Incorporating a Business in Canada: Guide for Small Business Owners

For many owners, incorporating a business in Canada feels like a natural next step. Revenue is growing, the business is becoming more real, and the old structure no longer feels like the right fit. What started as a side hustle or a simple partnership now has staff, recurring clients, equipment, and actual risk.

That is usually the point where the conversation shifts from “Should we incorporate?” to “What exactly changes once we do?”

A lot, actually.

Yes, incorporation can offer limited liability, a separate legal entity, stronger credibility, and potential tax planning advantages. But it also creates a new compliance world: a corporation has its own filings, its own bookkeeping, and its own deadlines. If you are moving from partnership to corporation, the transition also raises a tax question many owners do not see coming: how do you transfer assets or business activity into the new company properly?

Why Small Businesses Incorporate

There is no single reason owners incorporate. Usually, it is a mix of legal, commercial, and tax reasons.

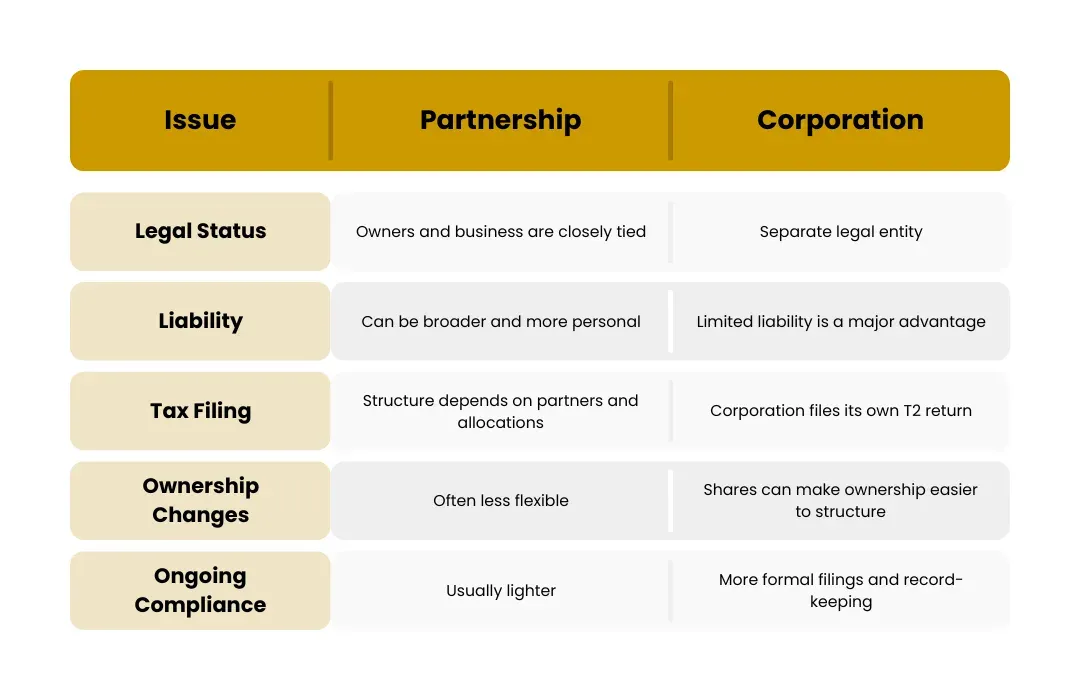

The first is limited liability. A corporation is a separate legal entity, which means the business is legally distinct from its shareholders. The second is tax structure. Corporations are taxed separately from their owners, and government guidance notes that corporate tax rates are generally lower than personal income tax rates. The third is credibility and flexibility. A corporation can often make it easier to add shareholders, raise capital, formalize ownership, and present a more established business profile.

There is also a practical branding angle. Clients, lenders, and partners often view an incorporated business as more permanent and more organized. That does not mean every business should incorporate immediately. But once profits are stable, ownership is becoming more complex, or liability exposure is rising, the conversation becomes serious.

