Equity vs. Debt Financing: Scale Smartly

What Is Equity vs. Debt Financing?

Running a business comes down to two things: having a good idea and having the money to fuel it. That money typically comes in two flavors — equity financing and debt financing.

Equity financing means selling a piece of your company to investors. Debt financing means borrowing money and paying it back with interest.

Both are powerful. Both come with trade-offs. And choosing between them could shape the future of your business.

Debt Financing: Borrow and Build

With debt financing, you get a lump sum and agree to pay it back over time — plus interest. Think of business loans, lines of credit, or even a company credit card.

You stay in control. You don’t give up ownership. But you do take on a financial obligation.

Good to know:

- Payments are fixed and predictable

- Interest is often tax deductible

- You’ll need strong cash flow to stay on schedule

- Can include both short-term debt (for working capital) and long-term debt (for equipment or expansion)

Common debt financiers include banks, credit unions, and alternative lenders.

Are you confident your business tax filings are fully optimized and compliant?

Equity Financing: Raise and Share

Equity financing is when you trade ownership for capital. Investors — from friends and family to venture capitalists — give you money in exchange for shares.

There’s no repayment pressure. No interest. But your investors now own a slice of the business.

Here’s the upside:

- Ideal for high-growth startups

- No need for existing revenue or assets

- You get more than money (mentorship, network, credibility)

But there are trade-offs:

- You dilute your ownership

- Investors may want decision-making power

- It takes longer to close a round than get a loan

This route is popular for businesses that are early-stage, tech-driven, or aiming big.

Debt vs. Equity: Key Differences

| Feature | Debt Financing | Equity Financing |

| Ownership | You keep it | You share it |

| Repayment | Required | Not required |

| Tax Benefits | Yes (interest is deductible) | No |

| Speed | Fast access | Slower process |

| Risk | Default on payments | Loss of control |

Choose debt if you want to move quickly without giving up control. Choose equity if you need a runway to build and scale without worrying about payments.

Combining Both: A Smarter Way to Fund Growth

You don’t have to choose just one. Many companies blend equity and finance strategies. Start with equity to get off the ground. Then layer in debt when you have reliable revenue.

This equity to debt shift helps balance growth with control. It also helps improve your debt to equity ratio — a financial metric that investors and lenders watch closely.

Example: Raise $300K in equity to launch. Use a $150K line of credit later to expand. That way, you scale without giving away too much.

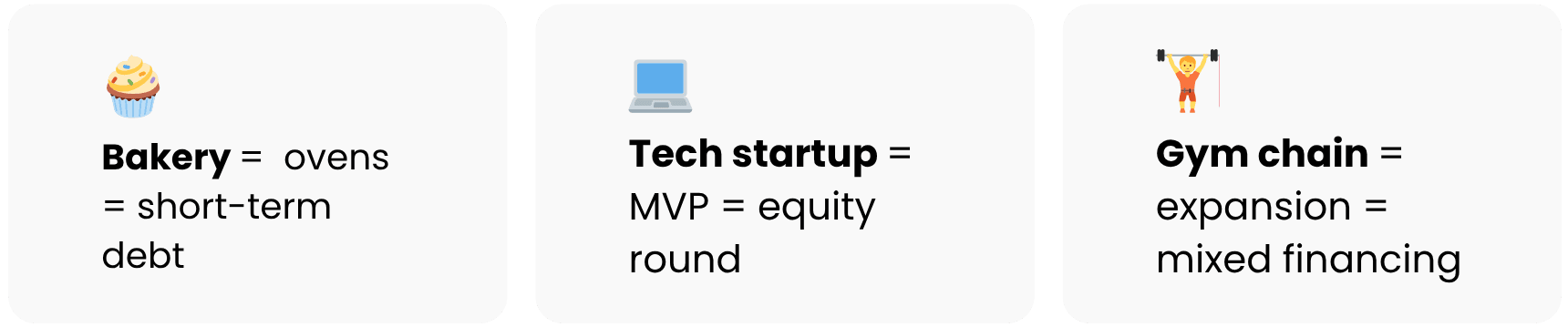

Real-World Scenarios

You run a bakery: Steady income. You use short-term debt to buy new ovens. Your ownership stays intact.

You’re a tech founder: No revenue yet. You raise equity financing from angel investors to build your product.

You own a gym chain: You get a long-term debt loan to open new locations. You also raise a small equity round to hire a head of marketing.

In each case, the mix depends on your goals, timeline, and working capital needs.

How Cash Flow, Interest, and Equity Shape Your Bottom Line

Every funding decision hits your bottom line differently. With debt, you’re making interest payments that reduce net profit but are tax deductible. With equity, you’re sharing profits — forever.

Use these factors to evaluate:

- Will your cash flow support regular loan payments?

- Are you okay giving up shareholder equity to avoid taking on debt obligations?

- Is the interest rate fixed or variable?

- Can you handle the pressure of monthly payments?

These questions help clarify the better fit.

Visual Guide: Debt vs. Equity Snapshot

| Element | Debt | Equity |

| Timeline | Short to medium term | Long-term growth |

| Collateral | Often required | Not needed |

| Flexibility | Less (fixed terms) | More (no repayment) |

| Who Provides It | Banks, online lenders | Angels, VCs, family |

| Risk Type | Financial risk | Ownership dilution |

Mistakes to Avoid When Raising Capital

- Relying too heavily on credit cards

- Over-diluting early with too much equity

- Taking on total debt without a repayment plan

- Ignoring your debt to equity ratio

- Misreading the fine print on terms debt offers

And here’s a big one: not aligning the funding source with your business model. For example, seasonal businesses need flexibility. High-growth startups need patience.

Final Thoughts: What’s Right for Your Business?

There’s no perfect formula. The right funding approach depends on where your business is, where it’s headed, and how much risk you’re willing to carry.

Some founders prefer to raise funds from friends and family. Others go after business loans for predictable growth. Many use a mix. And the savviest understand their debt to equity ratio like the back of their hand.

The takeaway? Don’t just follow the crowd. Choose the route that helps you scale smart.

Frequently Asked Questions

What’s the main difference between equity financing and debt financing?

Equity means giving up part of your business in exchange for capital. Debt means borrowing money and paying it back over time.

Are interest payments tax deductible?

Yes, in most cases, business loan interest can be deducted from your taxable income.

How do I calculate the debt to equity ratio?

Take your total debt and divide it by your shareholder equity. It’s a key number for lenders and investors.

What are the advantages of debt financing?

- Keep full control

- Interest is tax deductible

- Helps build credit

- Clear repayment terms

Can I use both equity and debt financing?

Absolutely. Many businesses use both to balance risk and reward.