How Your Various Sources of Income May Be Increasing Your Taxes (And How to Fix It)

When you work hard to earn money, the last thing you want is to pay more taxes than necessary. However, depending on how you make your income, your taxes might be higher than you expect. Understanding how your different sources of income affect your taxes can help you make smarter decisions to reduce the amount you owe.

In this blog, we will explore how various income sources can increase your taxes, and more importantly, how to fix it. We’ll also provide you with some practical tax planning strategies, and ways to reduce taxable income to help you save on taxes. By the end, you’ll have a better understanding of how to keep more of your hard-earned money.

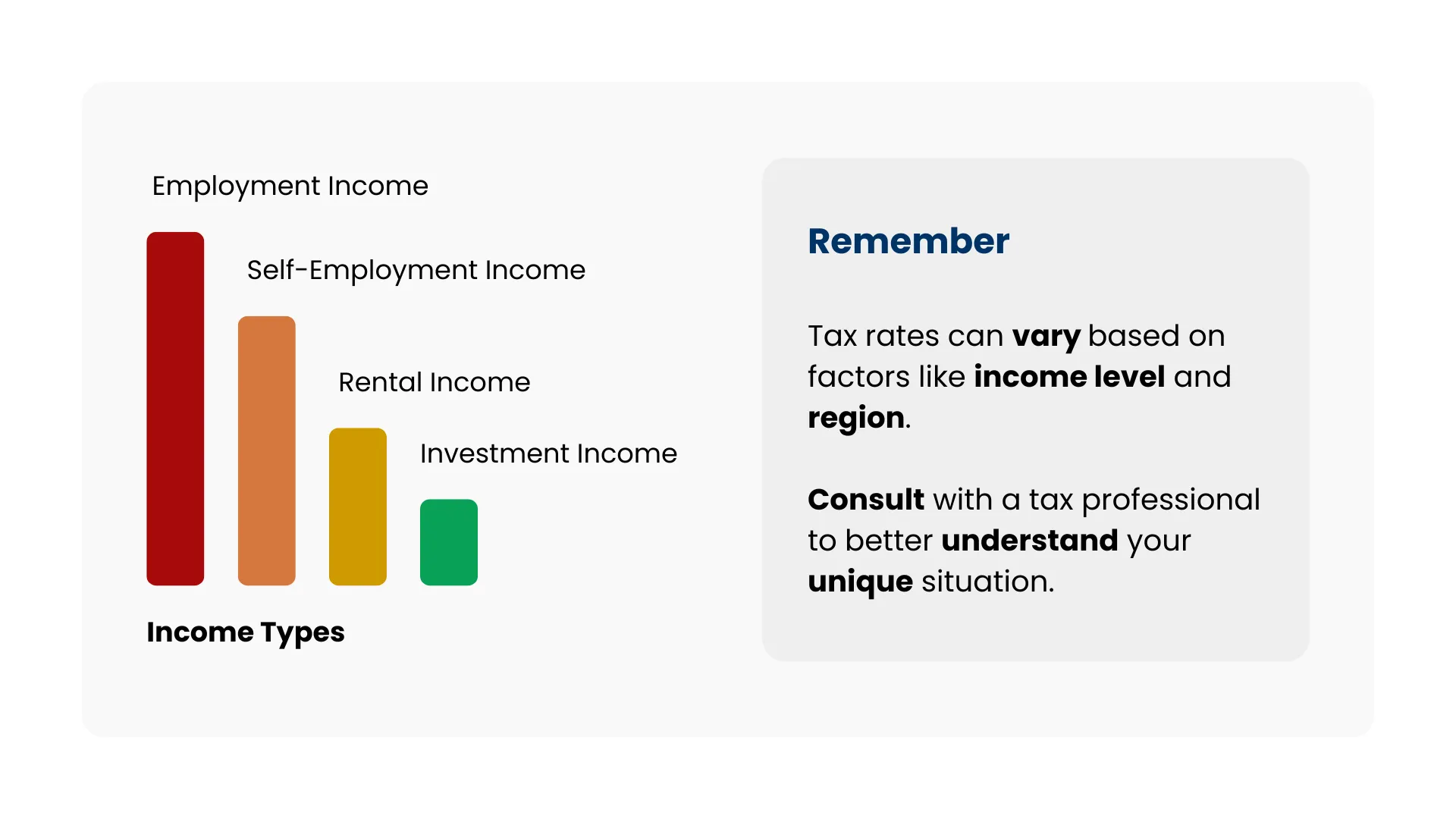

How Different Sources of Income Affect Your Taxes

You might have one or more types of income, and each one is taxed in a different way. Let’s explore how each of these sources can increase your tax liability.

1. Employment Income

When you work for an employer, you receive a paycheck, and a portion of that money is automatically deducted for taxes. The more you earn, the higher the tax rate, which can quickly add up. If you only rely on employment income, you may not have many ways to reduce your taxable income.

2. Self-Employment Income

Being self-employed offers more flexibility and freedom, but it also comes with more responsibilities. How to pay self-employment tax can be tricky because, unlike regular employees, you have to pay both the employer and employee portions of Social Security and Medicare taxes. This means a higher overall tax bill.

