HoldCo Donations: A Smarter Way to Give

Corporate giving isn’t just about generosity — it’s smart tax strategy. For Canadian business owners who hold investments inside a holding company (HoldCo), donating publicly traded securities in kind instead of cash can unlock major tax efficiencies.

After the June 25, 2024 federal budget increased the corporate capital gains inclusion rate to two-thirds, the math behind charitable giving changed. Donating securities directly (rather than selling first and donating cash) often creates a bigger corporate deduction, avoids capital gains tax, and boosts your Capital Dividend Account (CDA) — paving the way for future tax-free dividends.

Let’s unpack how this works, why it’s so powerful, and how business owners across Canada are using it as part of their CCPC tax planning and estate strategy.

Understanding Corporate Giving in Canada

Corporate giving refers to when a business or holding company donates to a registered charity or donor-advised fund (DAF). Unlike personal donations, corporate giving provides a deduction against taxable income, rather than a non-refundable tax credit.

That deduction reduces the company’s taxable income, leading to direct tax savings. For business owners holding investment portfolios or real estate inside their corporations, giving through HoldCo can be a flexible way to support causes while managing tax exposure.

Would strategic financial oversight from a Fractional CFO add value to your operations?

Why Donate Publicly Traded Securities “In Kind”?

“In kind” means transferring the shares or securities directly to the charity instead of selling them first.

When you sell first, you trigger a taxable capital gain on the increase between the adjusted cost base (ACB) and fair market value (FMV). But when you donate in kind, that gain is fully exempt from tax under the Income Tax Act, provided the recipient is a registered charity.

So, your corporation:

- Gets a donation receipt equal to FMV,

- Pays no capital gains tax, and

- Adds the full capital gain amount to its CDA, which can later be paid out as a tax-free dividend to shareholders.

That’s three layers of benefit — donation deduction, tax-free gain, and future tax-free payout.

The Role of Your Holding Company (HoldCo)

Many Canadian business owners keep investments in a CCPC (Canadian-Controlled Private Corporation) holding company for asset protection and reinvestment.

A HoldCo often owns a portfolio of marketable securities, like mutual funds or ETFs. Over time, those securities appreciate, creating latent capital gains. If sold, two-thirds of the gain is now taxable as of mid-2024.

By donating those securities directly, your HoldCo avoids that taxable event while supporting causes you care about. This strategy can also rebalance portfolios without selling positions — for instance, donating outperforming shares instead of realizing gains.

The 2024 Capital Gains Change and What It Means

Before June 2024, only 50% of a capital gain was taxable. The change raised that to two-thirds (66.67%) for corporations.

That means if your HoldCo realizes a $100,000 gain, the taxable portion jumped from $50,000 to $66,667. At a corporate tax rate of ~50%, that’s an extra $8,333 of tax on the same sale.

Hence, corporate philanthropy through in-kind donations became even more attractive. It’s not just about generosity anymore — it’s a sophisticated tax efficiency move.

