Important Tool for Business Valuation

What Is EBITDA?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. In plain English, it tells you how much profit a company makes from its core operations before the impact of financial and accounting decisions.

It removes variables like:

- Interest (depends on financing)

- Taxes (depend on jurisdiction)

- Depreciation & Amortization (non-cash and vary by asset structure)

So when you ask, “What is an EBITDA?” — you’re really asking: “How much is the business earning before everything else gets taken out?”

Think of EBITDA as a clear picture of a company’s operating performance.

Are you confident your business tax filings are fully optimized and compliant?

The EBITDA Formula

Understanding how to calculate EBITDA starts with knowing what is EBITDA and what is an EBITDA used for in business analysis.

By definition, EBITDA—which stands for Earnings Before Interest, Taxes, Depreciation, and Amortization—removes the noise from net income and helps isolate the gross profit derived from core operations.

Put simply, the EBITDA definition helps you understand profitability before accounting choices or financing decisions affect the numbers. It’s a financial tool used by operators and investors to assess efficiency without the distortion of interest costs or depreciation methods.

There are two standard ways to approach the formula:

Net Income Approach

This method starts from the bottom line—your net income—and adds back costs that don’t reflect day-to-day operations.

EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

This approach is widely used because:

- Net income is readily available from financial statements.

- Interest and taxes reflect financing and location, not operations.

- Depreciation and amortization are non-cash and accounting-based.

📌 Example:

Let’s say your business posts:

- Net Income: $150,000

- Interest Expense: $25,000

- Taxes: $35,000

- Depreciation: $20,000

- Amortization: $10,000

You calculate EBITDA like this:

EBITDA = 150,000 + 25,000 + 35,000 + 20,000 + 10,000 = $240,000

So even if net income is only $150,000, your EBITDA (which excludes financing and accounting adjustments) shows a healthier $240,000.

Operating Profit Approach

If your income statement shows Operating Profit (also called EBIT, or Earnings Before Interest and Taxes), this formula is even easier:

EBITDA = Operating Profit + Depreciation + Amortization

This method skips net income entirely, making it great for:

- Internal reporting

- Multi-year comparisons

- Assessing divisions or subsidiaries

Why Two Methods?

Because different businesses report differently. Some small firms may not break out EBIT, while larger companies do. Either method works—the key is consistency in what you include.

✅ Pro Tip: When comparing EBITDA across businesses, always check whether it’s calculated from net income or EBIT. Inconsistent inputs = misleading conclusions.

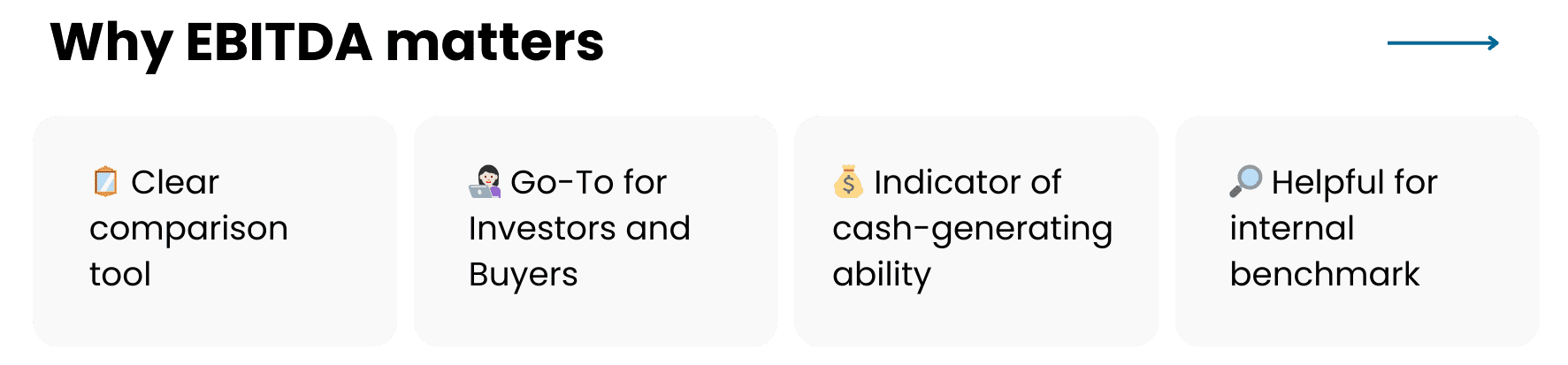

Why EBITDA Matters in Business Valuation

Let’s break it down: what does EBITDA really do for business owners, buyers, and investors?

It isolates the profitability of core operations—stripping away the financial engineering, local tax rules, and accounting quirks. That’s why it’s a favorite in business valuation and M&A.

Cleaner Comparison Tool

Two companies could have:

- Different capital structures (debt vs equity)

- Different asset ages (new vs depreciated equipment)

- Different tax setups (Delaware vs international)

But when you strip all that away with EBITDA, you’re left with what really matters:

How well does this business operate day-to-day?

It creates an apples-to-apples view of financial performance. Whether you’re comparing two coffee chains or two manufacturing firms, EBITDA tells you who runs the tighter ship.

The Go-To for Investors and Buyers

When someone wants to buy your business, they’re often thinking in multiples of EBITDA.

“We’ll pay 6x EBITDA” means if your EBITDA is $500K, they’re offering $3M.

It’s direct, simple, and allows for industry benchmarking.

🔍 Valuation Insight:

- High EBITDA → Higher sale price

- Consistent EBITDA → Lower perceived risk

- Growing EBITDA → Premium multiples

Easy Indicator of Cash-Generating Ability

While EBITDA isn’t the same as cash flow, it points to the potential for cash flow—especially before capital expenditures or interest payments.