For example, if you earn $20,000 as a freelancer, you’ll need to pay self-employment taxes on top of regular income taxes. This can significantly increase your tax liability. Fortunately, there are ways to reduce taxable income when you are self-employed, such as deducting business expenses like office supplies, travel, and even part of your home expenses if you work from home.

3. Investment Income

If you invest in stocks, bonds, or mutual funds, any income earned from these investments will be taxed. This could include dividends, interest, and capital gains. For example, if you sell an asset for more than you paid for it, you’ll owe capital gains tax on the profit.

One common concern for investors is how to avoid capital gains tax. You can minimize this tax by holding investments for longer than a year. Long-term capital gains are typically taxed at a lower rate than short-term gains. By planning ahead, you can make your investment strategy work for you in a tax-efficient way.

4. Rental Income

If you rent out property, whether it’s an apartment or a house, that rental income will be taxed. However, you can also deduct certain expenses related to your property, such as maintenance costs, property management fees, and mortgage interest. This is why tax planning is especially important for landlords – it helps you maximize your deductions and how to reduce taxable income.

5. Business Income

If you own a business, any income you make through it is also subject to taxes. Whether it’s a small side hustle or a large business, you need to pay taxes on your profits. How to do self-employed taxes can be tricky for business owners, but it’s essential to keep accurate records of all income and expenses. By doing so, you can ensure you pay only the taxes you owe and reduce your taxable income through allowable deductions.

