Sole Proprietorship Taxes in Canada: A Guide and Overview

Cryptocurrency remains popular in Canada, but sorting out your taxes on crypto can feel like a maze. Many investors don’t realize that gains, losses, or even certain crypto transactions may be subject to Canadian tax law. If you’re unsure how to handle your crypto trader tax obligations, this guide is here to help. We’ll look at CRA regulations, how capital gains or losses apply, and ways to manage your digital assets in the 2025 tax year. Whether you’re curious what is crypto taxes, or need crypto tax services, the information below offers clarity.

Understanding Sole Proprietorship in Canada

A sole proprietorship in Canada involves operating under your own name (or a registered trade name), with no legal separation between personal and business assets. This structure’s ease appeals to many entrepreneurs, but it also ties your business income to your personal tax return. There is no separate corporate tax return or unique business tax rate—everything merges on your T1.

Why People Choose It:

- Low startup costs and minimal paperwork.

- Full control over profits and decisions.

- Straightforward dissolution if you want to stop or pivot the business.

Are you confident your business tax filings are fully optimized and compliant?

Potential Risks:

- Unlimited personal liability for any debts or lawsuits.

- Harder to raise capital compared to a corporation.

- Without distinct legal status, expansions or major investments can become complex.

Basic Tax Obligations for Canadian Sole Proprietors

As a sole proprietor, you report all revenue, minus eligible expenses, on your personal tax return. The net amount is added to your personal income, which could raise your overall tax bracket. Additionally, you may collect GST/HST if your revenue exceeds $30,000 in four consecutive calendar quarters.

Key Documents:

- T1 General Return: Your main personal income tax form.

- Form T2125 (Statement of Business or Professional Activities): Used to declare business income and expenses.

- GST/HST Return: If you’re registered, file regularly (often quarterly) to remit or claim back sales tax.

Paying taxes generally means calculating your net income, applying relevant personal tax credits, and settling any balance by the personal tax deadline (usually April 30 for most taxpayers). If your business is large enough, you might make quarterly instalments.

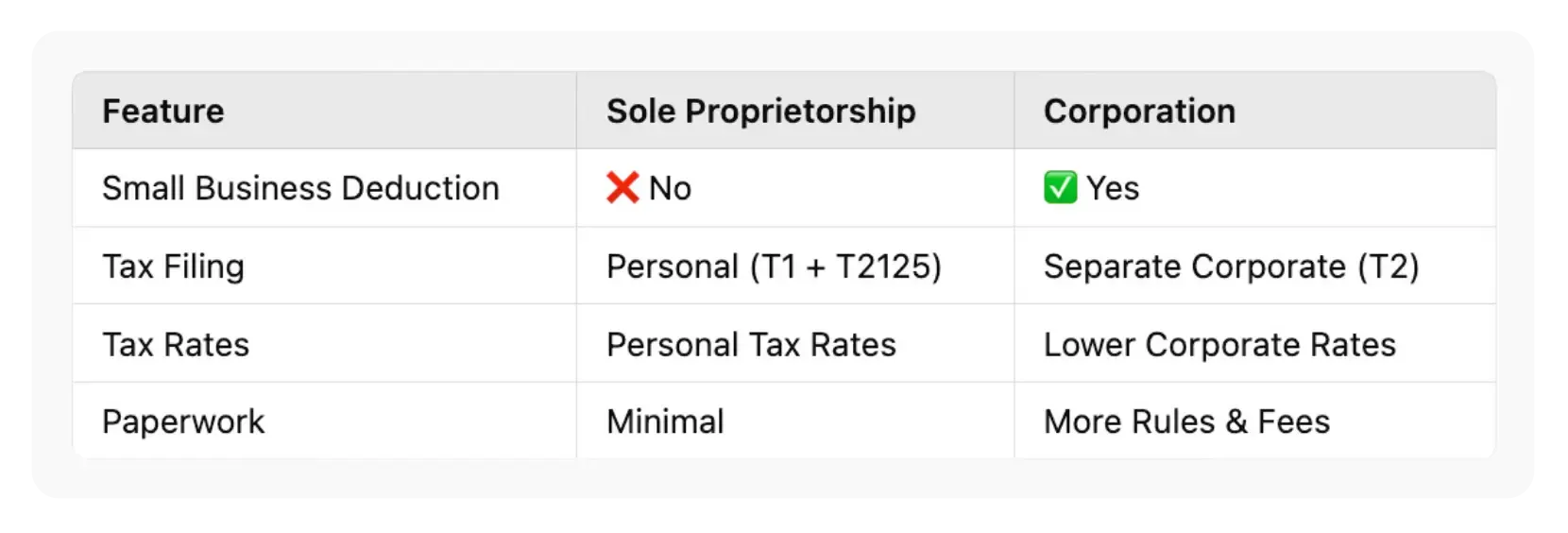

Comparing Sole Proprietorship vs. Corporations

Unlike a corporation, a sole proprietorship does not have its own distinct legal identity. Here is how that plays out:

Corporate Route:

- Files T2 corporate tax returns.

