How Orbit Accountants Can Help

When managing your business finances, one of the first things that you will be needing to decide is how to track your income and expenses.

This choice can shape how you view your profits, manage cash flow, and file taxes.

The two main methods – cash accounting and accrual accounting each have their own benefits and limitations. While one focuses on real-time cash movement, the other gives a more complete financial picture.

In this blog, we will be breaking down cash accounting vs. accrual accounting in simple terms so you can confidently decide which method suits your business best, no matter your experience level.

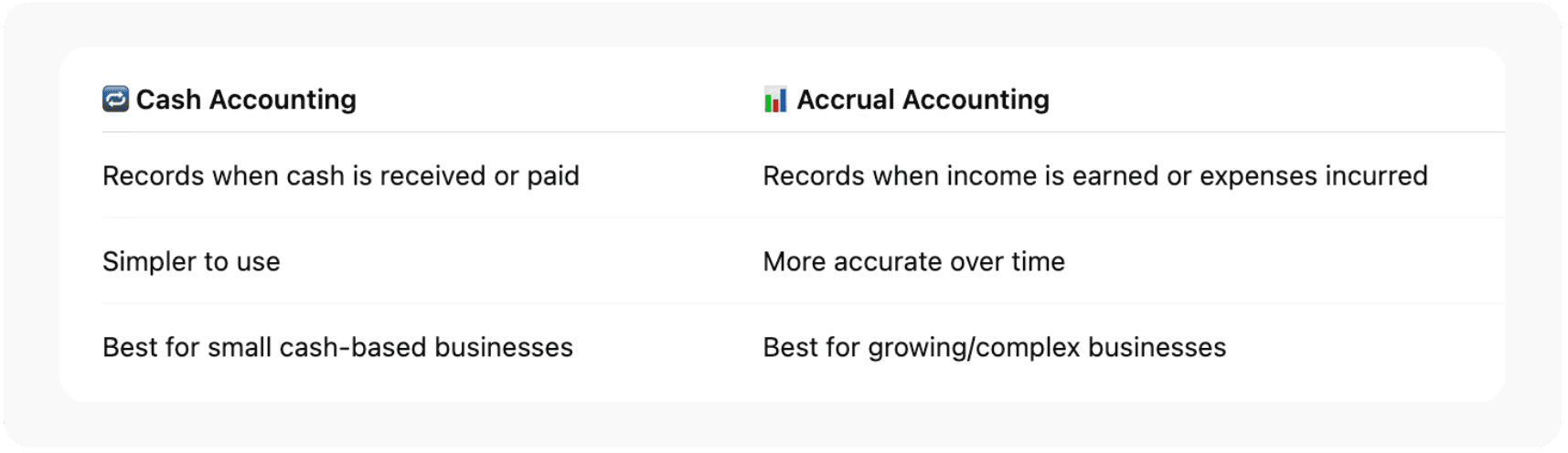

What Is Cash Accounting?

Cash accounting is the easier of the two methods. In this system, you record income only when you actually receive the money, and you record expenses only when you pay them.

For example, if you send an invoice today but the client pays you next month, you won’t record that income until the money lands in your bank account. It works the same for expenses – if you receive a bill but haven’t paid it yet, it won’t show in your books until the money goes out.

This method is very common for small businesses, freelancers, and sole proprietors because it is simple to manage and gives a clear picture of how much cash you actually have on hand.

What Is Accrual Accounting?

Accrual accounting on the other hand is a little more complex. In this method, you record income when it is earned, not when it is received, and you record expenses when they are incurred, not when they are paid.

Let’s say you completed a project today and sent an invoice. Under this system, you will record that income today even if your client pays you a month later. Similarly, if you get a bill today for something you used this month, you record the expense now, even if you pay it later.

Accrual accounting gives a more accurate picture of your business’s financial health, especially over longer periods. That’s why it’s preferred by larger businesses or businesses that need detailed financial reports.

Are you currently managing your bookkeeping in-house?

Key Differences Between the Two Methods

The biggest difference between accrual accounting vs cash basis accounting is timing. It’s all about when the money is recorded.

Here’s a simple comparison to give you a brief understanding:

| Feature | Cash Accounting | Accrual Accounting |

| Income Recorded | When received | When earned |

| Expenses Recorded | When paid | When incurred |

| Matches Invoices/Receipts? | No | Yes |

| More Accurate Long-Term? | No | Yes |

Understanding this table can help you see why the choice between cash accounting vs accrual accounting depends on your business needs.

Which Is Better for Small Businesses?

If you run a small business and mostly deal in cash transactions, the cash method might suit you well. It is easier to understand, and you always know how much money you have available.

However, if your business is growing, and you’re dealing with larger projects, delayed payments, or expenses that need to be tracked over time, accrual accounting may be a better fit. It provides a more realistic picture of your business performance.