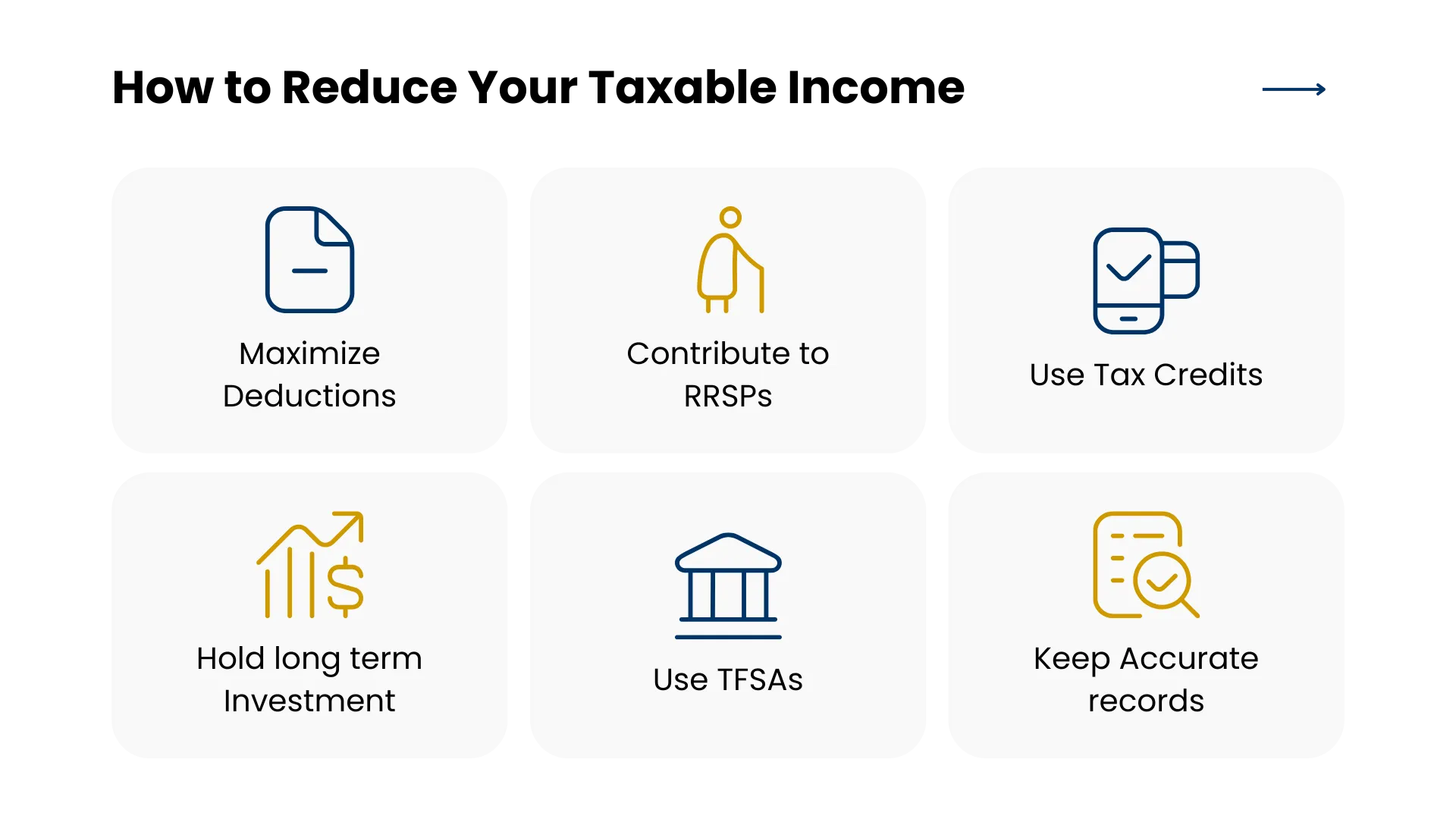

How to Reduce Your Taxable Income

The good news is that there are several strategies you can use to lower your taxable income. Let’s take a closer look at how to reduce taxable income and save money on taxes.

1. Maximize Your Deductions

Deductions are expenses that the government allows you to subtract from your total income, reducing the amount that is subject to taxation. For example, if you’re self-employed, you can deduct business expenses like supplies, equipment, and even the cost of working from home. Keeping track of all your business-related expenses is crucial for how to reduce your taxable income.

Even if you’re employed, there are deductions you may be able to claim, such as charitable donations, student loan interest, or medical expenses. The more deductions you can claim, the lower your taxable income will be.

2. Contribute to Retirement Accounts

Contributing to a retirement account, like a Registered Retirement Savings Plan (RRSP), is a great way to reduce taxable income. When you contribute to these accounts, the amount you contribute is deducted from your income, lowering your tax bill. This means you’ll pay less in taxes in the short term while saving for your future.

Retirement accounts like RRSPs also grow tax-free, meaning you won’t pay taxes on any earnings within the account until you withdraw them. This is an effective tax saving strategy for people who want to plan for the future while lowering their tax liability today.

