Year-End Bookkeeping Checklist

The finalization of a company’s accounting books at the end of the year provides essential information regarding the performance of a business during that year. This enables management to make informed decisions; it also minimises tax liabilities. An accurate Year-End bookkeeping checklist ensures all transactions, reports and documentation have been reviewed and cleared prior to the closing of the books for a specific year.

In this blog post we will provide you with a comprehensive and straightforward Year-End checklist for bookkeeping purposes, allowing bookkeepers to keep their companies in order, compliant and ready for future profitability.

Why Year-End Bookkeeping Matters

As the financial year draws near an end, it is critical to undertake year-end bookkeeping for any business. During this process, each entry must be made accurately, resulting in an accurate reflection of the actual financial state of your business. Year-End bookkeeping is also vital for compliance with applicable taxes as discussed above; it will also enable better financial planning for 2022. If the Year-End closing is not done correctly, there would likely be confusion regarding reports and other issues conceivably if filing taxes

Step-by-Step Year-End Bookkeeping Checklist

Year-End bookkeeping follows sequentially from step to step. Each task is related and will move to the next. Follow the steps to ensure everything is included and your final records will be ready for tax season.

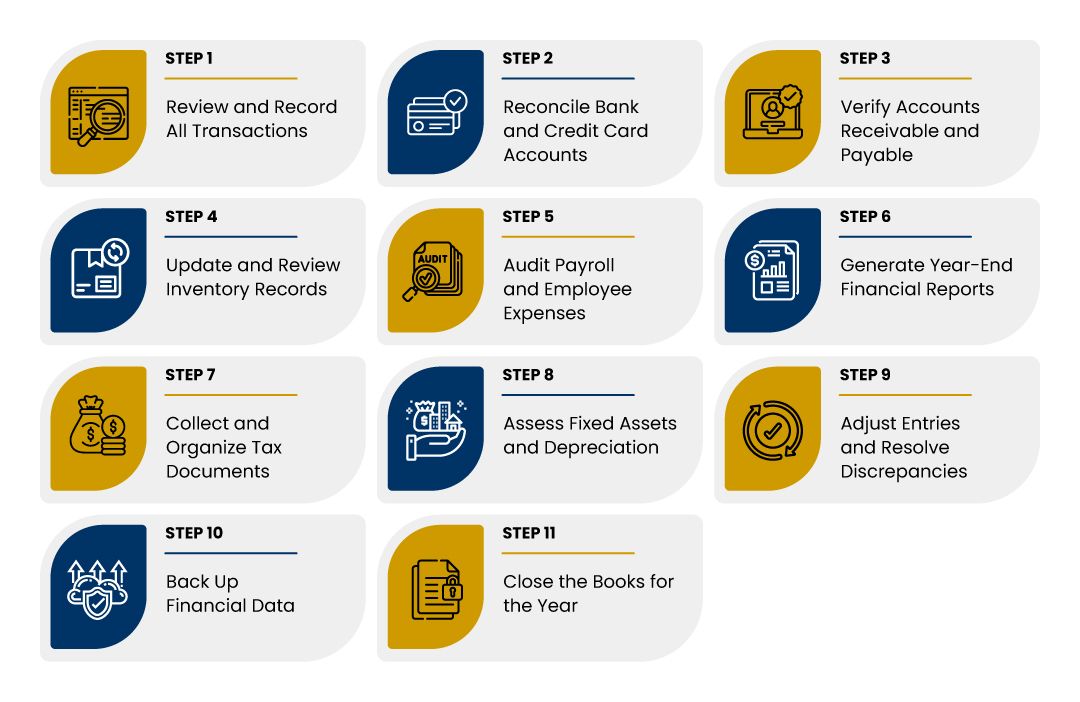

Review and Record All Transactions

You first want to check that every transaction your business did was recorded; revenue, expense, interest, vendor payments, and fees charged by your bank are all things you need to be sure were captured properly. One error such as missing just one small item could mean the difference between being in the red and in the black; therefore, look through all receipts, invoices, and bank statements for accuracy.

Reconcile Bank and Credit Card Accounts

Reconciliation is the process of verifying that the company’s bank and credit card records correctly match its internal bookkeeping records (e.g., journal entries). Reconciliation provides a way to identify any discrepancies in accounting records that could be caused by duplicate entries, unrecorded bank charges and/or missing expenses.

Verify Accounts Receivable and Payable

Next, check outstanding invoices you are yet to receive payment for and bills you still need to pay. Clearing up these numbers ensures your year-end financial reports show accurate totals for money owed and money due.

Update and Review Inventory Records

If your business handles products, perform a physical inventory count. Compare this with your digital records. Adjust the numbers if items are damaged, missing, or outdated. Accurate inventory tracking impacts your tax calculations and profit reports.

Audit Payroll and Employee Expenses

Employees’ salaries and the amounts paid to them (e.g., bonuses, benefits, etc.), as well as the amounts reimbursed to employees (e.g., travel, business travel, entertainment expenses, etc.) need to be reviewed annually to ensure the information in employee payroll files agrees with the information in the company’s accounting records. Incorrect payroll records can result in non-compliance with applicable employment regulations and have serious ramifications with respect to tax returns.

Generate Year-End Financial Reports

Financial reports that must be prepared at year-end include the company’s income statement, balance sheet, and trial balance; these reports provide insight into your company’s profitability and/or losses, what it owns, what it owes, and what its total net worth is. Furthermore, these reports are the basis for a taxpayer’s federal income tax return.

Collect and Organize Tax Documents

Gather all documentation necessary to file your taxes, including, but not limited to, receipts, T4’s, invoices, bank statements, payroll summaries and vendor forms. By keeping them organized in one place, you will save time later and avoid having to search at the last minute for what you need.

