What Is Depreciation? And How to Calculate It

Depreciation is a familiar term for anyone who owns a business or invests in property. In a nutshell, depreciation measures how an asset loses value over time because of wear and tear, changes in technology, or basic aging. Businesses can use these calculations to reduce taxable income and get a clearer picture of their bottom line. But how does it work in Canada, and what are the rules if you want to claim property depreciation for a building or piece of equipment? This guide will walk you through the basics, explain how to calculate the amount, and show you how different methods play out in financial statements.

Why Depreciation Matters for Canadian Businesses

Imagine you buy a new delivery van for your company. Over time, it loses value as it racks up kilometres and endures wear and tear. Depreciation is the way to record that loss in value year after year. This is important for several reasons:

- Accurate Financial Statements: An income statement that expenses the cost of an asset too quickly or not at all can misrepresent profits. It spreads the cost over the life of the asset.

- Tax Deductions: In Canada, businesses use depreciation to reduce taxable income. If you didn’t deduct the cost of your fixed assets over time, you’d pay higher taxes in the early years.

- Better Decision-Making: Depreciation figures help you see when it’s time to upgrade, how assets affect your bottom line, and how to plan for capital expenditures.

While depreciation is sometimes used interchangeably with capital cost allowance (CCA), they share the same idea: an asset’s cost is split across its useful life, giving a realistic measure of actual wear and tear.

Key Terms and Concepts

- Cost of an Asset: The price you paid, plus any fees to install or transport it. This total becomes your starting point.

- Life of the Asset: How long you expect to use it before it’s retired or replaced.

- Accumulated Depreciation: The sum of all yearly depreciation amounts so far. On the balance sheet, it’s shown as a negative entry against the asset.

- Wear and Tear: The natural decline in an asset’s value from everyday usage.

- Tax Deduction: Depreciation can be claimed as an expense on your tax return, reducing taxable income.

In simple terms, assets depreciate because they don’t last forever. You might keep a computer for three years, a vehicle for five, and an office building for decades. Each year, you allocate part of the cost as an expense, ensuring your income statement reflects reality.

Also Read: Self-Employment Tax Deductions in Canada: The Ultimate Guide

Are you currently managing your bookkeeping in-house?

