Crypto Tax Guide Canada 2026: CRA Rules & Tax Rates Explained

In 2026, cryptocurrency has moved from the fringes to a staple of the Canadian financial landscape. However, as adoption grows, so does the scrutiny of the Canada Revenue Agency (CRA). If you are buying, selling, staking, or mining digital assets, navigating this tax season requires more than just basic record-keeping—it demands a strategic understanding of shifting legislative thresholds and global transparency standards.

The CRA views cryptocurrency as a commodity, not a legal currency. Consequently, every “disposition”—from swapping Bitcoin for Ethereum to using a stablecoin for a coffee—is a taxable event.

How Cryptocurrency Tax Works

Your tax obligations are determined by the nature of your interaction with digital assets. The CRA generally classifies crypto income into two distinct categories:

Capital Gains: For most casual investors, profits are treated as capital gains. You buy an asset, hold it, and sell it later. Under current 2026 rules, you only pay tax on a portion of this profit.

Business Income: If you trade frequently (day trading), use specialized hardware for industrial mining, or promote crypto services, the CRA may view your activity as a business. In this scenario, 100% of your profits are taxable.

Orbit Advisor Tip: The line between “investor” and “trader” is a high-audit area. The CRA analyzes transaction frequency, period of ownership, and “badges of trade.” At Orbit, we help you determine the most tax-efficient classification before the CRA does.

Identifying Capital Gains and Losses

A gain occurs when you sell your cryptocurrency at a price higher than your Adjusted Cost Base (ACB)—the original purchase price plus any acquisition fees.

The 2026 Inclusion Rate Rule:

For individuals, the first $250,000 of annual capital gains are taxed at a 50% inclusion rate. However, for any gains exceeding that $250,000 threshold (and for all capital gains realized by corporations), the inclusion rate increases to 66.67%.

Example:

If you purchased Ethereum for $2,000 and sold it for $5,000, your capital gain is $3,000.

If you are under the $250,000 threshold, $1,500 (50%) is added to your taxable income.

If you have already surpassed the threshold for the year, $2,000 (66.67%) becomes taxable.

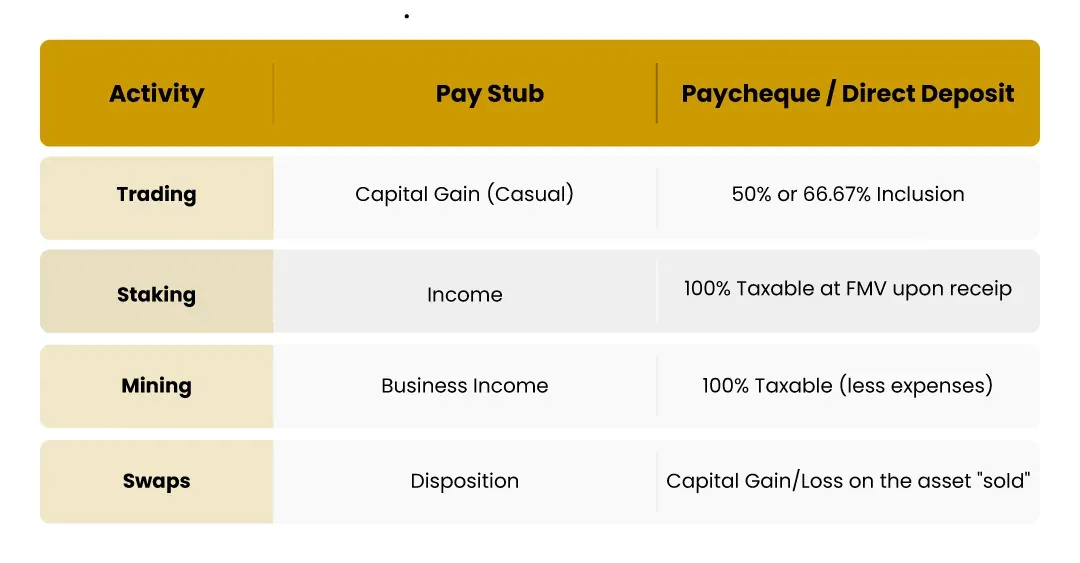

Trading, Staking, and Mining

Not all activities involving cryptocurrencies are taxed the same way. The CRA (Canada Revenue Agency) treats each of the following categories differently for tax purposes as outlined in the chart below.

The CRA treats different activities with distinct rules:

Staking Rewards: These are taxed as income at the Fair Market Value (FMV) on the day you receive them. If you later sell those tokens at a higher price, you trigger a secondary capital gain event.

Mining: While “hobby mining” may receive capital gains treatment, any operation with commercial intent or significant overhead is treated as business income.

Swaps: Trading one crypto for another is considered a sale of the first and a purchase of the second. You must record the CAD value at the exact moment of the trade.

Setting Up Your Records

It’s essential to maintain proper documentation of your crypto taxes as required by the Canada Revenue Agency (CRA). You must document the date, amount, wallet address, exchange details and value in Canadian dollars of each of your transactions.

You must also document any fees incurred while transacting through exchanges; these can be used to offset any gains when calculating taxable gains. Many individuals choose to use crypto-tracking software to manage their records easily. Having appropriate records will enable you to accurately determine all your gains/losses and provide protection during an audit while also making the process of filing your tax return less stressful.

Real-World Example: Crypto Gains in Action

Rahul, a Toronto-based investor, realizes a $300,000 capital gain from selling Bitcoin in 2026.

The first $250,000 is taxed at the 50% rate ($125,000 taxable).

The remaining $50,000 is taxed at the 66.67% rate ($33,335 taxable).

Total Taxable Income: $158,335.

If Rahul had $10,000 in capital losses from a previous trade, he could subtract that $10,000 from his $300,000 gain before the inclusion rates are applied, significantly lowering his bill.

Key CRA Regulations for 2026

The CRA has increased the requirements for reporting income through 2025, 2026. Crypto exchanges are now required to provide user information to CRA in order for CRA to track unreported income.

Income arising from cryptocurrencies must be reported on an individual’s annual tax return. Capital gains from holding cryptocurrenices will be reported on Schedule 3 and business income will typically be reported as self employment income. If you do not report cryptocurrency Income, you could be subject to penalties, interest and audits. In addition, CRA requires taxpayers to report worldwide holdings of cryptocurrencies that exceed certain dollar thresholds and/or other regulations. It is very important to clearly follow these rules to avoid any future issues.

Conclusion

2026 is the year of transparency. While the higher inclusion rates and CARF reporting standards add complexity, they also provide a clear roadmap for compliance. At Orbit Accountants, we specialize in bridging the gap between complex blockchain data and CRA-ready filings. Whether you need an ACB reconciliation for thousands of DeFi trades or strategic advice on corporate holdings, we provide the clarity you need to grow your portfolio.

Would you like me to help you calculate the specific tax liability for a hypothetical trade using the new 2026 inclusion rates?

FAQs

Do I pay tax if I just move crypto between my own wallets?

No. Transfers between wallets you own are not “dispositions.” However, keep a record of the transfer fees (gas), as they can be added to your cost base.

Can I use crypto losses to lower my employment income tax?

Generally, no. Capital losses can only offset capital gains. However, they can be carried back three years or forward indefinitely to offset future gains.

Is every NFT sale taxable?

Yes. If you are a creator, it is typically business income. If you are a collector, it is usually a capital gain or loss.

Disclaimer: This article is for informational purposes only and does not constitute professional tax, legal, or accounting advice. Inclusion rates and CARF requirements are subject to specific individual circumstances. Always consult with a qualified professional at Orbit Accountants.