Salary vs. Dividends in Canada

If you own a Canadian corporation, you’ve likely asked yourself how to best take money out. You might be wondering “dividends vs salary Canada,” or searching for a “salary vs dividends Canada calculator.” Perhaps you’re a company director pondering “how do I pay myself dividends,” or you’re a professional corporation owner who wants to know “how to move money out of a professional corporation.” This in-depth guide walks you through dividends vs salary—why it matters, when each option is best, and what happens if you don’t pay corporation tax on time.

We’ll explore how to pay yourself from your corporation in Canada, how to pay yourself in dividends, and whether you should rely on a salary vs dividend approach. We’ll also review the dividend tax rate in Alberta (and how it compares to other provinces) and highlight some best practices for business owners. By the end, you’ll have a clearer picture of how to pay yourself from your business in a way that aligns with your goals, personal financial needs, and tax obligations.

1. Introduction: Why Compare Dividends vs Salary Canada?

Running a corporation in Canada gives you options for how to draw personal income. You can take a T4 wage or declare dividends as a shareholder. Each method involves distinct tax rules, compliance requirements, and implications for your finances.

- Tax Efficiency: Dividends often have lower personal tax rates, but your corporation needs after-tax profits to pay them.

- Personal Budgeting: Salaries offer predictable pay, which might matter for mortgages or monthly bills.

- Retirement Benefits: Paying yourself a salary contributes to the Canada Pension Plan, while dividends do not.

If you’re not sure whether to pay yourself with salary or dividends, or you keep searching “salary vs dividends Canada,” you’re not alone. This guide untangles these choices and explains how to decide what’s best for you.

2. Key Concepts: Salary vs Dividend, T4 vs Incorporated

Before diving deeper, let’s clarify:

- Salary: A wage paid to yourself. The corporation deducts it as an expense and issues you a T4 slip. You pay personal income tax on this salary, and you or the corporation must handle CPP and possibly EI.

- Dividends: Payments of corporate profits to shareholders. After the corporation pays its own taxes, it can distribute dividends. You then report them on your personal return, often at a lower rate due to the dividend tax credit.

- T4 vs Incorporated: T4 references the slip used for employment income. Being “incorporated” means you have a corporation. As a shareholder, you can choose how to extract your share of the business profits—via dividend or wage.

3. Pros and Cons Overview

The debate of dividend vs salary can be boiled down to a few key considerations. Here’s a quick look:

| Factor | Salary (T4) | Dividends |

| Tax Treatment (Personal) | Fully taxed at marginal rates | Eligible for dividend tax credit, often lower rates |

| Corporate Income Reduction | Lowers corporate taxable income | Paid from after-tax profits, no extra corporate deduction |

| CPP Contributions | Salaries trigger CPP premiums, building retirement benefits | No CPP contributions (can save money now, but less for retirement) |

| RRSP Contribution Room | Salary counts as earned income, increasing RRSP room | Dividends do not create RRSP room |

| Complexity | Requires payroll setup, source deductions, T4s | Dividend issuance + T5 forms, requires after-tax profits |

| Cash Flow Predictability | Provides steady, budget-friendly income | Can be lumpy or irregular, depending on corporate profits |

| Administrative Effort | Ongoing payroll remittances, monthly or quarterly CRA submissions | Periodic resolutions for dividend declarations, simpler monthly flows |

| Suitability | Ideal for consistent living expenses, pension building | Good for flexible, tax-efficient payouts if corporate profits exist |

4. Tax Implications (with Table)

When deciding “how do i pay myself a dividend” or “how do i pay myself from my business,” personal and corporate taxes both matter:

| Aspect | Salary | Dividends |

| Corporate Tax | Lowers corporate profits, so you pay less corporate tax | Paid from profits already taxed in corporation, no further reduction |

| Personal Tax Reporting | T4 slip; reported as employment income | T5 slip; reported as dividend income |

| Marginal Tax Rate | Can be higher if your personal salary is large | Usually lower due to dividend tax credit, but net effect depends on integration |

| Dividend Tax Rate Alberta etc. | Not applicable as you’re paying salary | Varies by province; “dividend tax rate Alberta” might differ from Ontario or BC |

| Payroll Deductions | Required (CPP, sometimes EI) | None for dividends |

| Potential for Tax Splitting | Salary can’t bypass restrictions easily | Dividends to family members used to be common, but post-2018 rules limit this |

Combining these points helps you see if a salary or dividend approach minimizes your total tax bill.

