How to Calculate the Cost of Goods Manufactured (COGM)

What Is Cost of Goods Manufactured (COGM)?

COGM refers to the total costs incurred in converting raw materials into finished goods during a specific period, typically tied to your monthly or quarterly accounting period. It captures everything that happens inside your facility—from labor and materials to indirect costs—until goods are fully completed.

You also factor in your beginning and ending work-in-progress (WIP) inventory to ensure the figure reflects only the cost of items completed during that time.

Basically, if your factory produces 1,000 chairs in April, the COGM tells you exactly how much it cost to finish those 1,000 chairs—not the ones still in process, and not the ones already sitting in your finished goods warehouse.

Are you confident your business tax filings are fully optimized and compliant?

Why COGM Matters in Manufacturing

COGM isn’t just an internal accounting metric. It’s a strategic lens for operations, finance, pricing, and growth.

Here’s why it matters:

- Sets the foundation for cost of goods sold (COGS): You need COGM to calculate COGS, which feeds into your income statement.

- Improves pricing strategy: Know how much it costs to produce before setting your prices.

- Helps manage efficiency: Rising COGM could flag waste, equipment issues, or labor inefficiency.

- Assists with budgeting and planning: Accurate forecasting needs a clear view of current production costs.

- Supports gross margin tracking: Gross margin = Revenue – COGS. So if COGS is off, your margins are too.

The Cost of Goods Manufactured Formula

Here’s the classic COGM formula:

| COGM = Direct Materials Used + Direct Labor + Manufacturing Overhead + Beginning WIP – Ending WIP |

Let’s break each element down:

| COGM Component | Description |

|---|---|

| Direct Materials Used | Raw materials consumed during production |

| Direct Labor | Wages and benefits for workers directly assembling products |

| Manufacturing Overhead | Factory rent, depreciation, maintenance, utilities |

| Beginning WIP Inventory | Value of incomplete goods at the beginning of the period |

| Ending WIP Inventory | Value of incomplete goods at the end of the period |

The COGM formula is designed to track the total expense across your manufacturing processes. It provides a reliable snapshot of what your production processes cost during a defined accounting period, ensuring that every inventory accounted reflects true, up-to-date costs.

Step-by-Step: How to Calculate COGM

Let’s walk through an example.

Your factory makes leather wallets.

Step 1: Calculate Direct Materials Used

Formula:

| Direct Materials Used = Beginning Raw Material Inventory + Purchases – Ending Raw Material Inventory |

Say:

- Beginning Inventory = $5,000

- Purchases = $25,000

- Ending Inventory = $4,000

→ Direct Materials Used = $26,000

Step 2: Add Direct Labor

Include:

- Hourly wages for production workers

- Overtime

- Benefits, if production-linked

Let’s say: → Direct Labor = $18,000

Step 3: Add Manufacturing Overhead

This includes:

- Factory utilities

- Maintenance costs

- Equipment depreciation

- Factory manager’s salary (indirect labor)

Total overhead = $12,000

Step 4: Adjust for WIP Inventory

- Beginning WIP = $3,000

- Ending WIP = $4,000

Final COGM Formula:

| COGM = 26,000 + 18,000 + 12,000 + 3,000 – 4,000 = **$55,000** |

You spent $55,000 to produce your completed wallets this month.

Real-World Applications: How COGM Drives Smarter Business

Understanding the cost of goods manufactured helps you make more informed, profitable decisions across various areas of your business. Here are five specific ways:

Pricing & Profitability Analysis

COGM directly impacts your gross margin—the more accurately you know what it costs to produce a product, the more precisely you can price it. Let’s say your COGM per unit is $14, and you’re selling at $15. That’s only a $1 margin, which might not even cover your admin or distribution costs.

Regularly tracking COGM helps you identify when production costs rise and take corrective action, like renegotiating supplier rates or tweaking pricing.

Budgeting and Forecasting

Your production budget relies heavily on COGM. Knowing what it costs to make each unit allows you to project future spending, especially if you’re scaling operations or adding new product lines.

