Self-Employment Tax Deductions in Canada: The Ultimate Guide

Working for yourself offers flexibility and control, but it also means handling your own taxes. If you’re self-employed in Canada—whether you consult, freelance, or run a small online store—understanding eligible write-offs can help lower your tax bill and keep more money in your pocket.

This guide explores crucial self-employment tax deductions, focusing on how Canadians can claim them according to Canada Revenue Agency (CRA) rules. We’ll also look at why each expense matters, how to keep track of them, and common mistakes to avoid. By the end, you’ll have a clearer strategy for your next filing season, from the list of typical expenses (like business insurance, home office costs, or interest payments) to the best ways to stay organized all year.

Introduction: Why Self-Employed Deductions Matter

Being self-employed in Canada means you wear multiple hats—owner, marketer, accountant, and everything else. At tax time, you’re responsible for reporting all business income on your personal tax return, typically using the T2125 form if you’re a sole proprietor or in a partnership. The good news: many expenses that help you run your business can be written off, reducing your taxable income. If you don’t take advantage of them, you might end up paying more than you should.

However, it’s not about simply listing everything you can think of. The CRA has guidelines on whether a cost is truly business-related, whether it should be capitalized (like big equipment) or claimed outright, and how partial personal usage can affect your deduction. If you keep an eye on these rules, you’ll be able to maximize your write-offs while staying on the right side of the law.

Are you confident your business tax filings are fully optimized and compliant?