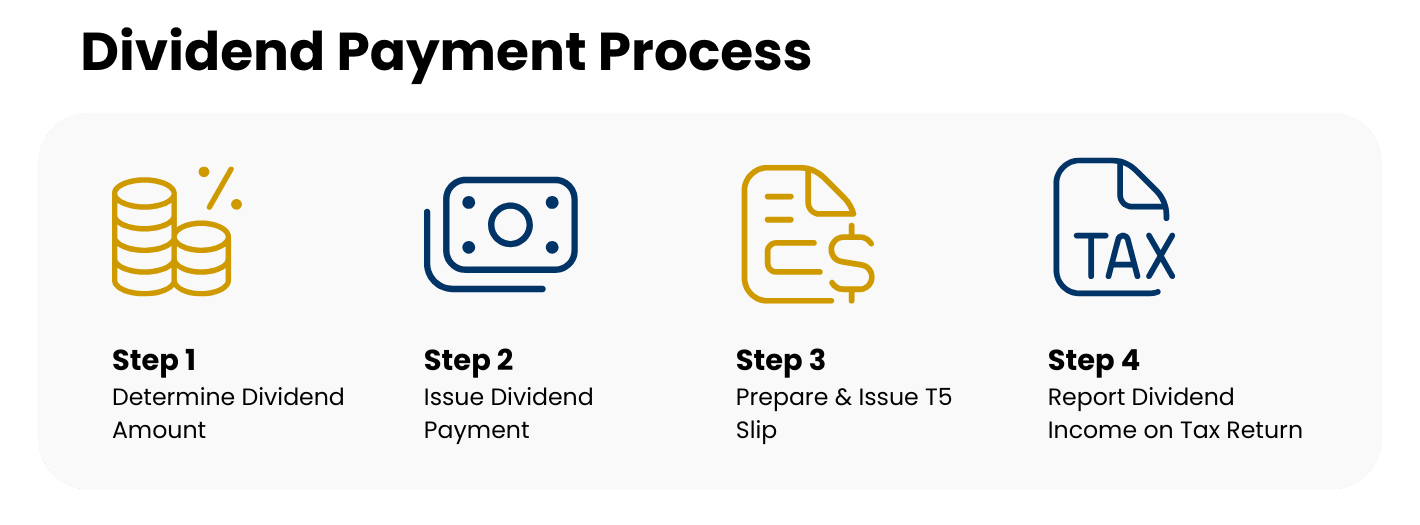

5. How to Pay Yourself Dividends from Your Corporation in Canada

If you lean toward “dividends vs salary Canada,” focusing on dividends, you’ll need to declare them properly:

- Check Profit and Retained Earnings: Dividends must come from after-tax corporate profits, either current or past retained earnings.

- Board Resolution: Directors (even if it’s just you) must sign a resolution stating an amount of dividend per share.

- Record in Corporate Ledger: Update your minutes and note the new balance of retained earnings.

- Disburse Funds: Transfer cash to your personal account or record it as a shareholder loan if you’re not taking the money immediately.

- Issue T5: At year-end, file a T5 slip for each shareholder receiving dividends.

If you skip these steps, the CRA might see the payouts as unreported salary or a shareholder loan with potential tax consequences. Many small corporations prefer monthly or quarterly dividends if the business is stable.

