Understanding the Nonprofit Statement of Functional Expenses (SOFE): A Canadian Guide

What Is the Statement of Functional Expenses (SOFE)?

The statement of functional expenses (SOFE) is more than just another nonprofit financial report. It’s a detailed breakdown that shows how resources were used—not just where they were spent.

Rather than only listing expense types (e.g., rent, salaries), the SOFE organizes costs by both function (such as programs or fundraising activities) and nature (the type of cost, like salaries or office supplies). This dual structure provides deeper insights into how efficiently a nonprofit organization supports its mission.

In Canada, while not mandatory under Accounting Standards for Not-for-Profit Organizations (ASNPO), functional expense reporting is increasingly used by funders, boards, and auditors as a transparency benchmark.

Why Functional Expense Reporting Matters

Think of the SOFE as a transparency tool. It lets donors and stakeholders assess whether your organization’s mission aligns with how you spend your dollars.

Here’s what functional expense reporting helps with:

- Ensuring accountability to donors and the public

- Demonstrating alignment with mission-critical spending

- Supporting budget planning and grant applications

- Identifying efficiency in fundraising efforts and overhead

This type of nonprofit accountability is vital for maintaining trust and eligibility for grants.

Are you confident your business tax filings are fully optimized and compliant?

Functional vs. Natural Expense Classifications

A key distinction in financial reporting for nonprofits is between functional and natural expense classification:

| Classification Type | What It Answers | Example |

|---|---|---|

| Natural | What was purchased or incurred? | Salaries, Rent, Supplies |

| Functional | Why was it spent? | Program delivery, Fundraising activities, Administrative expenses |

Natural vs functional expense classification isn’t about choosing one over the other—your SOFE combines both.

FASB ASU 2016-14 and the Canadian Context

The U.S. Financial Accounting Standards Board (FASB) introduced ASU 2016-14, which requires functional expense reporting for all nonprofits filing Form 990. While Canada has no such legal mandate, the CRA encourages similar clarity in reporting through T3010 filings.

Canadian nonprofits aiming for international grants—or wanting to meet best practice—should consider aligning with these standards. This helps build credibility with cross-border donors and grant makers.

Breaking Down Key Categories: Program, Management & General, Fundraising

Every expense in a SOFE typically falls into one of three major buckets:

- Program Services: Direct costs tied to your mission (e.g., education programs, shelter operations).

- Management & General: Overhead and admin (e.g., office rent, accounting services).

- Fundraising Expenses: Campaigns, donor communication, event planning.

Understanding and consistently applying these categories is crucial for clean, auditable books.

Functional Expense Allocation Methods for Nonprofits

Not all expenses fit neatly into one function. That’s where functional expense allocation for nonprofits becomes essential.

Here are some allocation methods commonly used:

| Expense Type | Allocation Method |

|---|---|

| Utilities | Square footage usage |

| Salaries | Time spent by employees |

| Supplies | Direct attribution or prorating |

No matter which method you choose, consistency and documentation are non-negotiable.

Personnel and Joint Cost Allocations: Common Pitfalls

Personnel costs usually make up the biggest share of nonprofit expenses. But personnel cost allocation in nonprofits can be tricky.

For example, if an executive director splits time between programming and fundraising, you must estimate the proportion and allocate accordingly—backed by time sheets or management estimates.

Similarly, joint cost allocation in nonprofits (e.g., newsletters that inform and also solicit donations) must follow strict guidance under GAAP and Canadian equivalents.

SOFE vs. Statement of Activities: How They Work Together

The statement of functional expenses and the statement of activities (like a nonprofit’s income statement) complement each other.

| Financial Statement | Purpose |

|---|---|

| Statement of Activities | Shows revenue and expenses over time |

| Statement of Functional Expenses | Shows how expenses were categorized |

This dual reporting paints a fuller picture of both “how much” and “why” money was spent.