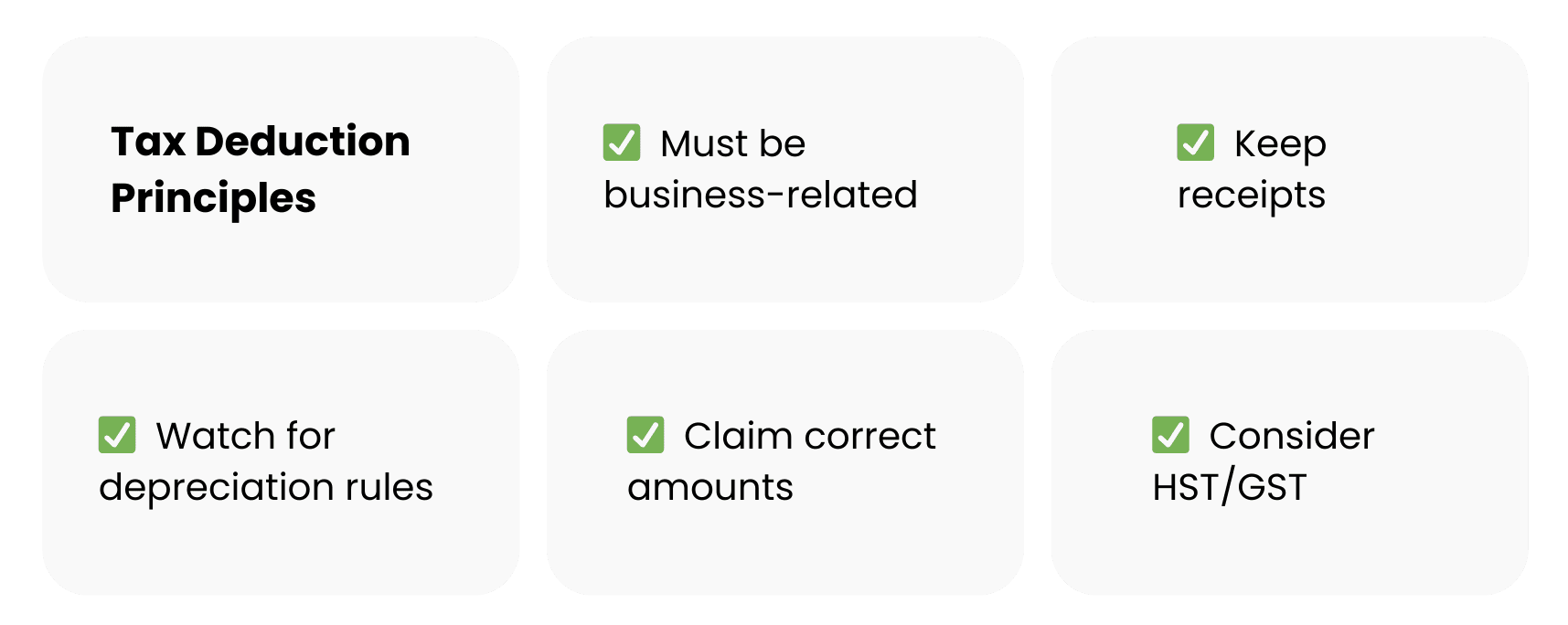

Key Things to Know Before You Start

- Must Be for Business: Every cost you claim must directly help you earn income. If you blend personal and professional usage—like with a cell phone—you can only deduct the business percentage.

- Keep Records All Year: Don’t wait until April to rummage for receipts. Set up a system that captures each expense at the time you pay it, noting the reason and the portion that’s business-related.

- Watch Out for Big Purchases: Large assets often need to be depreciated rather than deducted in one shot. For instance, a new $3,000 computer might be subject to capital cost allowance (CCA).

- Claiming the Right Amount: Some categories, like meals and entertainment, typically allow for only 50% of the cost. Others, like mileage, have specific ways to keep track.

- HST/GST: If you’re registered for the goods and services tax (GST) or harmonized sales tax (HST), your net expense might be only the after-tax amount if you claim input tax credits. Adjust your deductions accordingly so you don’t double-claim or miss out.

Overview of Common Self-Employment Deductions

Below is a quick list of the main categories we’ll go into:

- Advertising

- Business Insurance

- Business Startup and Organizational Costs

- Commissions and Fees

- Commissions and Fees

- Contract Labour

- Depreciation

- Employee Benefits

- Home Office Expenses

- Interest Payments

- Legal and Professional Services

- Office Expenses

- Rent or Lease Payments

- Repairs and Maintenance

- Retirement Plan Costs

- Supplies

- Taxes and Licenses

- Travel, Meals, and Entertainment

- Utilities

Not every deduction applies to every business. For instance, if you have no employees, you can’t claim the employee benefits category. If you run a digital consulting service, you might have no inventory or minimal supply costs. Pick what fits your actual operations, ensuring everything lines up with your bank records.

Detailed Breakdown of Each Deduction Category

A. Advertising

This includes costs to promote your business—like online ads, social media boosts, or local print flyers. Canadian businesses can also write off the design fees for logos or websites, plus promotional freebies. The key is that the ad must target your potential customers. A personal ad unrelated to your business isn’t deductible.

Possible Sub-Items

- Facebook/Google ads

- Print media (flyers, local magazines)

- Sponsorship fees if it specifically promotes your product or service

B. Business Insurance

Insurance that covers your commercial activities (liability insurance, errors and omissions, etc.) is a valid write-off. For instance, a freelance consultant might have professional indemnity coverage, while a small shop owner has commercial property insurance. If you combine personal and commercial coverage, only the business portion is allowed.

Possible Sub-Items

- General liability insurance

- Professional indemnity

- Product liability insurance

(Note: Personal auto insurance for commuting is not typically a business expense unless it’s also for business usage.)

C. Business Startup and Organizational Costs

When you start a business, you might pay for registration, licensing, or initial marketing. You can normally deduct these one-time costs. However, some might be capital in nature—like buying equipment for your new office. Distinguish these from operational expenses to avoid confusion.

Possible Sub-Items

- Registration fees

- Domain name, initial marketing push

- Professional fees for setting up your structure

D. Car and Truck Expenses

If you drive to meet clients or transport goods, you can claim a portion of your vehicle costs. Keep a mileage log to track how many kilometres are for business. Then apply that ratio to fuel, maintenance, insurance, and even depreciation (if you own the vehicle). If you lease the vehicle, you can claim part of the lease expense.