Another decision is whether to incorporate federally or provincially. Federal incorporation generally gives the corporation the right to carry on business anywhere in Canada and is often seen as having broader recognition, while provincial incorporation follows the rules of the province or territory where you incorporate. Either way, there may still be extra-provincial registration requirements depending on where you operate.

Partnership vs. Corporation at a Glance

The Incorporation Process: Timeline and Steps

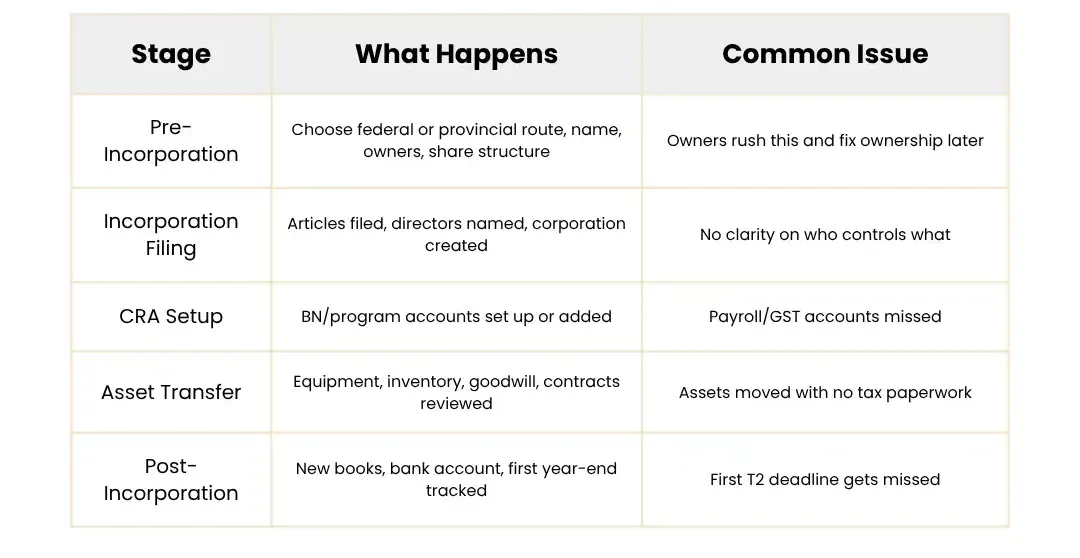

From a high level, incorporating a business in Canada is not just “filling out one form.” It is a sequence of legal and tax setup steps.

For a federal incorporation, the government describes a five-step process: choose a name, prepare the articles of incorporation, set the registered office and first directors, file information on individuals with significant control, and submit the application and fee. As part of federal incorporation, you can also obtain a business number and a corporation income tax account, with options to register for other CRA program accounts such as GST/HST and payroll.

In practice, most small business owners should think about the transition in three layers:

1. Legal setup

You choose the jurisdiction, corporate name, directors, share structure, and articles. If there are multiple owners, this is also the stage to think carefully about who owns what and whether a shareholders’ agreement is needed.

2. Tax and account setup

You obtain or update your CRA registrations. Depending on the situation, that may include a corporation income tax account, GST/HST account, payroll account, and possibly import/export accounts.

3. Operational cleanup

You open a corporate bank account, move your bookkeeping into the new entity, stop mixing personal and business expenses, and document any assets or contracts being transferred into the corporation.

Simple Transition Timeline

How to Calculate Employment Health Tax BC

Tax can be calculated very easily with an understanding of how payroll and rates work together. There are also online tools provided by the province to assist all employers in estimating their liabilities accurately so they don’t make mistakes.

Using the BC Employer Health Tax Calculator

The use of the BC employer health tax calculator allows employers to estimate tax liability by inputting their total BC remuneration to the calculator. This determines any exemptions and / or rates that apply.

Taxable remuneration explained

Taxable remuneration includes pay, salary, bonus, commission, tax-benefit, etc. for employees working in British Columbia during the calendar year.