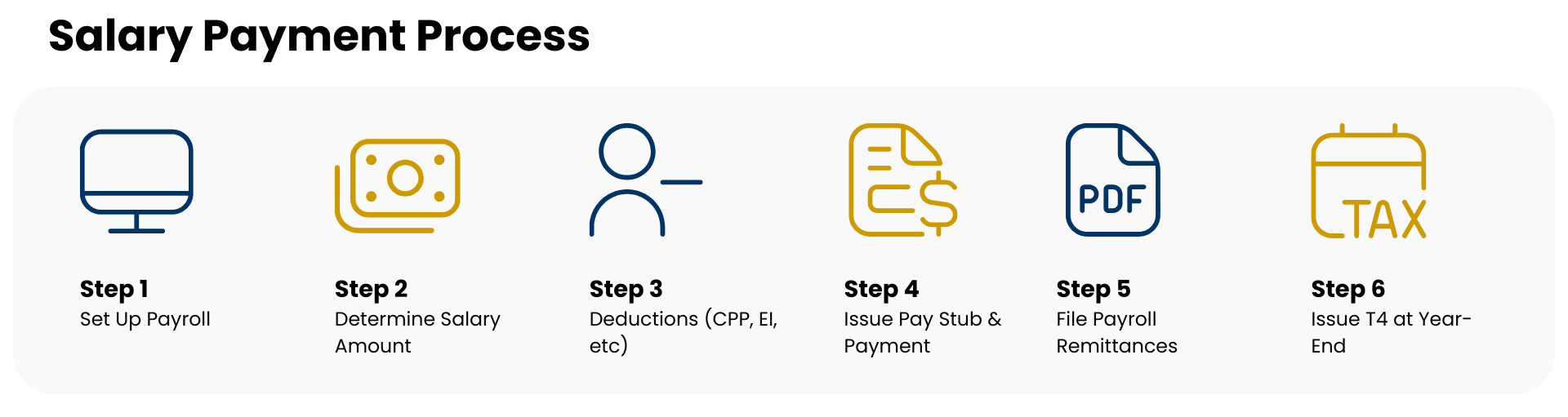

6. How to Pay Yourself a Salary

If “how do i pay myself from my business” points you to a salary, the process is:

- Set Up Payroll: Register for a payroll account with the CRA.

- Decide Wage: Choose an amount that covers your personal needs but still leaves your corporation able to pay bills and taxes.

- Withhold Taxes, CPP, Possibly EI: Each pay cycle, deduct these amounts from your gross pay.

- Remit Source Deductions: Send them to the CRA monthly or quarterly.

- Year-End T4: Provide yourself a T4 slip showing total wages, taxes withheld, and CPP contributions.

This route is straightforward if you want a predictable monthly deposit, but it involves more ongoing compliance. That said, many owners prefer the stability and the forced CPP contributions that come with a T4 wage

7. Salary vs Dividends Canada Calculator: Is It Enough?

You might see a “salary vs dividends Canada calculator” online. These tools:

- Estimate net personal income by factoring in corporate taxes and personal taxes.

- Assume certain average rates or integrated tax approaches.

- Often ignore unique personal details like spousal income, child benefits, or corporate carry forward losses.

They can provide a ballpark figure for “salary vs dividends.” But for serious decisions—like large expansions or retirement plans—meeting with an accountant is safer. The right approach can shift yearly based on changing rules and personal circumstances.