If COGM is rising quarter over quarter, your forecasts need to reflect that shift. Failing to do so can lead to underfunded operations and missed revenue targets.

Product Line Evaluation

Some products are costlier to manufacture than others. With detailed COGM data per product line, you can compare margins and make calls like:

- Which SKUs are underperforming?

- Should we discontinue a product or switch to cheaper materials?

- Are we allocating resources to high-margin lines?

This insight supports more strategic inventory and product decisions.

Manufacturing Efficiency Tracking

If your COGM has been trending up but your production volume hasn’t, something’s wrong. It could be:

- Inefficient labor scheduling

- Machinery downtime

- Material wastage

Tracking these costs over time gives you the ability to investigate spikes and take targeted action, like investing in automation or cross-training workers to improve output.

Capital Investment Justification

Planning to invest in new machinery or upgrade your plant layout? COGM helps you compare your current cost structure to your projected post-investment costs.

For example, if automating a production line reduces your direct labor costs by 20%, your future COGM could justify the capital expenditure through higher margins.

COGM vs. COGS: Why the Distinction Matters

Let’s clear up this common confusion.

| Metric | Covers | Used For |

|---|---|---|

| COGM | Cost to manufacture goods | Internal efficiency & costing |

| COGS | Cost of goods sold | Financial reporting (income stmt) |

COGM is a stepping stone to COGS.

Here’s the COGS formula:

| COGS = Beginning Finished Goods Inventory + COGM – Ending Finished Goods Inventory |