Possible Sub-Items

- Fuel, parking, tolls

- Repairs and maintenance

- Car insurance, registration

- Depreciation or lease costs (pro-rated for business use)

(Be mindful of the “Logbook method.” The CRA expects consistent tracking of business mileage vs. personal.)

E. Commissions and Fees

This covers amounts you pay to external agents, affiliate marketers, or platforms that bring you sales. If you pay someone a percentage for each lead, that’s a commission. If you sell on a platform that charges transaction fees, that might also fall here. For real estate agents or influencers, such fees can be a big chunk.

Possible Sub-Items

- Affiliate program payouts

- Referral fees

- Marketplace selling fees (Etsy, eBay)

F. Contract Labour

You might hire subcontractors or freelancers to help your business. Their pay is deductible if they perform actual tasks that generate income for you. Keep records of what was done and how much was paid. If your contractor is a GST/HST registrant, you pay them the tax, but you might claim input tax credits if you’re also registered.

Possible Sub-Items

- Payment to a freelance graphic designer or web developer

- Wages for a short-term assistant or seasonal help

G. Depreciation

In Canada, we call it “capital cost allowance” (CCA). This is how you split the cost of major assets over several years. Instead of writing off a $5,000 piece of equipment at once, you apply the CRA’s rate (e.g., 20% declining balance) each year. Keep a schedule for these assets so you know each one’s remaining “undepreciated capital cost.”

Possible Sub-Items

- Computers, laptops, printers

- Furniture, machinery, heavy equipment

- Large software packages if classified as capital

H. Employee Benefits

If you have employees (not just contractors), you can write off what you pay for their benefits. This might be health insurance premiums or even contributions to a group RRSP. The entire cost is generally deductible, though the employees themselves must treat certain benefits as taxable. This doesn’t apply if you have no employees or if you only hire freelancers.

Possible Sub-Items

- Group health or dental insurance

- Employee life insurance if part of a standard plan

- Employer’s share of RRSP or pension plan

I. Home Office Expenses

For sole proprietors or small corporations run from home, you can claim a portion of rent/mortgage interest, utilities, home insurance, or property taxes. The portion is typically based on square footage used exclusively for business. If your living room doubles as a workspace, the CRA expects you to treat that carefully. Read more

Possible Sub-Items

- Electricity, heat, water, gas

- Mortgage interest or rent proportion

- Home insurance portion (if not personal coverage alone)

J. Interest Payments

Sometimes you borrow for your business—like a line of credit or a loan used to buy equipment. The interest portion is deductible as long as the funds were used for business. Keep separate personal vs. business loans to show clear lines.

Possible Sub-Items

- Bank loan interest

- Credit card interest if the card is business-only

K. Legal and Professional Services

This covers lawyers, accountants, business consultants, and more. If you pay an accounting firm to manage your books or file your taxes, that’s a legitimate expense. If you see a lawyer for contract drafting, that too is allowable. The key is that the service is needed for your business, not personal issues.

Possible Sub-Items

- Tax preparation fees

- Contract review or drafting

- Consultation with a business attorney

L. Office Expenses

These are standard day-to-day costs for running an office, whether physical or virtual. Think of paper, pens, or a subscription to a printing service. If you buy furniture or major equipment, that might shift to capital costs, but basic office consumables are fine to expense right away.

Possible Sub-Items

- Stationery, postage

- Small office tools like staplers, hole punches

- Minor software subscriptions (if not capitalized)

M. Rent or Lease Payments

This includes renting a storefront, workshop, or warehouse. If you run your business from a space not in your home, you can claim that monthly rent. Sometimes, you might also lease equipment under an operating lease rather than a capital lease. The entire monthly lease expense can be deducted if it’s purely for business.