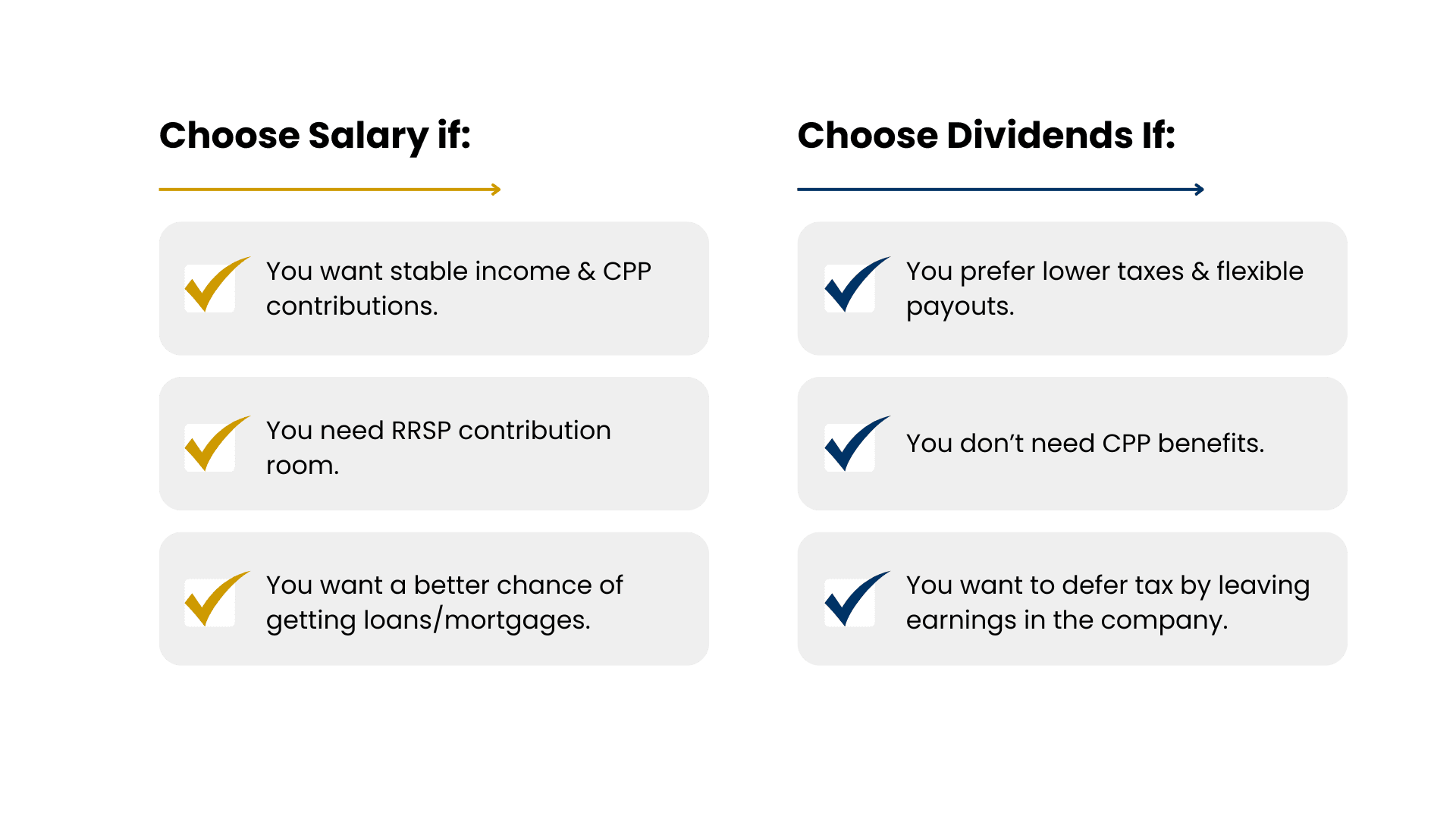

8. When Dividends Might Be Better

- Simplicity: If you dislike monthly remittances, dividends are less frequent, though you must do official declarations.

- High Corporate Profits: If your corporation has robust after-tax profits, dividends might be tax-efficient.

- Lower Personal Tax: “Dividend vs salary Canada” discussions often highlight that dividends can see lower rates.

However, consider that no CPP accumulates from dividends. If retirement is far off or you have other retirement savings strategies, this might be a trade-off you accept.

9. When Salary Might Be Better

- CPP and RRSP: If you’re trying to build RRSP room or future pension benefits, salary is the main path.

- Mortgage Applications: Banks often prefer T4 income. A stable wage can improve your chances for loans at good rates.

- Regular Budget: If you rely on consistent monthly income to pay living costs, salary is simpler.

Salary suits owners who want straightforward statements, forced savings via CPP, and easy personal budgeting. That said, you might face slightly higher total taxes than if you used a well-structured dividend approach.

10 . The Hybrid Strategy: Mixing Salary and Dividends

Many entrepreneurs do both. For instance, you could pay yourself a modest salary for living costs and to get some CPP coverage, then issue occasional dividends if the corporation has leftover profits. This approach can:

- Offer reliable monthly income

- Maintain RRSP contribution room

- Provide a tax-efficient bonus in the form of dividends

- Allow year-end flexibility—if the company has a good year, declare a higher dividend

“How do i pay myself a dividend” plus a monthly salary is common among owners who want a balanced strategy.

11. How to Move Money Out of Professional Corporations

Doctors, lawyers, accountants, and other professionals often incorporate, then wonder: “How to move money out of professional corporation?” The same “salary vs dividend” logic applies, but check:

- Your profession’s rules: Some colleges or associations have extra guidelines.

- The structure of your professional corp: You might have restrictions on share ownership or dividends to family.

- Minimizing risk: Evaluate insurance, capital reserves, or overhead before draining too much cash.

Declaring dividends in a professional corporation usually follows the same process—board resolution, T5 slips, etc. Salaries likewise require a payroll account. Always ensure your corp remains solvent after paying you.

12. Company Director Pay and Shareholder Distributions

As a director, you might receive a director’s fee or an official salary. But if you’re also a shareholder, you can get dividends. For clarity:

- Directors must act in the corporation’s best interests.

- Paying yourself huge dividends that leave the corporation unable to pay its taxes or debts can lead to personal liability.

- Keep meeting minutes detailing major financial decisions. This ensures you have a paper trail showing your dividend declarations or salary changes.