Example calculation scenarios

A payroll of $2 million incurs a tax of 1.95% which is $39,000; or, a payroll of $1 million only calculates tax on what is above $500,000 (use partial relief formula).

Tax Implications: Section 85 Rollovers and the First Corporate Return

This is where many transitions go sideways.

When you move an existing business into a corporation, you are not just changing the name on the invoice. You may be transferring property into a new taxpayer. That can include equipment, inventory, receivables, goodwill, or other business assets. If that transfer is handled badly, it can create unintended tax consequences.

One of the key tools here is the Section 85 rollover. Under section 85 of the Income Tax Act, a taxpayer and a taxable Canadian corporation can jointly elect on eligible property transferred to the corporation when the consideration includes shares. In plain English, this may allow certain assets to move into the corporation on a tax-deferred basis rather than triggering immediate gains at fair market value. The election is generally made using CRA Form T2057.

This is exactly why a mid-year move from partnership to corporation deserves more than a template checklist. The details matter:

- what property is being transferred

- what values are assigned

- whether liabilities are also being assumed

- what consideration the owners receive

- whether the election is filed properly and on time

A second issue is the first T2 return.

Once the corporation exists, it generally has to file a T2 corporate income tax return for every tax year, even if there is no tax payable. CRA guidance is clear that this includes inactive corporations, with only limited exceptions. The filing deadline is generally within six months of the corporation’s year-end. The tax balance is generally due two months after year-end, although some Canadian-controlled private corporations may have a three-month balance-due day if they meet the required conditions. For tax years starting after 2023, corporations generally have to file the T2 electronically.

That means a brand-new corporation can fall behind surprisingly fast. Owners often assume, “We just incorporated, so filings are a next-year problem.” They are not.

What Changes After Incorporating: Bookkeeping, Payroll, and CRA Obligations

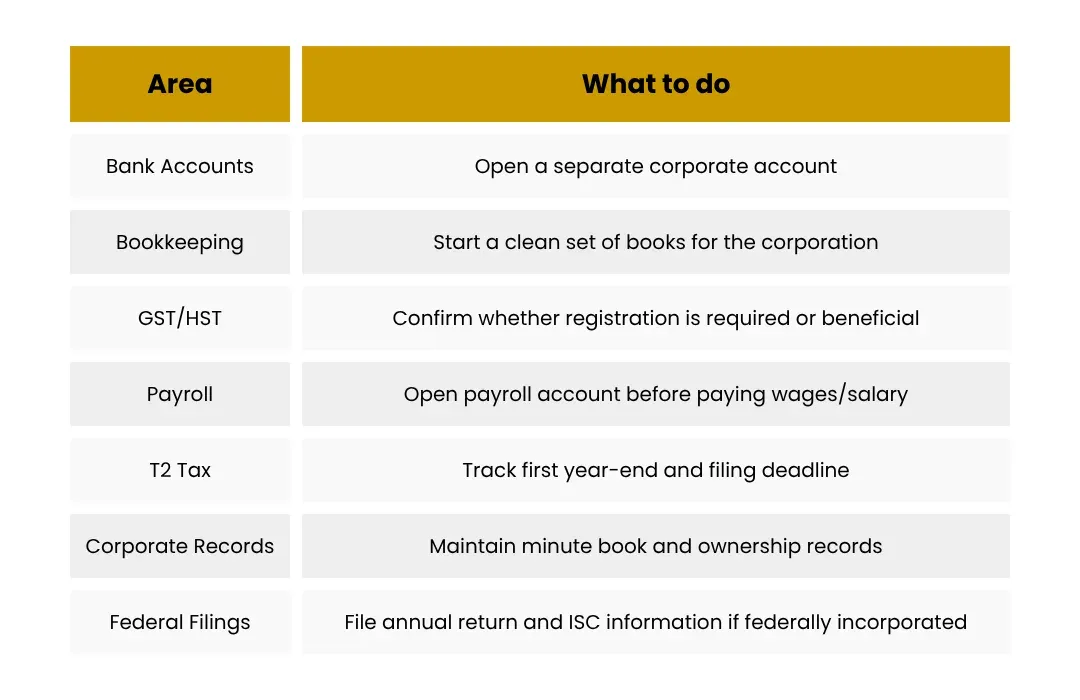

After incorporation, the biggest mindset shift is simple: this is now a separate business entity.