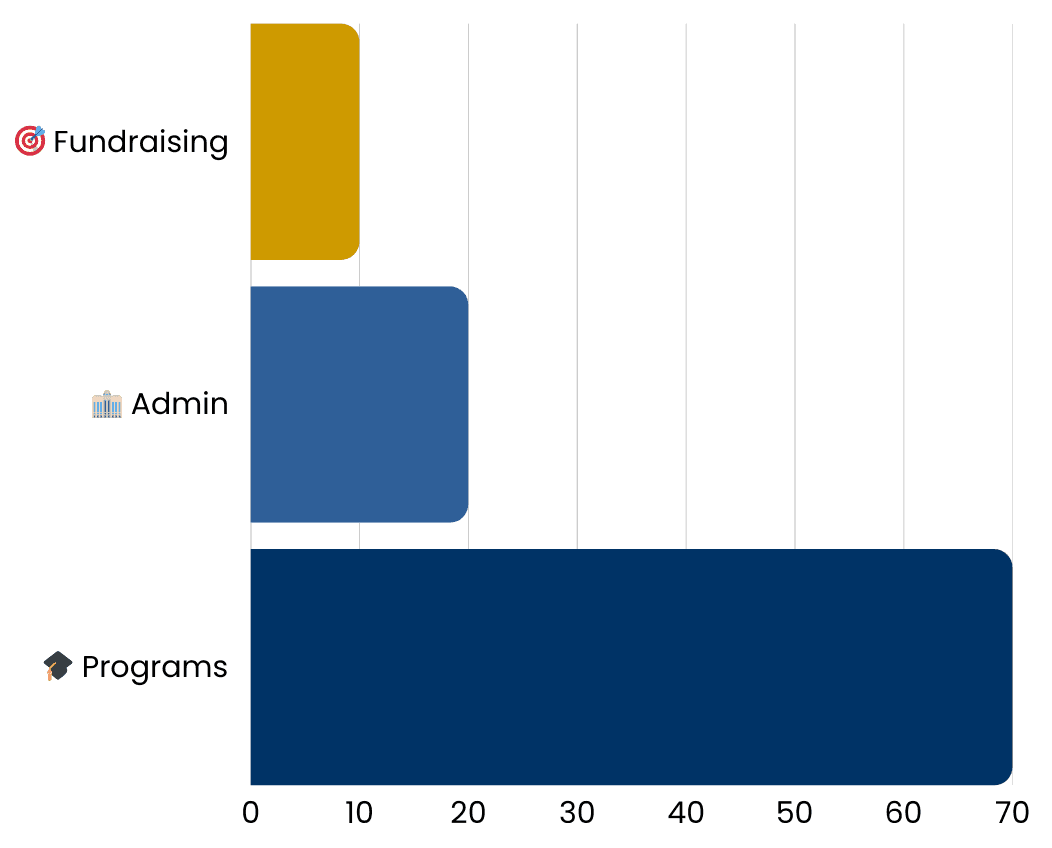

Nonprofit Overhead Ratios and the 65/35 Rule

Funders often look at the nonprofit overhead ratio—how much is spent on admin and fundraising vs. programs.

A popular benchmark is the 65/35 rule:

- 65% or more to program services

- No more than 35% on admin + fundraising combined

But beware: ratios vary by sector, size, and scope. Don’t chase the perfect ratio at the expense of quality infrastructure.

Building a Statement of Functional Expenses Template

A good statement of functional expenses template includes:

- Expense rows by nature (salaries, rent, software)

- Columns for each function: program, admin, fundraising

- Total columns for cross-referencing

| Expense Type | Program Services | Admin | Fundraising | Total |

|---|---|---|---|---|

| Salaries | $200,000 | $50,000 | $30,000 | $280,000 |

| Rent | $15,000 | $5,000 | $2,000 | $22,000 |

Best Practices for Nonprofit Bookkeeping and Expense Reporting

To stay compliant and audit-ready, follow these steps:

- Track expenses in real-time using non profit bookkeeping software.

- Keep source documentation for all allocations.

- Revisit and update your allocation method annually.

- Cross-check SOFE totals with your general ledger and income statement.

Consider outsourcing to professionals familiar with generally accepted accounting principles (GAAP) for nonprofits.

Final Thoughts: Functional Expense Reporting and Accountability

Functional expense reporting isn’t just a reporting formality—it’s a trust-building exercise.

For Canadian nonprofits, especially those looking to scale, attract grants, or operate cross-border, investing in transparent, standards-aligned SOFE practices is a smart move.

It supports mission clarity, enhances credibility, and strengthens your annual report, donor relations, and long-term sustainability.

FAQs

Is the SOFE mandatory for Canadian nonprofits?

Not legally. But funders and auditors often request it, and it’s considered a best practice.

What’s the difference between program and fundraising expenses?

Program expenses support direct mission delivery. Fundraising covers donor outreach, campaigns, and events.

Can I use time estimates for cost allocation?

Yes—but they should be consistent, documented, and preferably backed by timesheets or management oversight.

How do I treat joint costs like mailers that both inform and fundraise?

Follow GAAP or ASNPO guidance—allocate proportionally based on content and intent.

What’s a good nonprofit overhead ratio?

Generally, 65% or more to programs is considered healthy, but it can vary.