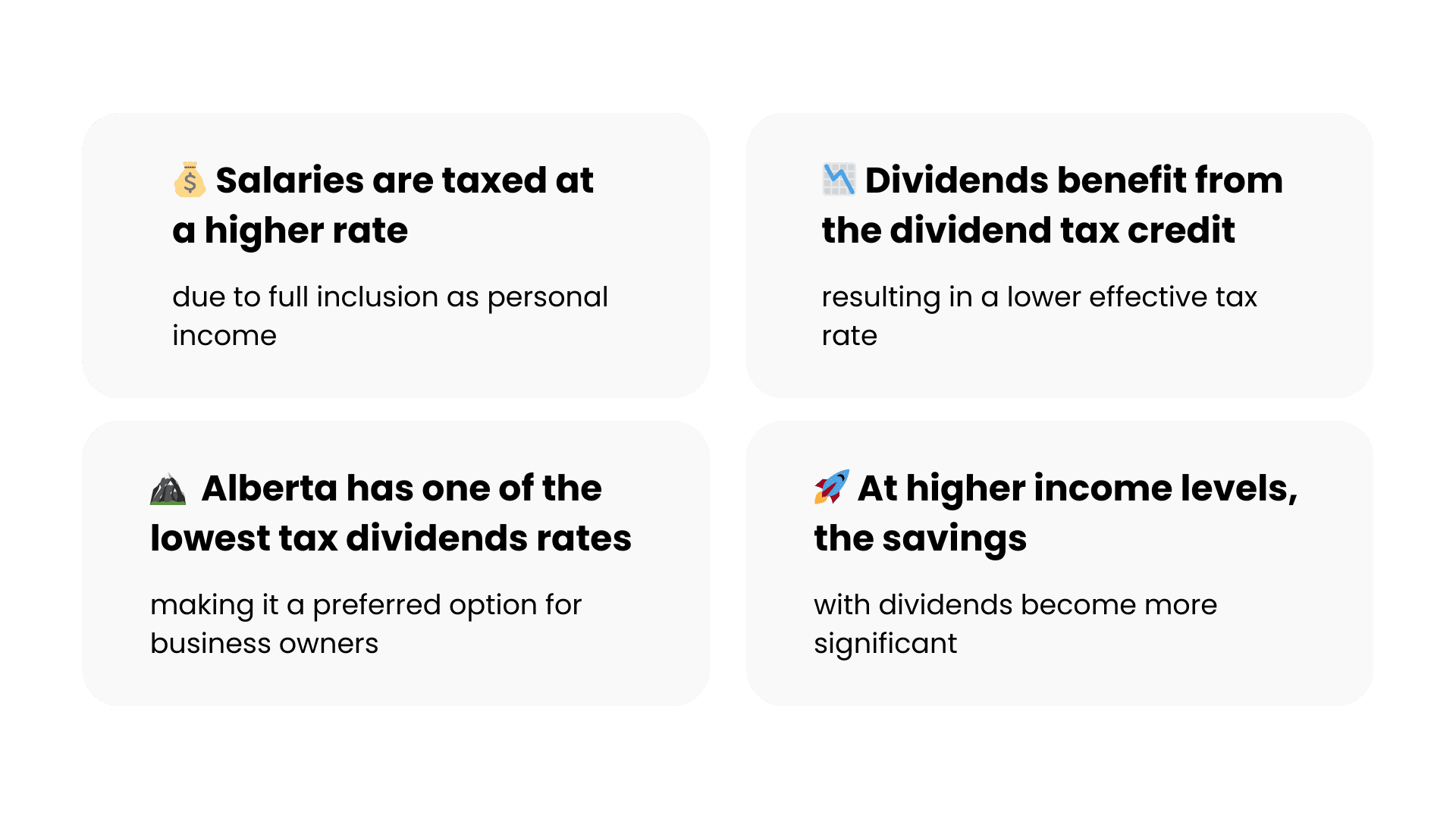

13. Provincial Nuances: Dividend Tax Rate Alberta vs. Others

Your personal location matters. The “dividend tax rate Alberta” differs from Ontario, BC, or Quebec. Why?

- Each province sets its own personal income tax rates and dividend tax credits.

- If you’re in Alberta, your integrated rate on dividends might be slightly higher or lower than in Ontario.

- Keep in mind corporate tax rates also vary by province. Alberta’s general corporate rate is lower than some provinces, which can shift the combined effect.

If you want a precise view, talk with an accountant or use a local “salary vs dividends Canada calculator” that includes your province’s rates.

14. Avoiding Common Mistakes

- Paying Dividends When There Are No Profits: You can’t declare dividends if your company has negative retained earnings.

