Financial Statements: How to Understand and Analyze Your Numbers

Running a business is not just about selling products or services. It’s also about keeping track of your money – how much is coming in, how much is going out, and how your business is doing overall.

This is exactly where financial statements come in.

Understanding your financial statements doesn’t need to be hard. And so, to help you get started into understanding what financial statements are, in this blog, we will be explaining everything so that you feel confident reading your numbers.

What Are Financial Statements?

Before we get deeper into the understanding of this comprehensive topic, let us first understand what are financial statements.

These are formal records that show the financial activities and condition of a business over a certain time period. They help you understand your profits, expenses, debts, and overall business health.

Banks, investors, and even tax authorities rely on these statements to check how a business is performing. But more importantly, you, the business owner, should use them regularly to make smart decisions.

Are you confident your business tax filings are fully optimized and compliant?

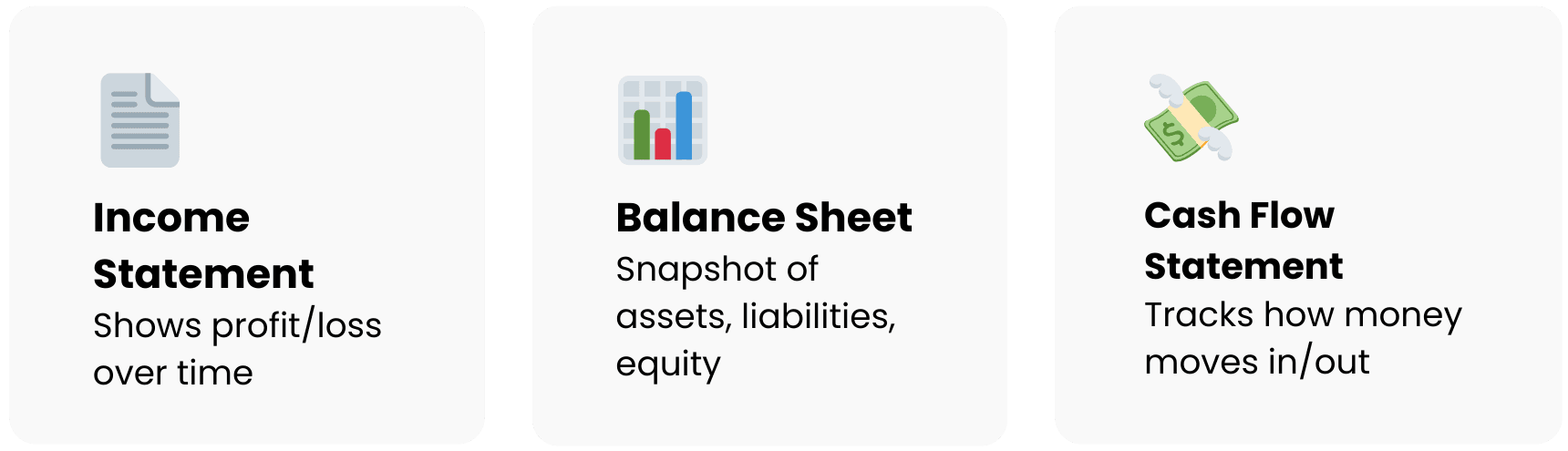

The Types of Financial Statement

There are three important types of reports that fall under the types of financial statement. These include the income statement, balance sheet, and cash flow statement. Each one gives a different picture of your business finances.

Let’s break them down one by one so you can understand them clearly.

Income Statement

The income statement is also known as a profit and loss statement or revenue statement. It shows how much your business earned and spent over a specific time – usually monthly, quarterly, or annually.

It starts with revenue (your total income), subtracts expenses (like rent, salaries, and supplies), and ends with your net profit or loss. This helps you understand if your business is making money or not.

Many people ask, what is a revenue statement? It’s simply another name for the income statement – a report that highlights your revenue and how it turns into profit (or loss).

Balance Sheet

The balance sheet shows what your business owns (assets), what it owes (liabilities), and what’s left for you as the owner (equity). It gives you a snapshot of your business’s financial position at a specific moment.

If your assets are more than your liabilities, it usually means your business is in good shape.

Cash Flow Statement

This statement shows how money moves in and out of your business. Even if your income statement shows a profit, you might not have enough cash on hand. The cash flow statement helps explain why.

It’s divided into three sections: cash from operations, investing, and financing. It shows where your money is coming from and where it’s going.

Overview of Financial Statements

Understanding financial statements is key to managing your business’s finances effectively. These reports provide valuable insights into your business’s performance and financial health.