Possible Sub-Items

- Retail store rent

- Office suite lease

- Equipment lease for monthly usage

N. Repairs and Maintenance

If you fix or maintain business property—like office equipment, a storefront, or a business vehicle—those costs generally qualify. If it’s a major improvement that extends the life or adds to the property’s value (like an extensive renovation), that might need to be capitalized. Routine maintenance, though, is typically an expense.

Possible Sub-Items

- Fixing a broken computer monitor

- Painting the office walls

- Routine car servicing for your business vehicle

O. Retirement Plan Cost

Self-employed people can set up registered retirement savings plans (RRSPs). The contributions are typically personal deductions rather than business costs. However, if you have a group plan for employees or you pay fees for managing your business’s retirement plan, that might be deductible. Confirm with a financial advisor if you mix personal RRSP with business deductions.

Possible Sub-Items

- Administration fees for employee RRSP

- Employer contributions to certain types of group plans

P. Supplies

Many small businesses buy supplies that aren’t big enough to be capital assets. It might be cleaning products for your studio, disposable gloves for a spa, or raw materials for a small craft operation. If an item’s short-lived or quickly used up, it’s an expense. If it’s long-term, it might shift to depreciation.

Possible Sub-Items

- Craft materials, shipping supplies, disposable items

- Maintenance supplies like soap, rags, mops

Q. Taxes and Licenses

This includes special business licenses, local taxes on the business, or certain municipal fees. If you pay an annual fee to the city for operating your store, or a professional license to keep practicing, that cost is typically deductible. Likewise, if you owe business-related property tax on a rented location, that can go here—though if you own property, you might treat that as a separate line item or partial home office cost.

Possible Sub-Items

- Business permit from your municipality

- Professional membership fees to remain licensed

R. Travel, Meals, and Entertainment

Visiting clients, attending conferences, or seeking new deals out of town often leads to travel expenses. Keep receipts for flights, hotels, or local transit. Meals and entertainment typically only allow 50% deduction in Canada if it’s strictly business-related. If you treat a client to dinner, track the date, reason, and who was present.

Possible Sub-Items

- Airline tickets, baggage fees

- Taxi or rideshare to a meeting

- 50% of your restaurant bill for a client lunch

(Some exceptions exist for events or remote sites. Double-check CRA guidelines if you think you can claim 100%.)

S. Utilities

If you rent an office or workshop, the electricity, water, and heating might be separate from rent. Claim that as an expense. If it’s a home office, that portion merges under “home office expenses.” But if it’s a separate shop, you track it as a direct business cost.

Possible Sub-Items

- Gas, hydro, water bills for a leased building

- Phone lines specifically installed at the business location

(Some exceptions exist for events or remote sites. Double-check CRA guidelines if you think you can claim 100%.)