Assess Fixed Assets and Depreciation

Evaluate your business’ fixed assets (machinery, equipment and vehicles) and update the depreciation calculations for the current year. This process will ensure that your financial statements accurately reflect the value of your fixed assets.

Adjust Entries and Resolve Discrepancies

Make any necessary adjustments for errors, accruals, prepayments and depreciation adjustments. Performing your adjustment entries at the end of the year will provide you with a complete and accurate set of books prior to closing the books for the year.

Back Up Financial Data

At all times, be sure to back-up your bookkeeping files. Whether digitally or in paper, your financial data needs to be stored securely to protect your business from the possibility of loss due to damage, system failure, etc.

Close the Books for the Year

Once you have verified, verified and made any necessary corrections, you can formally close your books. By closing the books, you lock-in the current year’s financial data and prepare the bookkeeping system for the new year.

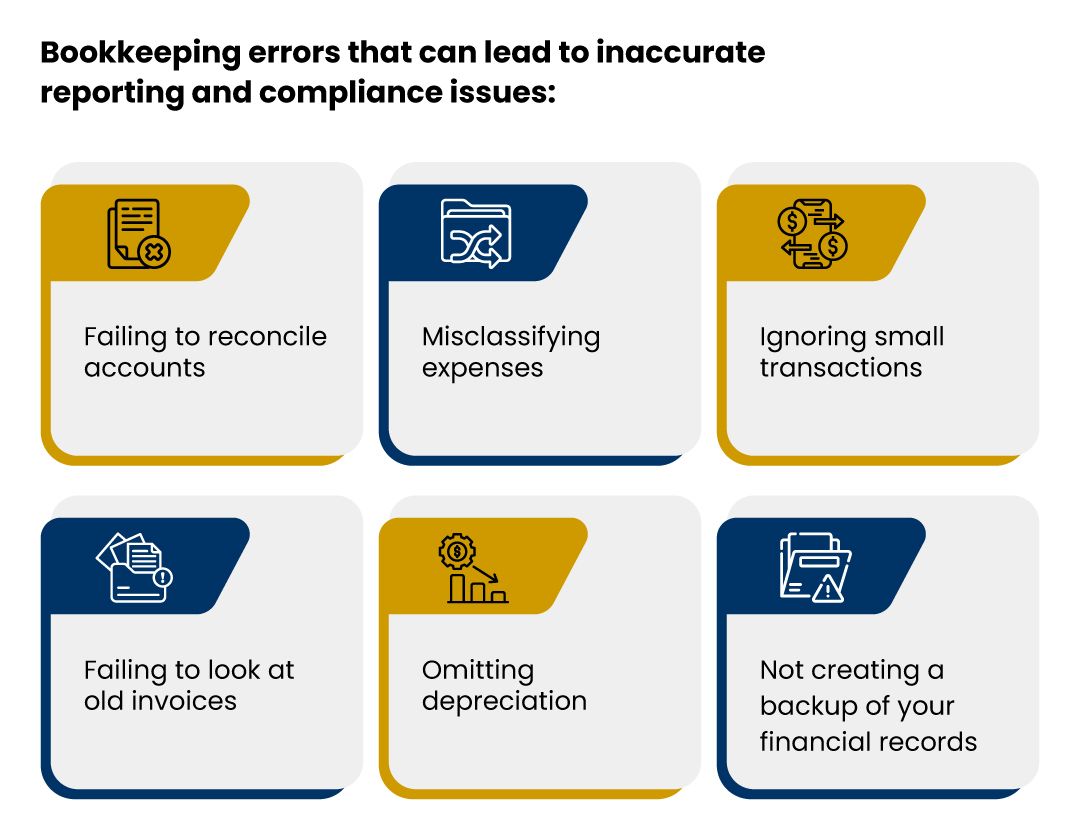

Common Year-End Bookkeeping Mistakes to Avoid

As businesses get ready to close out the year, they are likely to make some bookkeeping errors that can lead to inaccurate reporting and compliance issues. Examples of typical problems include: failing to reconcile accounts, misclassifying expenses, ignoring small transactions, failing to look at old invoices, omitting depreciation, and not creating a backup of your financial records. Many of these errors can easily be avoided, thus saving you time, easing your stress, and keeping your records clean.

When to Hire a Professional Bookkeeper

For some businesses, especially those that are expanding or those that have owners who are busy, year-end bookkeeping can be overwhelming. When you have messy records, have fallen behind in updating your records, or just find yourself lost navigating through the tax preparation process, it may be beneficial for you to hire a professional bookkeeper. At Orbit Accountants, we provide bookkeeping solutions that are accurate, compliant, and efficient, giving you the confidence to focus on your growth as a business. With Orbit Accountants, you can eliminate your need to keep complex spreadsheets and paper records for your bookkeeping activities. Using cutting-edge cloud-based accounting software, we can integrate your bank feeds, track your expenses, and provide you with year-end financial statements that are tax-ready, allowing you to complete your year-end bookkeeping hassle-free.

Frequently Asked Questions

Why is it important to reconcile accounts at Year-End?

Reconciling your records with the actual activity in your bank account helps ensure that the accuracy of your year-end financial statements.

Which financial reports should be generated during the Year-End close?

The primary reports you generate for a complete overview of your company’s financial position include an income statement, balance sheet, trial balance, and cash flow statement.

How do I prepare my books for taxes at Year-End?

To prepare yourself for a successful year-end (and tax preparation), you must compile your receipts, enter your journal entries, review your accounts, create and maintain your monthly/quarterly financials, and prepare your economic reports for tax purposes.

What are common mistakes during Year-End bookkeeping?

Common mistakes are incorrectly entered transactions, unrecorded transactions, incorrectly classified transactions, missed invoices, and skipped adjustments.