Think of it as the raw engine before fuel and wear-and-tear kick in.

If net income is noisy, EBITDA is cleaner. If sales are seasonal, EBITDA shows the underlying strength. That’s why it’s a key metric on pitch decks, term sheets, and due diligence reports.

Helpful for Internal Benchmarking

Even if you’re not planning to sell, EBITDA can help:

- Benchmark year-over-year performance

- Track operational efficiency

- Spot cost inflation in core operations

By removing non-operational expenses, you see what your business is really doing under the hood.

EBITDA vs Net Income: What’s the Difference?

Here’s how they stack up:

| Metric | Includes | Use Case |

|---|---|---|

| EBITDA | Core profits before non-cash and financing expenses | Operational benchmarking |

| Net Income | All revenues minus all expenses | Bottom line profit |

While EBITDA focuses on the engine of the business, net income tells you what’s left over for shareholders. Both are useful — but for different things.

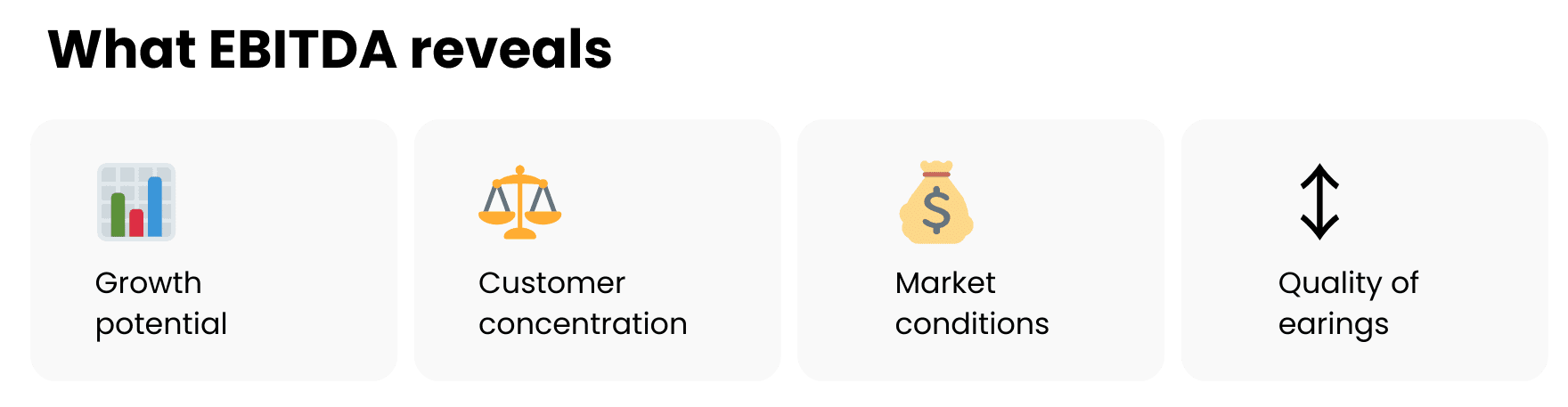

EBITDA Multiples: What They Reveal

EBITDA multiples are used to estimate how much a business is worth.

Formula:

Enterprise Value / EBITDA = EBITDA Multiple

Let’s say your company has an EBITDA of $500,000 and it sells for $2.5 million. That’s an EBITDA multiple of 5x.

Multiples vary by industry:

- SaaS: 6x–12x

- Manufacturing: 4x–6x

- Retail: 3x–5x

These valuation multiples are influenced by:

- Growth potential

- Customer concentration

- Market conditions

- Quality of earnings (i.e., recurring vs one-time)

Limitations of EBITDA

Despite its popularity, EBITDA has blind spots:

- Ignores capital expenditures — a company might need to spend heavily on equipment to sustain EBITDA.

- Excludes debt costs — which can be massive for leveraged firms.

- Doesn’t capture working capital changes, which affect cash flow.

So while EBITDA can show financial performance, it’s not a substitute for analyzing the cash flow statement or overall capital structure.

How to Adjust EBITDA

Sometimes raw EBITDA doesn’t tell the whole story. That’s where Adjusted EBITDA comes in.

You tweak it to remove unusual or one-off items:

- Lawsuit settlement

- Restructuring costs

- Owner’s salary adjustments in private companies

This gives buyers a better sense of normalized earnings.

Table Suggestion:

| Adjustment Item | Impact on EBITDA |

|---|---|

| One-time legal cost | Add back |

| COVID relief grant | Subtract (if non-recurring) |

| Non-operating rental income | Subtract |

Use adjusted EBITDA to show what your business would earn under normal circumstances.

Conclusion: Why You Should Care

If you’re a business owner, investor, or advisor — knowing what EBITDA means gives you an edge. It helps you:

- Compare companies more fairly

- Understand operating health

- Negotiate better deals

It’s not perfect, but it’s powerful.

EBITDA is not the end-all metric — but when used smartly and with context, it can provide a valuable snapshot of financial health.

Frequently Asked Questions

What does EBITDA stand for?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It’s a measure of a company’s operating performance.

How do you calculate EBITDA?

Add back interest, taxes, depreciation, and amortization to net income. You can also start with operating profit and add depreciation and amortization.

Why do investors care about EBITDA?

Because it reflects earnings from core operations, making it easier to compare businesses across different industries or financial setups.

Is a higher EBITDA always better?

Generally yes, but context matters. You must also look at margins, growth, and capital expenditures.

What’s the difference between EBITDA and adjusted EBITDA?

Adjusted EBITDA removes unusual or non-recurring items, offering a clearer view of ongoing profitability.