny abroad. For Canadians, it also strengthens any CRA argument that the company is really Canadian-resident.