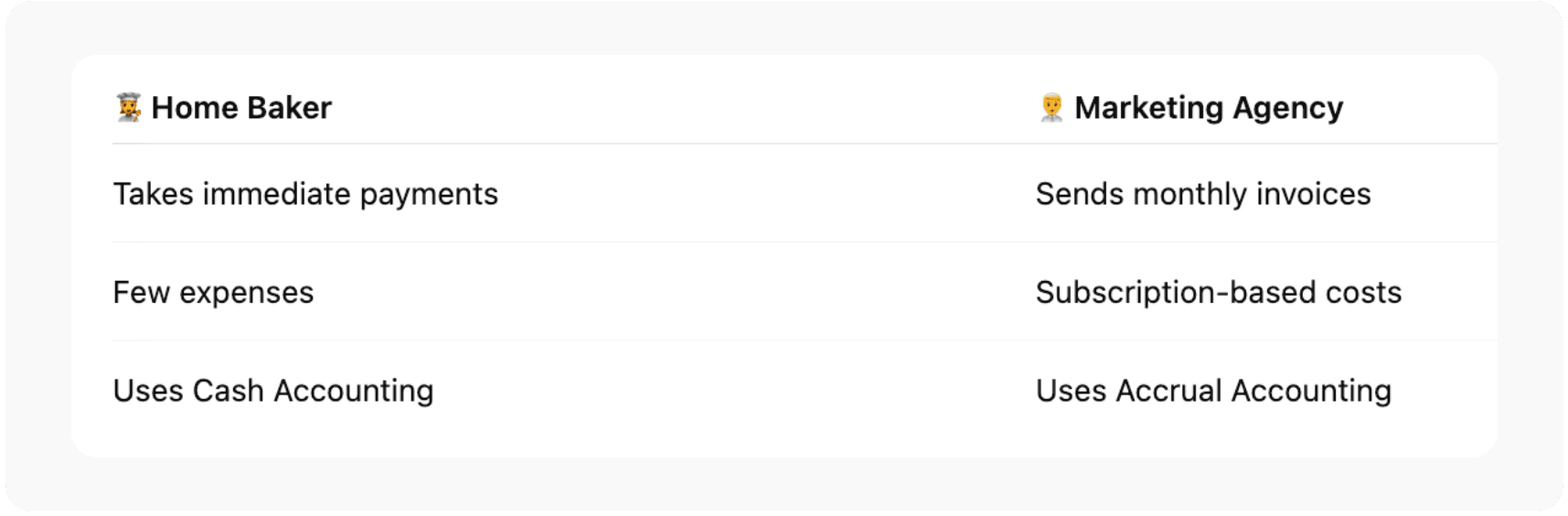

Let’s imagine two businesses: a small home baker and a mid-size digital marketing agency.

The baker mostly takes payments immediately from customers either in cash or through a payment app. Cash accounting works well here because the business only records money that’s been received or paid.

Now, the marketing agency often sends invoices to clients and pays for services like software and advertising that are billed monthly. Even if the client pays late, the agency still needs to show the income in the month the work was done. In this case, accrual accounting helps provide an accurate view of profits and losses.

This example shows how the accounting method accrual vs cash works in real-life business situations.

What About Taxes?

Your choice of accounting method also affects your taxes. In cash accounting, you only pay tax on money you have received. So if you invoice a client in December but they pay in January, you’ll include that income in next year’s taxes.

In accrual accounting, that income is counted when invoiced, so it will be taxed in the current year even if the money hasn’t been paid yet.

This is an important point to consider when choosing between accrual basis vs cash basis, especially if you’re planning your year-end finances.

|

How Orbit Accountants Can Help

Here, at Orbit Accountants, we have been providing expert bookkeeping services in Canada. We understand that every business is different and has unique needs when it comes to accounting, taxes, and financial planning. That is why we offer personalized services that are designed to match your business goals.

From managing daily transactions to preparing accurate financial statements, our experienced team uses the latest tools and follows the best practices to make sure your records are up-to-date and compliant.

Book a free consultation, and we’ll guide you through the entire process!.

In Essence

Choosing between accrual accounting vs cash basis accounting may seem overwhelming at first, but with the right information and guidance, you can make the best decision for your business. Cash accounting is simpler and easier to manage for new and small businesses. On the other hand, accrual accounting gives a clearer and more accurate financial picture, especially for growing companies.

Whichever method you choose, the important thing is to be consistent, stay organized, and seek professional help when needed. Understanding the difference between accounting method accrual vs cash will help you track your money better, make smarter decisions, and grow your business with confidence!

Frequently Asked Questions

What is the difference between cash and accrual accounting?

Cash accounting records income and expenses when money is received or paid. Accrual accounting records them when they happen, even if the money isn’t received. However, accrual gives a more accurate picture of a business’s finances, while cash accounting is easier and shows real-time cash flow.

What are the advantages and disadvantages of accrual accounting?

Accrual accounting gives a clearer view of income and expenses, helping with better planning and decision-making. But it’s more complex and needs careful tracking. Unlike cash accounting, it doesn’t show actual cash available, which might confuse business owners who want to know their current cash status.

How does accrual accounting affect financial statements?

Accrual accounting matches income and expenses to the time they occur, not when money is received or paid. This makes financial statements more accurate and useful for understanding real profits. It helps businesses see what they truly earned or owe in a given period, even without cash movement.

Is cash or accrual accounting better for tax purposes?

It depends on your business size and needs. Cash accounting can delay taxes by recognizing income only when received. Accrual accounting shows income when earned, which might lead to earlier taxes but gives a more accurate financial understanding.

Can a business switch from cash accounting to accrual accounting?

Yes, a business can switch from cash to accrual accounting. It usually requires approval from tax authorities and adjusting previous records to match the new method.