- Access to the small business deduction if qualified.

- Pays corporate taxes at a lower rate on active business income up to a limit.

- Requires more paperwork, such as annual returns, possible audit reviews, and separate accounting.

Sole Proprietorship Route:

- Merges business income with personal return (T1).

- Has no access to the small business deduction—only corporations can claim it.

- May pay higher personal tax if profits are large.

- Less administration and easier day-to-day recordkeeping.

The small business deduction is a key differentiator. It lowers the corporation’s tax on the first chunk of active income, often up to $500,000. A sole proprietor cannot tap into that. Still, for many new or smaller ventures, the simpler structure outweighs those potential savings.

Small Business Deduction: Who Benefits and Why

What It Is:

The small business deduction is a special corporate tax break that lowers the rate on active business income for qualifying Canadian-controlled private corporations. Since sole proprietors are not corporations, they do not get this direct deduction. Instead, profits are fully taxed at personal rates.

When It Could Matter:

If your sole proprietorship is generating sizeable profits, you might wonder if incorporation would reduce your tax. Incorporation could allow you to split income or take advantage of the small business deduction, but it comes with extra obligations and might not be worth it for modest incomes. For some, staying a sole proprietor remains cheaper overall, given that corporate compliance can be expensive.

Recordkeeping and Accounting

Why Good Records Matter:

In a sole proprietorship, personal and business finances can blur. To maintain clarity, set up a separate bank account for business transactions. Use simple accounting software to track every sale and purchase. Save receipts for all business expenses, from advertising to office supplies, so you can claim them at year-end.

Core Recordkeeping Tips:

- Track GST/HST: If you must charge sales tax, note it separately in your bookkeeping.

- Keep Digital Copies: Scanning receipts or taking photos cuts down on physical clutter.

- Categorize Expenses: Group costs under marketing, vehicle, rent, home office, etc., to make T2125 simpler.

By dedicating a bit of time each month to update your financial data, you’ll have a clearer picture of your business performance, and a breezier tax filing come spring.

Home-Based Business Expenses

Working from home is common for a sole proprietor, but you need to separate the personal portion of your bills from the business portion. For instance, if a home office takes up 10% of your home’s square footage, you might claim 10% of rent, utilities, or mortgage interest as business expenses. However, ensure it’s used primarily for business or you risk pushback from the Canada Revenue Agency.

Examples of Home Expenses:

- Rent or Mortgage Interest: If you rent a two-bedroom and one room is exclusively for business, you might claim half that portion.

- Property Taxes: A portion is deductible if it ties to your workspace.

- Utilities (Heat, Electricity, Internet): Adjust for business usage.

- Home Insurance: The business part of your premium might be written off.

Keep a detailed floor plan or log how many hours the space is used for business if it’s shared. The CRA expects a well-documented approach.