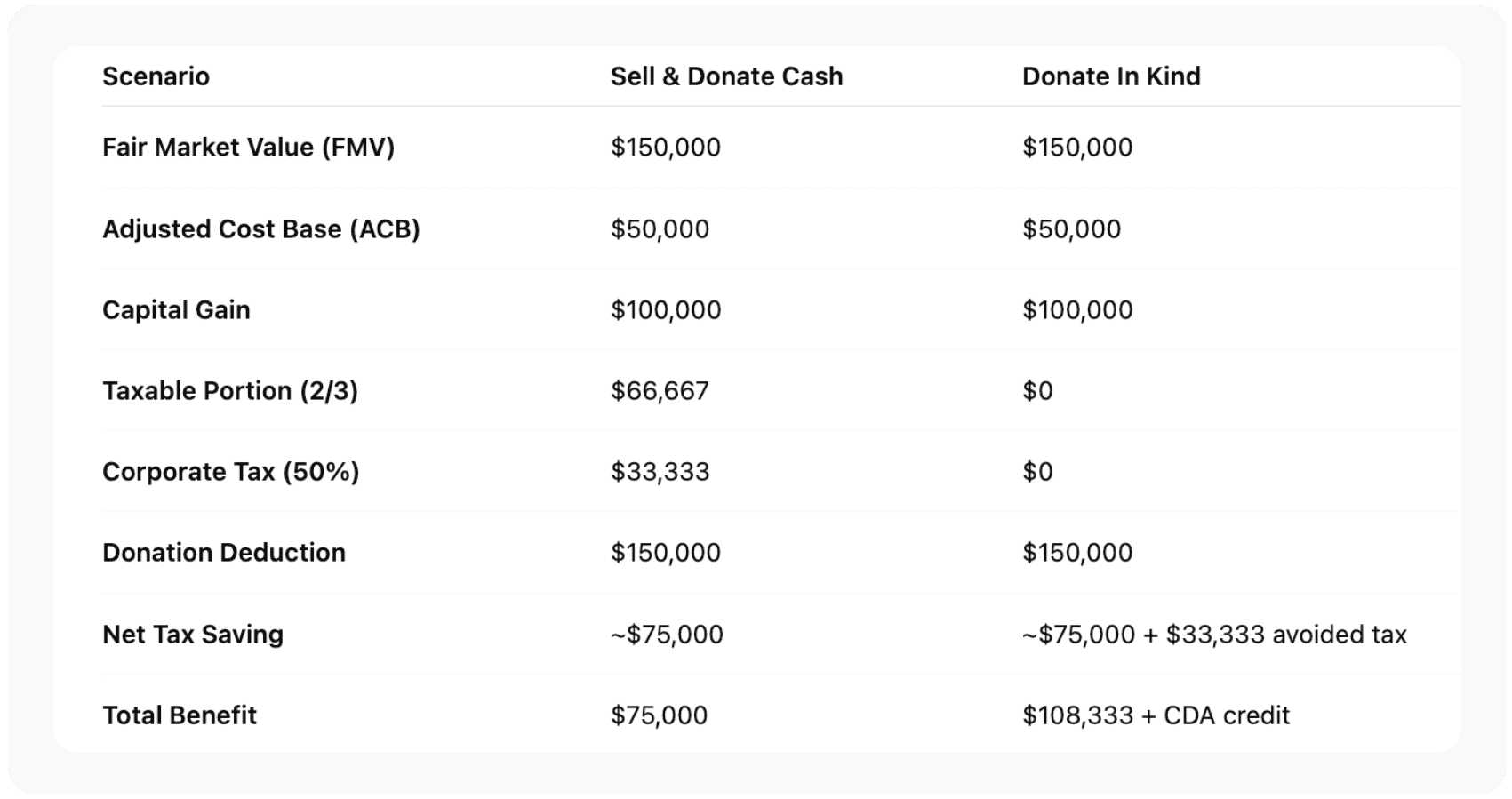

Example: Donating $150,000 in Shares — Cash vs. In-Kind

Let’s look at a practical example. Suppose your HoldCo owns publicly traded shares with a fair market value (FMV) of $150,000 and an adjusted cost base (ACB) of $50,000.

By donating in kind, your HoldCo avoids the $33,333 tax hit, earns the same donation deduction, and credits $100,000 to its Capital Dividend Account — allowing you to pay yourself $100,000 tax-free later.

How the Capital Dividend Account (CDA) Grows Tax-Free

The CDA is a notional account within a private corporation that tracks amounts that can be paid out tax-free to Canadian resident shareholders.

When you donate securities in kind, the non-taxable portion of the gain gets added to the CDA. That credit can then fund tax-free dividends, often to the owner or family members in the same common law partnership or estate plan.

It’s a powerful wealth extraction tool, especially when combined with portfolio rebalancing and charitable intent.

Using Donor-Advised Funds for Simpler Giving

Many business owners prefer to use a donor-advised fund (DAF) instead of donating directly to multiple charities.

A DAF acts like a charitable investment account:

- You donate securities (and get the donation receipt right away).

- The fund liquidates them tax-free.

- You can distribute grants to registered charities later — at your own pace.

This setup simplifies recordkeeping, supports estate planning, and lets you give more strategically over time.

When Corporate Giving Aligns with Estate Planning

Corporate giving can fit naturally into broader estate planning and succession goals.

By donating appreciated securities before a deemed disposition (like death or a sale of the corporation), you reduce both corporate tax liability and future estate tax exposure.

This can be especially useful for:

Common Pitfalls and Valuation Tips

Even though this strategy is powerful, it needs proper documentation.

✅ Fair Market Value (FMV) — must be determined on the donation date, not the settlement date.

✅ Donation Receipt — ensure it lists the FMV and the date of transfer.

✅ Eligible Charities — verify they’re registered with the Canada Revenue Agency (CRA).

✅ Valuation Reduction — avoid overvaluing thinly traded shares; CRA may adjust FMV if inflated.

✅ Timing — securities must be transferred before year-end for the deduction to apply.

Working with your financial advisor and accounting team ensures the tax benefits are preserved under the Income Tax Act.

Key Takeaways

- Donating publicly traded securities from your HoldCo can significantly improve tax efficiency.

- The June 2024 inclusion rate change made this strategy even more valuable.

- You get a corporate deduction, avoid tax on capital gains, and increase your CDA credit.

- Using a donor-advised fund streamlines the process and allows ongoing grants.

- Always confirm FMV, timing, and documentation for CRA compliance.

Frequently Asked Questions

1. Can my operating company donate shares, or must it be from my HoldCo?

Both can, but a HoldCo is usually better since it holds investments rather than active business assets, simplifying reporting and maximizing deductions.

2. Is there a limit to how much my corporation can donate?

Yes. Corporate donations are generally deductible up to 75% of net income for the year. Unused amounts can carry forward for five years.

3. Do I need to sell the shares first?

No. In-kind transfers directly to a registered charity or DAF eliminate the capital gains tax and maximize your CDA credit.

4. How do I prove the fair market value of my donation?

Use your brokerage’s valuation on the transfer date and retain documentation for CRA verification.

5. What if I donate to a foreign charity?

Only donations to Canadian registered charities qualify for the corporate deduction and capital gains exemption.

Legal Disclaimer

This article is provided by Orbit Accountants for general information only and does not constitute accounting, tax, or legal advice. Tax rules can vary by province and change over time. Always consult a qualified Canadian tax professional before making financial or charitable decisions. Reading this content does not create a client relationship with Orbit Accountants. Orbit helps Canadian business owners navigate charitable giving, corporate tax planning, and bookkeeping — so you can give confidently while keeping your numbers optimized.