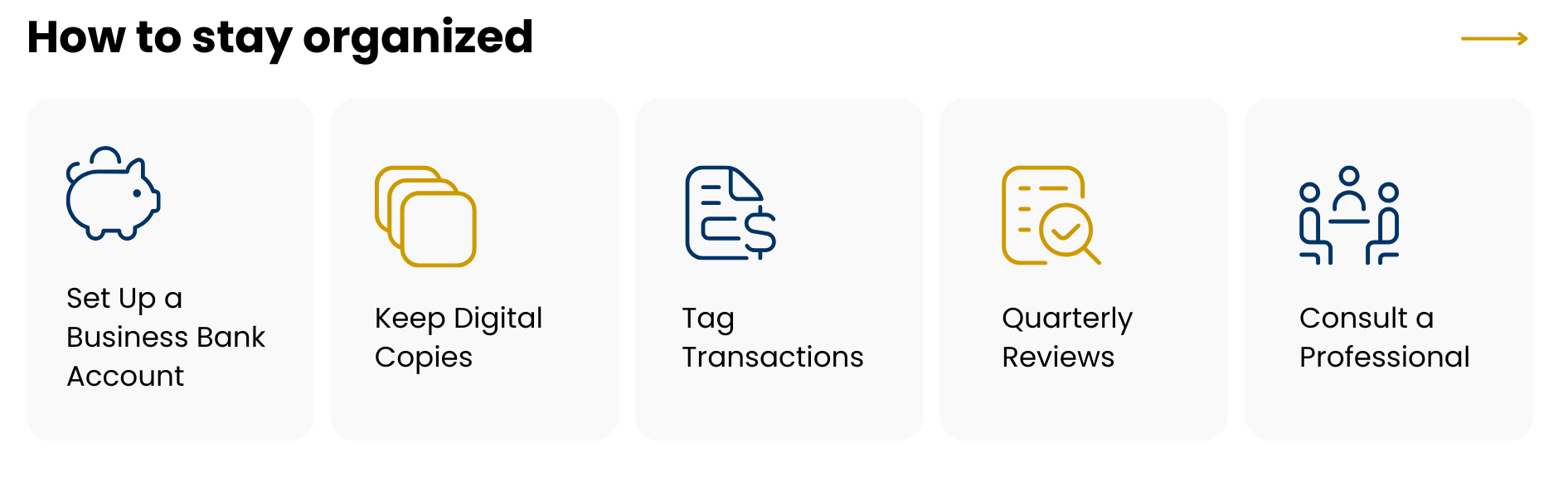

Tips for Staying Organized

- Set Up a Separate Business Bank Account: This stops you from mixing personal expenses with business outlays.

- Keep Digital Copies: Snap photos of receipts on your phone or scan them. Paper fades, but a cloud folder is permanent.

- Tag Transactions: If you use accounting software, tag each expense to a category (like “advertising” or “car expenses”).

- Quarterly Reviews: Evaluate your profit and loss every few months. This practice keeps you from discovering errors right before deadlines.

- Consult a Pro: If your business has many cross-border or complicated scenarios, an accountant can confirm you’re applying CRA rules properly.

Frequently Asked Questions

What is the difference between writing off and deducting an expense?

They’re typically the same concept. “Write-off” and “deduct” mean you claim certain costs on your tax return to reduce taxable income. The CRA uses “allowable business expenses,” but the idea is identical.

Can I deduct 100% of my phone or internet bill?

If your phone or internet is used partly for personal reasons, you must allocate the portion that’s business-related. The same applies to home office utilities, mileage, or anything else with mixed use.

Am I better off incorporating to claim more expenses?

Incorporation has pros (separate legal entity, sometimes better tax rates) but also added complexities (a T2 corporate return, potential payroll). The list of allowable expenses doesn’t change drastically just by incorporating.

Do I need to keep receipts for every item?

Ideally, yes. The CRA can require proof for each claim. Bank statements help, but receipts show details like taxes paid, vendor names, and the exact date.

Conclusion and Next Steps

Self-employment offers independence but also means more responsibility at tax time. By understanding key expense categories—advertising, home office, business insurance, etc.—and systematically recording them, you can reduce your tax burden. Tools like self-employed tax deductions calculators or basic bookkeeping apps show you how each cost impacts your final bill. The trick is consistency: keep logs as you go, store digital receipts, and ensure you use a business bank account for clarity.

Action Items

- Create a categories list: Mirror the main expense headings from the CRA or from the list provided here.

- Adopt monthly or weekly logs: This habit kills last-minute chaos and missed claims.

- Stay updated: The CRA’s rules can shift slightly, especially if new budgets come out or if you pivot your business type.

- Ask for help: If you’re uncertain about complex issues—like partial personal usage or big capital expenditures—seek a qualified accountant or read the official CRA resources.

Long story short: Self-employed Canadians can significantly lower their tax bills by systematically claiming legitimate expenses. With the right approach and a thorough checklist of potential deductions, you’ll walk into tax season with more confidence—and, hopefully, keep more of your earnings where they belong: in your bank account.