- Ignoring Share Classes: If you have multiple share classes, ensure you pay the correct dividends to each class.

- Failing to Document: Keep track of all dividends in a corporate minute book. If the CRA audits you, you need proof.

- Not Checking Tax Rates Annually: Federal and provincial rates for dividends vs salary change. Adjust accordingly.

- Late Payment of Corporate Tax: If you neglect corporate tax deadlines to pay yourself first, you risk penalties. The question “what happens if you don’t pay corporation tax on time” is relevant: you face interest, fines, and possible CRA scrutiny.

15. What Happens If You Don’t Pay Corporation Tax on Time?

Paying yourself a salary or dividends is irrelevant if you skip your corporate tax obligations. The CRA imposes:

- Late-Filing Penalties: Usually 5% of the balance, plus 1% per month for up to 12 months or more if repeated.

- Daily Interest: Any outstanding tax accrues interest daily.

- Audits: Chronic delays can trigger a deeper look into your business finances.

- Strained Cash Flow: Penalties add up fast, reducing funds available for salary or dividends later.

Always ensure you set aside enough for corporate taxes before distributing big amounts to yourself.

16. How to Pay Myself Dividends: Step-by-Step Example

Imagine you’re the sole shareholder of ABC Inc.:

- Check Retained Earnings: Suppose ABC Inc. has $50,000 in after-tax profits from last year.

- Decide on Amount: You want $10,000 as a dividend.

- Issue Dividend Resolution: As the director, you sign a corporate resolution stating ABC Inc. will pay a dividend of $10,000 to yourself.

- Record Entry: Debit retained earnings $10,000, credit dividends payable $10,000.

- Transfer Funds: Move $10,000 from the company’s bank to your personal account, or record it to your shareholder loan if you’re not taking it in cash right away.

- End of Year: Prepare T5 slip, listing $10,000 as dividends. You claim it on your personal tax return, applying the appropriate tax credit.

17. How to Pay Myself from My Business with a Salary: Example

Let’s say you own 100% of a corporation called TechCorp:

- Open Payroll Account: TechCorp registers for a CRA payroll number.

- Set Monthly Salary: You pay yourself $4,000 a month.

- Calculate Deductions: Each month, withhold federal/provincial tax, plus your CPP share. Suppose $800 total withheld. TechCorp also pays an employer CPP share.

- Pay Remittance: By the 15th of the next month, TechCorp sends $800 (plus the employer portion) to the CRA.

- Year-End T4: TechCorp issues you a T4 slip for $48,000 annual salary, plus total tax withheld. You report it as personal employment income.

18. Impact on Retirement Savings: CPP, RRSP, TFSA

- CPP: Dividends do not contribute. Salary does. If you rely on CPP for future income, you might prefer some salary to maximize those benefits.

- RRSP Room: Dividends don’t boost RRSP contribution room. Salary does. If you plan to save in an RRSP, consider paying yourself at least enough wage to build space.

- TFSA: Whether you pay yourself salary or dividends, you can always invest in a TFSA. The difference is whether you have enough net income to do so.

19. Special Cases: Paying Myself vs. Minimizing Taxes

You might want to keep personal income low (to minimize your taxes) and let the corporation hold the earnings. This can be wise for expansions or if you want to avoid hitting higher personal tax brackets. However, the personal funds you need monthly matters too. If you starve yourself of personal cash, it’s pointless to have big corporate savings. Balancing the two is crucial. Many owners consider partial dividends, partial salary. A “salary v dividend” approach is never black and white.

20. Conclusion: Decide How to Pay Yourself

If you’re stuck on “dividends vs salary Canada,” or you keep researching “how do i pay myself dividends” and “how do i pay myself from my business,” remember there’s no one-size-fits-all. Each year, re-evaluate these factors:

- Corporate profits vs. your personal cash needs

- RRSP goals, CPP considerations, and personal taxes

- The administrative load you’re willing to handle

- Provincial tax rates if you wonder about “dividend tax rate Alberta” or in other provinces

In a perfect scenario, you might blend salary and dividends for a balanced approach. Or, if you favour a straightforward route, a consistent salary might be best. If you’re comfortable with lumps, you might choose dividends. Regardless, keep excellent records, track your corporation’s finances, and never forget to pay your corporate taxes on time. By doing so, you’ll preserve the health of your corporation while enjoying the personal income you need—without unnecessary tax headaches down the road.