Here’s a simple table to help you see the differences between these reports:

| Statement Type | What It Shows | Why It’s Important |

| Income Statement | Income, expenses, and profit/loss | Tells if your business is profitable |

| Balance Sheet | Assets, liabilities, and equity | Shows financial health at a point in time |

| Cash Flow Statement | Inflows and outflows of cash | Helps manage daily cash needs |

By regularly reviewing these financial statements, you can make informed decisions and keep your business on track. Each statement serves a unique purpose, helping you understand profitability, financial stability, and cash flow, which are important for long-term success.

|

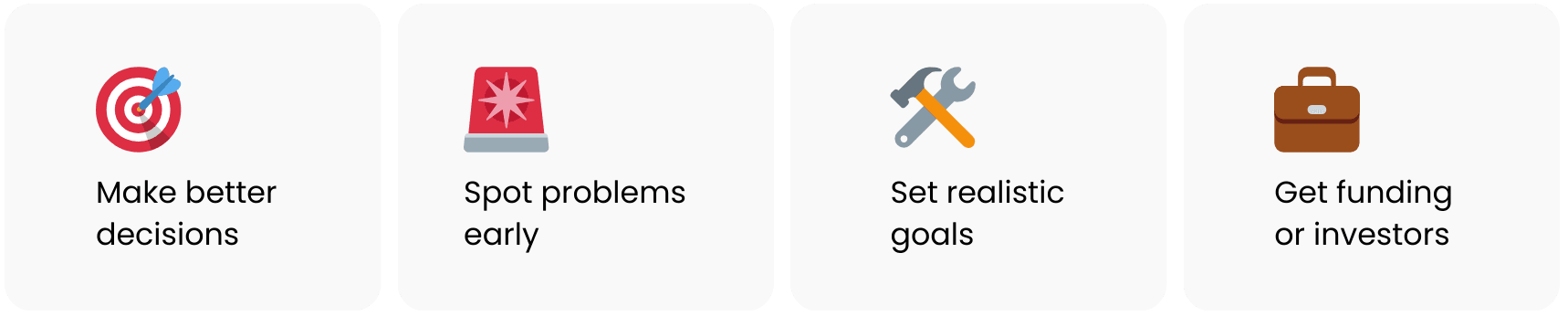

Why These Statements Matter

You might wonder why all these statements are so important. The truth is, without knowing your numbers, you’re flying aimless. These documents help you:

- Make better decisions

- Spot problems early

- Set realistic goals

- Get loans or attract investors

For example, if your income statement shows high sales but your cash flow statement shows negative cash flow, you know there’s a problem with how money is being managed.

Understand Trends, Not Just Numbers

One mistake many business owners make is only looking at one report or one month’s numbers. But what really matters is the trend. Are things getting better or worse?

Compare this month’s income with the last three months. Are you spending more on ads but not seeing extra sales? Is your inventory going up but your revenue staying the same?

These trends help you take action before small issues become big problems.

Remember that, even if you manage your books yourself, it’s a good idea to speak with a financial expert regularly. They can help you understand complex parts of your reports and give advice that fits your business.

A professional can also help you with taxes, growth planning, or solving cash flow issues saving you time and money in the long run.

Here, at Orbit Accountants, we specialize in helping business owners like you stay on top of their numbers. For years, we’ve been offering trusted bookkeeping, accounting, and tax services across Canada. Whether you’re a solo entrepreneur or running a fast-growing company, we make financial management simple.

From handling your books to preparing for tax season and planning for the future, we’ve got you covered. Book a free consultation today, and we’ll learn about your business, answer your questions, and guide you to the perfect solution.

In Essence,

Understanding financial statements is key to running a successful business. You don’t need to be a finance expert. You just need to understand what each report tells you and how to use that information to make better choices.

By reviewing your income, expenses, assets, and cash flow regularly, you’ll stay in control and avoid surprises. And when you have support from experienced professionals like Orbit Accountants, your financial journey becomes even easier!

Frequently Asked Questions

What are the main types of financial statements?

There are 3 main types of financial statements: the income statement shows profits and losses, the balance sheet shows what a business owns and owes, the cash flow statement tracks money coming in and out.

What information does an income statement provide?

An income statement shows how much money a business earned and spent over a period. It lists revenue, costs, and profits or losses. It helps you see if your business is making money and where expenses are going, making it easier to improve performance and plan ahead.

What are the key financial ratios used in financial statement analysis?

Common ratios include the current ratio (measures liquidity), debt-to-equity ratio (shows financial stability), gross profit margin (profit from sales), and return on investment (how well profits are made from money invested). These ratios help compare performance and spot problems or strengths in a business’s financial health.

How do financial statements help with business decision-making?

Financial statements show how a business is doing with money. They help you decide when to spend, save, invest, or cut costs. With this information, business owners can make smarter choices, like hiring staff, setting prices, or applying for loans based on real data, not guesswork.

How often should I review my financial statements?

It’s a good idea to review financial statements monthly to track performance and catch issues early. Quarterly reviews help with planning and reporting, and yearly reviews are important for taxes and long-term strategy. Regular reviews keep your business on track and help you make timely, informed decisions!