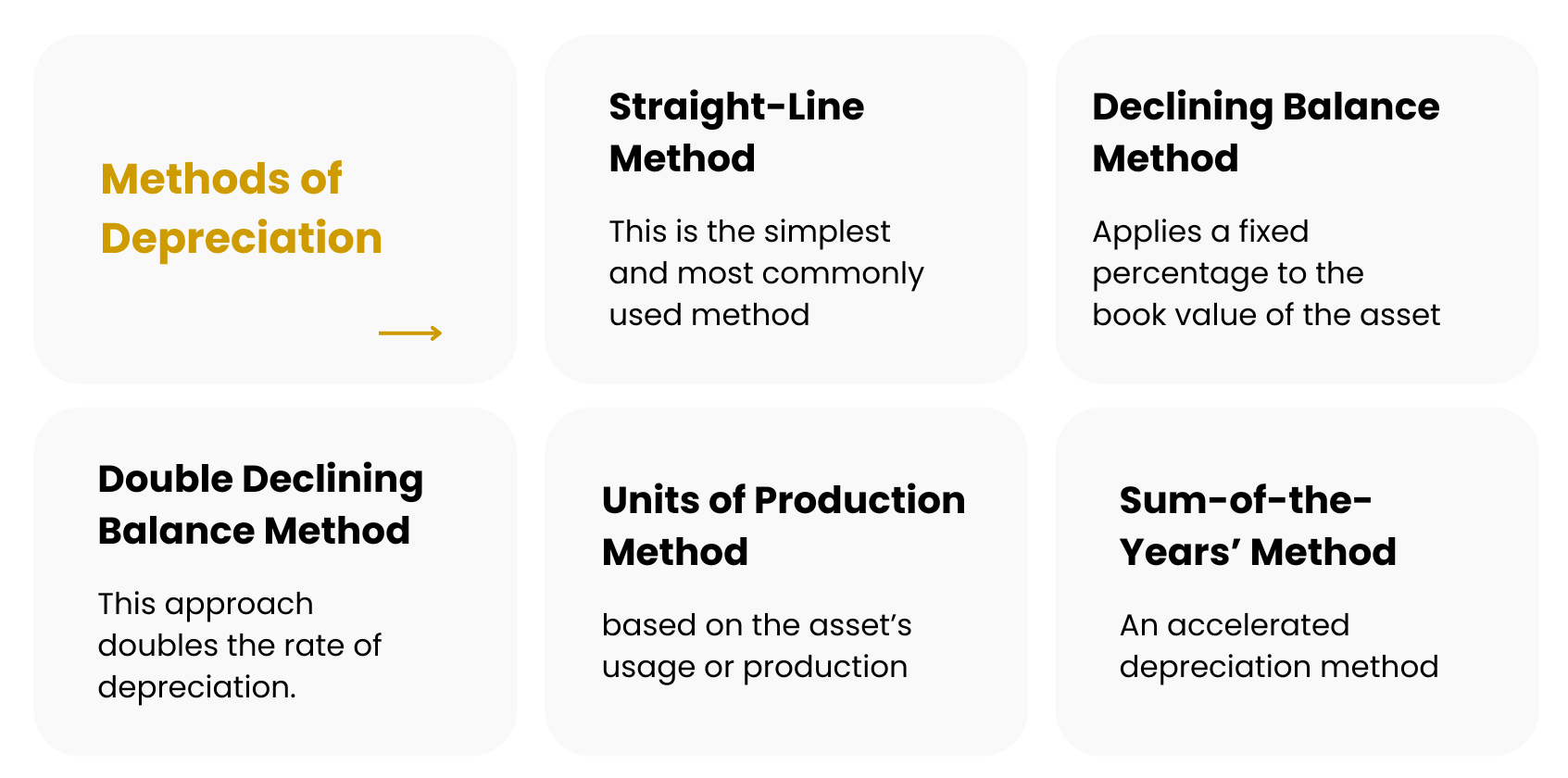

Different Methods of Depreciation

Though the concept is the same—spreading an asset’s cost over time—there are various ways to calculate depreciation. Here are the most common methods:

1. Straight-Line Depreciation Method

- You deduct an equal amount each year for the asset’s useful life.

- Formula: (Cost of Asset – Salvage Value) / Useful Life

- Example: If a $10,000 machine is expected to last 10 years with no salvage value, you’d depreciate $1,000 annually.

2. Declining Balance Method

- Each year, you apply a fixed percentage to the remaining book value.

- The asset depreciates more in early years, less later on.

- For instance, if you have a 30% rate, in year one you multiply the cost by 30%, in year two you multiply the new (reduced) amount by 30%, and so forth.

3. Sum of the Years’ Digits

- A slightly more complex approach that weights earlier years higher.

- If an asset’s life is 5 years, you sum digits 1+2+3+4+5 = 15. In the first year, you depreciate 5/15 of the cost, in the second year 4/15, and so on.

4. Units of Production Depreciation

- Ties depreciation to usage (hours or units produced) rather than time.

- Common for manufacturing equipment where “wear” depends on actual output.

Though the “straight line method” is easiest to grasp, each type may fit different assets or business needs. In Canada, the CCA system effectively uses a declining balance approach for many asset classes (with some exceptions).

Using a Depreciation Schedule

A “depreciation schedule” or “CCA schedule” is simply a table tracking each asset, its cost, the method or rate applied, and the remaining undepreciated balance. Over the life of the asset, you update the schedule yearly to reflect how much value remains. This is handy for:

- Tax Return Preparation: You won’t guess how to calculate depreciation every time, as the schedule is your record.

- Financial Statements: Lays out the annual depreciation expense. If you have multiple vehicles, equipment, or property, a schedule keeps it organized.

- Future Planning: A depreciation schedule reveals when major assets might become fully depreciated and need replacement.

In short, the schedule keeps you consistent from year to year.