3. Take Advantage of Tax Credits

Tax credits directly reduce the amount of tax you owe. Unlike deductions, which lower your taxable income, tax credits lower the amount of tax you need to pay. There are various tax credits available, depending on your situation. For example, there are credits for education, medical expenses, and childcare costs.

Using all available tax credits is one of the easiest ways to reduce taxable income and save on taxes.

4. Hold Investments for the Long Term

If you invest in stocks or other assets, holding them for more than a year may help you avoid higher taxes. This is because long-term capital gains are taxed at a lower rate than short-term gains. If you’re wondering how to avoid capital gains tax, the answer is simple: hold onto your investments for the long term.

5. Use Tax-Free Savings Accounts (TFSAs)

In addition to RRSPs, TFSAs allow you to grow your savings without paying taxes on the earnings. This means that any interest, dividends, or capital gains earned in a TFSA are completely tax-free. Contributing to a TFSA is another great tax saving strategy for anyone looking to reduce taxes while growing their wealth.

6. Keep Accurate Records

Whether you’re self-employed or have rental income, keeping accurate records is essential for reducing taxable income. If you have receipts, invoices, or records of business expenses, make sure to keep them organized. This will make it easier for you to file your taxes and take advantage of deductions that can lower your tax bill.

Did you Know? If you invest in your Tax-Free Savings Account (TFSA) in Canada, any income earned, such as interest, dividends, or capital gains, is tax-free! This can be a powerful tool for tax planning and saving. Learn more here. |

Tax Planning Strategies to Help You Save on Taxes

Effective tax planning can make a huge difference in the amount of tax you pay. By planning ahead and understanding your income sources, you can minimize your tax liability and how to save money on taxes.

Here are some useful tax planning strategies to consider:

Strategy | Description |

| Contribute to RRSPs | Reduce taxable income and save for retirement. |

Track business expenses | Deduct legitimate business expenses to lower taxes. |

Hold investments long-term | Take advantage of lower long-term capital gains tax rates. |

Maximize tax credits | Use all available tax credits to lower your tax bill. |

Contribute to TFSAs | Save money without paying taxes on your earnings. |

Conclusion

Taxes can be a burden, especially if you have multiple sources of income. However, with the right tax planning and a good understanding of how to reduce taxable income, you can significantly lower your tax bill. Whether you’re self-employed, have rental income, or earn from investments, there are several ways to save on taxes and keep more of your hard-earned money.

By implementing tax planning strategies, using tax-advantaged accounts, and taking advantage of deductions and credits, you can make sure that you’re paying only the necessary taxes and not a penny more.

If you’re feeling unsure about how to file taxes as a sole proprietor, or if you need help with how to do self-employed taxes, contact us today. Book a consultation, and we’ll help you create a tax plan that works for you.

FAQs

1. What tax planning strategies can help reduce the impact of multiple income sources?

Use strategies like income splitting, contributing to RRSPs, and maximizing tax credits. These approaches help spread income across tax brackets and reduce your overall taxable income.

2. What should I know about how my investments and side businesses affect my taxes?

Income from investments and side businesses may push you into a higher tax bracket. Keep detailed records, claim eligible deductions, and consider professional advice for accurate tax filing.

3. How can I minimize the tax burden from freelance or self-employed income?

Track all business expenses and claim deductions like home office and vehicle costs. Filing taxes as a sole proprietor and using tax software can help manage self-employment taxes efficiently.

4. How can I use tax deductions to lower taxes on different types of income?

Claim deductions like childcare costs, education expenses, or charitable donations. For business income, write off expenses like supplies and advertising. Proper documentation ensures you maximize tax savings legally.

5. How does splitting income between family members help reduce taxes?

Income splitting allows you to transfer income to lower-earning family members, reducing the overall tax burden. Methods include spousal RRSP contributions or hiring family members for business work.

picture, offering expert advice on taxes, financial health, and ensuring everything is compliant with regulations.