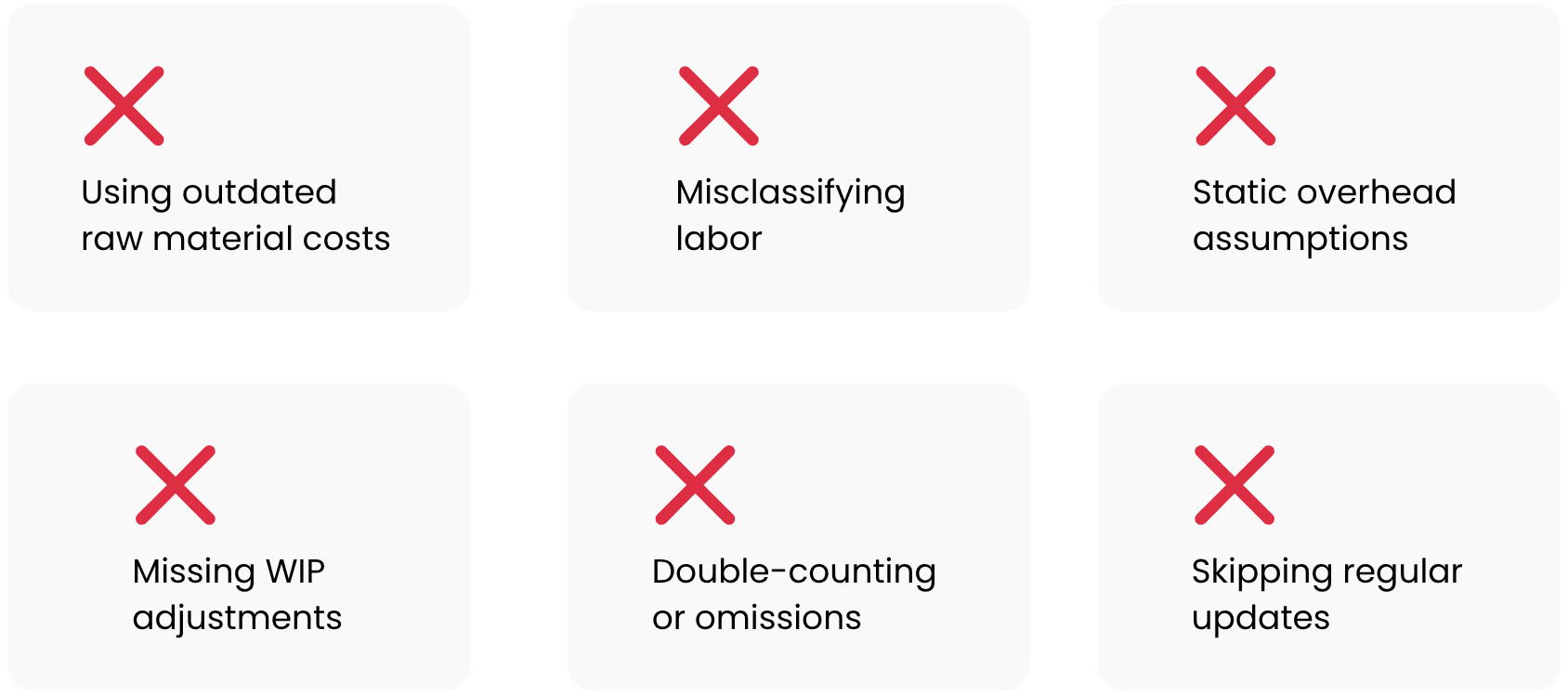

Common Mistakes in COGM Calculations

While the COGM formula looks simple, many businesses fall into traps that lead to inaccurate reporting. Here are the most frequent mistakes to watch for:

Outdated or Incorrect Raw Material Costs

Using last year’s prices or failing to include freight and import fees can distort material valuations. Use real-time inventory valuation systems and apply the correct method—FIFO, LIFO, or weighted average—consistently across all raw material inputs.

Misclassified Labor

Maintain a clear distinction between direct and indirect labor in your payroll system. Cross-check with your production schedules to verify inclusion is appropriate. Including admin staff or R&D teams inflates your COGM.

Flat Manufacturing Overhead

Overhead can vary widely month to month. Using a static figure can make your COGM seem stable—even when it’s not. Regularly update your overhead rate using actual incurred costs, not just budgeted estimates. If you use predetermined overhead rates, adjust periodically to reflect true spending.

WIP Inventory Errors

Missing or misestimating beginning or ending WIP can skew your production cost by thousands. Always tie WIP figures to physical or system-based counts.

Overlooking Waste or Defects

WIP directly affects COGM. Overstating ending WIP understates your COGM—and vice versa. These mistakes can skew both your gross profit and inventory levels. Implement barcode or batch tracking for in-process inventory and align it with your ERP or accounting software. Even in small operations, a manual WIP log updated daily can help.

Infrequent Calculations

Some businesses mistakenly include the same cost in multiple categories (e.g., counting factory rent in both overhead and admin costs), or omit them entirely (like machine depreciation). This distorts your COGM calculation and causes confusion when reconciling financial statements. Maintain a COGM worksheet template that clearly separates cost types and includes a review checklist. Have accounting double-check entries quarterly for duplication or omissions.

Avoiding these common mistakes keeps your COGM clean, timely, and actionable—helping you manage costs with confidence and accuracy.

Conclusion

The cost of goods manufactured is more than just a formula—it’s your gateway to profit clarity.

Understanding how much it truly costs to produce your goods helps you price right, reduce waste, and grow sustainably. Whether you’re scaling up, seeking investors, or just trying to control costs, a well-tracked COGM keeps your business sharp.

So next time you look at your profit margins, remember: it all starts with what happens on the production floor—and how well you measure it.

Frequently Asked Questions

Is COGM the same as COGS?

No. COGM is the cost of making goods. COGS is the cost of selling them.

What’s included in manufacturing overhead?

Things like:

- Factory rent

- Depreciation of machines

- Indirect labor

- Utilities

Can software help calculate COGM?

Yes. Tools like:

- Craftybase (for makers and small batch manufacturers)

- Unleashed Software (for inventory-led businesses)

- ERP systems (for enterprise use)

These tools help automate real-time cost tracking.

How often should COGM be calculated?

Ideally:

- Monthly for high-volume manufacturers

- Quarterly for others

This keeps your financials and forecasts current.

What happens if I miscalculate COGM?

You risk:

- Setting wrong prices

- Misreporting inventory values

- Misleading your income statement

- Making flawed strategic decisions

COGM isn’t just a metric—it’s a business control lever.