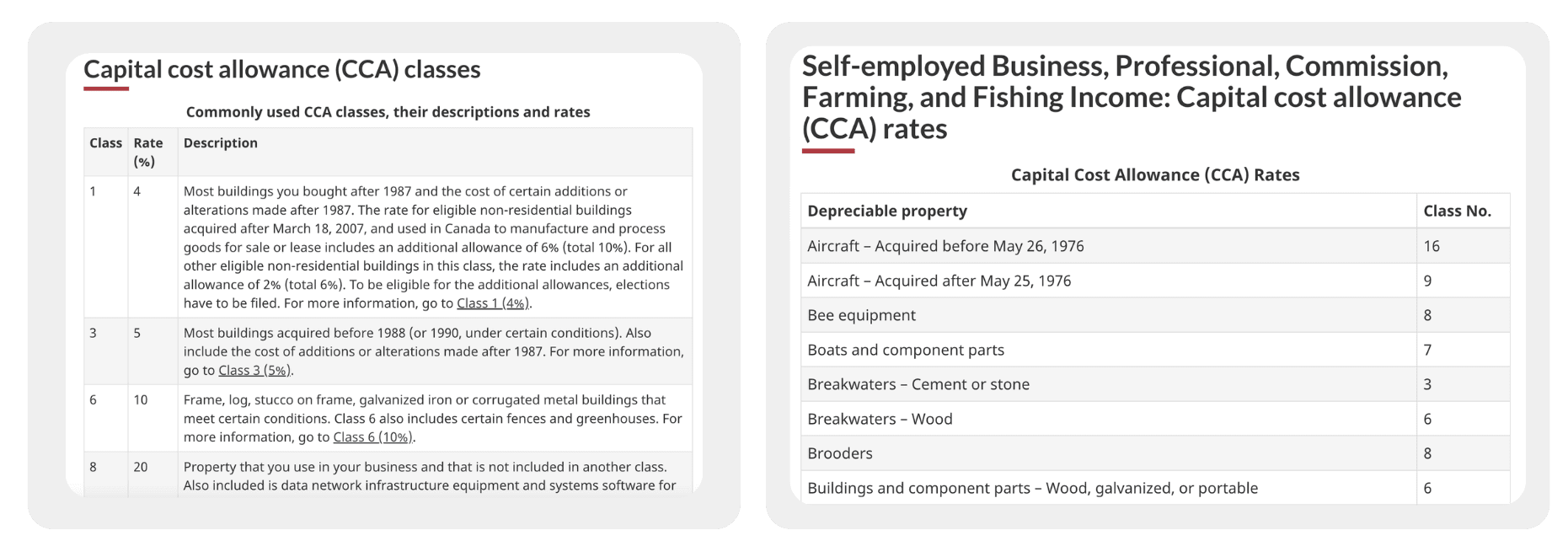

The CCA Approach

In Canada, the CRA uses Capital Cost Allowance (CCA) classes to regulate how quickly you can write off an asset. Each class has a specific rate. For example, a Class 10 vehicle might have a 30% declining balance rate, while a Class 8 piece of equipment might have 20%. The CRA site has a master list of classes, or you can consult an accountant to match your property to the correct category.

- Claiming CCA: You decide how much to claim each year, up to the maximum. If you prefer not to reduce your taxable income too fast (maybe your income is lower in that year), you can claim less.

- Half-Year Rule: Often, in the first year you only claim half of the normal rate to avoid fully depreciating brand new assets too quickly.

- Property Depreciation: For real estate like rental properties, you may place the building in Class 1 or another class. Land itself is not depreciable; only the building portion is.

CCA helps you manage your taxable income effectively, though you must follow the CRA’s rate tables rather than picking any method you want.

Frequently Asked Questions

1.What is depreciation?

It is the process of spreading the cost of an asset over its useful life. Each year, you record an expense to show how the asset loses value.

2. How to calculate depreciation for business assets?

In Canada, many businesses follow the CRA’s CCA system. You find the asset’s class, apply the appropriate rate, and deduct that portion from your income. Common methods include straight-line or declining balance.

3. Can you claim depreciation on rental properties?

Yes, you may claim CCA on the building portion of a rental property. But claiming it can trigger future recapture if you sell the property at a profit, so weigh the pros and cons.

4. What happens when an asset is fully depreciated?

Once you’ve claimed its entire cost, the asset’s book value is zero in your accounts. If you sell it for more than that, you may have a gain (and possibly recapture of depreciation). If it’s worthless, you might scrap it from your records.

Key Takeaways

- CCA ensures you don’t lump the entire cost of a long-lived asset into one year, giving a fair reflection of wear and tear.

- In Canada, the CCA schedule is crucial for tracking each asset’s remaining undepreciated cost.

- The CRA sets out rules (like the half-year rule) and rates for different asset classes, so your main job is to identify the correct class and apply the right rate.

- “Property depreciation” for real estate can’t be claimed on the land portion, only on the building or improvements.

- Once an asset is fully depreciated, any further usage is effectively free from a book perspective, though you must track potential recapture if you sell it.

Conclusion

Depreciation stands for more than just an accounting chore. It’s a strategic tool that helps businesses recognize the ongoing cost of fixed assets, keep financial statements honest, and manage taxes more effectively. From choosing the right method—like the straight line method or a declining balance approach—to following the CRA’s guidelines for capital cost allowance, each step can ensure your business doesn’t overstate profits or pay more tax than needed.

If you’re new to the process, begin by making an asset list, grouping them into categories, and reading up on the CRA’s specific classes and rates. You can often do the calculations yourself if you have a small operation, but as your business grows or your assets become complicated, consider seeking professional advice. An accountant can steer you through advanced topics, or whether a particular asset might qualify for a faster rate.

By mastering this subject, you not only comply with Canadian tax law, but also gain insights into how your assets affect the business’s bottom line. The end result is better financial planning, more precise budgeting, and a clearer picture of how your major investments wear down over time. That’s a win for both your books and your overall business strategy.

For Val: Tables and Graphics Ideas

1. Flowchart

- Start: “Purchase Asset” → Next: “Identify Class or Depreciation Method” → Next: “Apply Rate or Formula” → Finally: “Record Depreciation on Income Statement.”

2. Table: Example of Declining Balance

| Year |

|

| Depreciation |

| ||||||

| 1 | $10,000 | 30% | $3,000 | $7,000 | ||||||

| 2 | $7,000 | 30% | $2,100 | $4,900 | ||||||

| 3 | $4,900 | 30% | $1,470 | $3,430 |

3. Checklist

- “Classify Asset → Check CRA Rate → Apply half-year rule if needed → Record monthly or yearly → Summarize on T2 or T1 if sole prop.”