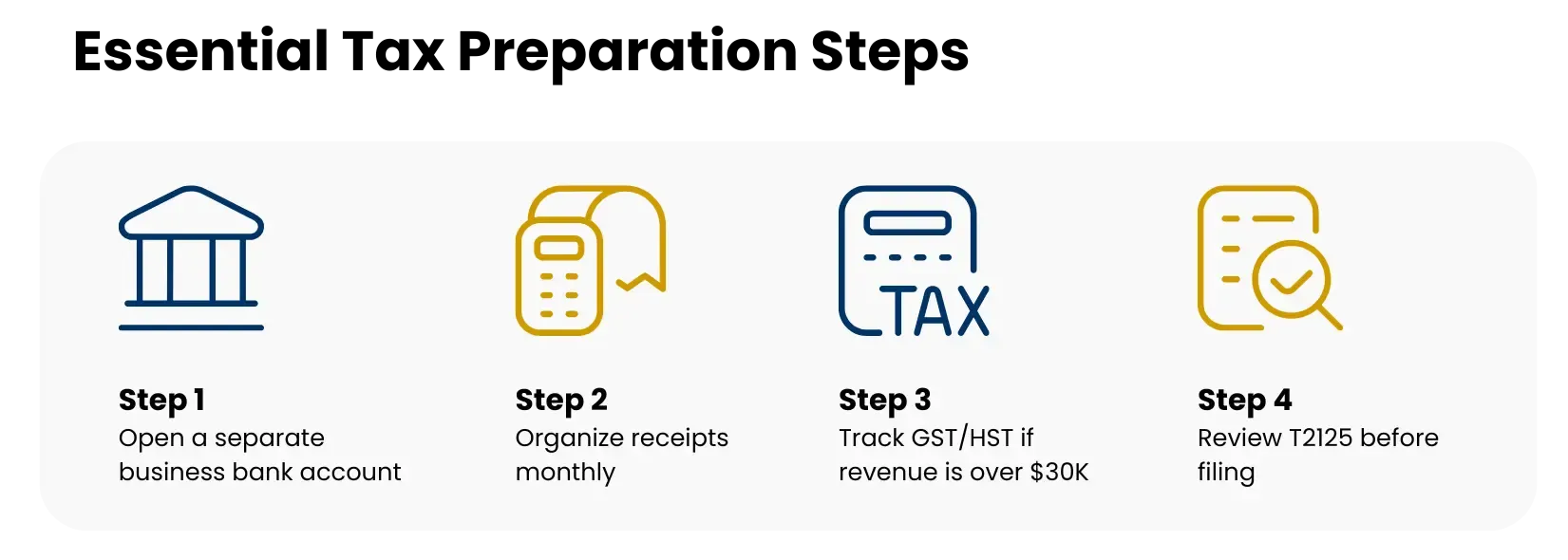

Step-by-Step Filing Process

Step 1: Gather Records

Start by collecting all receipts, bank statements, and relevant documents. If you charge GST/HST, ensure you have a record of how much you collected and paid out.

Step 2: Separate Income from Employment

If you have a day job plus your sole proprietorship, the T4 from your employer covers your regular employment income. Your business income goes on T2125 or a similar schedule, which merges with your personal return.

Step 3: Calculate Net Income

Total business revenue minus legitimate expenses is your net profit. That figure merges into your T1. Keep an eye on any capital expenditures, which might need depreciation over time (Capital Cost Allowance).

Step 4: Fill Out Required Forms

Besides T2125, watch for any local forms that your province may require for certain credits or specialized aspects like RST (Retail Sales Tax) in some jurisdictions.

Step 5: Submit by the Deadline

Canadian personal tax returns usually need to be filed by April 30. If your business is a sole proprietorship, you might receive a later filing deadline (often June 15), but any balance owing is still due by April 30 to avoid interest. Read more about When Are Corporate Taxes Due? Deadlines for 2025.

Step 6: Pay Taxes Owing

Set aside money for taxes throughout the year. If you owe more than a certain threshold, you might need to make quarterly instalments to avoid late payment interest.

Conclusion

A sole proprietorship in Canada remains the simplest way to operate for countless entrepreneurs, contractors, and side-hustlers. The main difference from a corporation is that your profits flow directly to you, and you file a single personal tax return. There is no direct access to the small business deduction, but the minimal red tape often compensates.

Staying on top of your tax responsibilities means good recordkeeping, separating personal from business finances, and knowing key deadlines. If your enterprise grows large or you face liability concerns, you might consider incorporation to tap into potential corporate tax advantages. But for many, the streamlined approach suits them well. The most important piece is ensuring that every sale, expense, or home office cost is properly tracked and declared, so that come tax time, you can confidently file everything on one unified return. With the right habits and a plan for expansions or bigger goals, a sole proprietorship might be the perfect launchpad for your business journey.

Frequently Asked Questions

What are sole proprietorship taxes?

Sole proprietorship taxes refer to the personal income tax you pay on your business profits. Unlike a corporation that files a separate T2 return, a sole proprietor merges business income with personal tax forms (like T2125).

What forms do I need when filing taxes as a sole proprietor?

You usually file a T1 return and include a T2125 (Statement of Business or Professional Activities). If you charge GST/HST, you submit those returns either monthly, quarterly, or annually, depending on your revenue.

How does a sole proprietorship pay taxes compared to other business structures?

Sole proprietors report all revenue under personal taxes, so they pay at personal rates. A corporation, by contrast, files its own return, potentially benefiting from the small business deduction. But corporations face more rules and fees.

Do I need a separate tax ID for my sole proprietorship?

You may need a Business Number (BN) if you must register for GST/HST. Many sole proprietors don’t need a separate “corporate” ID because they’re unincorporated, but it depends on local regulations or whether you employ people.

Can I file personal and business taxes together as a sole proprietor?

Yes. In fact, that’s exactly how it works. Your business income merges with personal income on a single T1, with specific schedules for business. You just need to keep thorough records to separate them accurately.