That means your bookkeeping should also become separate. New bank account. New chart of accounts. New expense coding. New support for shareholder contributions, dividends, payroll, and reimbursable expenses. If the old partnership books continue to blur into the new corporation, year-end becomes messy very quickly.

CRA obligations also change. If you need to charge GST/HST, you may need a GST/HST account. If you become an employer or start paying salary, you may need a payroll deductions account. CRA states that you generally need to register for GST/HST once you stop being a small supplier, which usually happens when taxable revenues exceed $30,000, and registration must generally be completed within 29 days of the effective date.

If you are federally incorporated, there is also a corporate maintenance piece that many owners miss: federal business corporations must file an annual return and ISC information every year, generally within 60 days of the incorporation anniversary date.

Post-Incorporation Compliance Checklist

Common Mistakes to Avoid

1. Transferring assets without documenting the transfer

This is one of the biggest errors. If assets move into the company with no valuation, no agreement, and no tax review, problems appear later.

2. Missing the first T2 deadline

CRA does not care that the corporation is new, tiny, or not yet profitable. If it has to file, it has to file.

3. Mixing personal and corporate spending

This creates bookkeeping confusion and weakens the clean separation you were trying to create in the first place.

4. Assuming incorporation automatically handles GST/HST or payroll

Sometimes registrations are streamlined through the incorporation process, but not every account is automatic in every situation. Someone still needs to confirm what is open and what is not.

5. Treating a partnership-to-corporation move as just a legal filing

It is not. It is a legal, tax, and accounting transition all at once.

When to Hire a Professional Accountant

You do not always need a large advisory team to incorporate. But you usually should bring in an accountant when:

- the business already owns assets

- the move is happening mid-year

- there are multiple partners or shareholders

- a holding company is involved

- you are unsure whether to pay salary, dividends, or both

- you want the first T2, GST/HST, and bookkeeping systems set up correctly from day one

This is where a good accountant saves more than tax. They save cleanup time, missed deadlines, and expensive backtracking.

Orbit’s advantage here is practical: not just helping you incorporate, but helping you land the transition properly. That means looking at the rollover issue, the first corporate year-end, the post-incorporation books, and the CRA accounts together instead of in isolation.

Final Thoughts

Incorporating a business in Canada can be a smart move. But the real value is not in the certificate alone. It is in setting up the new corporation correctly so the legal structure, tax filings, and day-to-day finance all line up.

That is especially true when you are moving from partnership to corporation. The risk is not usually that owners fail to incorporate. It is that they incorporate halfway, assume the rest will sort itself out, and only discover the gaps when tax season arrives.

FAQs

Is incorporating a business in Canada always better than staying a partnership?

Not always. It depends on profit levels, liability exposure, growth plans, ownership structure, and compliance tolerance. Incorporation usually gives more structure and flexibility, but it also brings more filings and administration.

Can I transfer business assets into the corporation without triggering tax right away?

Sometimes. A Section 85 rollover may allow eligible property to be transferred to a taxable Canadian corporation on a tax-deferred basis if the rules are met and the election is filed properly.

When is the first T2 return due?

Generally, the corporation’s T2 return is due within six months after its fiscal year-end. The balance of tax is generally due two months after year-end, with a longer balance-due period available for some CCPCs that meet specific conditions.

Do I need new CRA accounts after incorporation?

Often, yes. Depending on your activity, you may need or want separate program accounts such as GST/HST and payroll, in addition to the corporation income tax account.

What if I incorporated federally?

Federal corporations generally have ongoing annual return and ISC filing obligations with Corporations Canada, separate from CRA tax filings.