Table of Contents

What is the Corporate Tax Rate in Canada?

In Canada, businesses pay corporate income tax on their taxable income. The tax rates applied consist of a federal component and a provincial or territorial component. For 2024, the base federal corporate tax rate remains at 15%, but this can be reduced for eligible small businesses.

The amount of tax your business owes depends heavily on where it’s incorporated and whether it qualifies for the Small Business Deduction (SBD). These decisions influence how the tax administration is handled—especially regarding filings, deadlines, and available credits. Staying informed on rate updates and deduction eligibility is key to maintaining compliance and reducing your tax burden.

Federal vs. Provincial Business Tax Rates

The federal government applies a flat corporate tax rate of 15%. Each province or territory then tacks on its own rate, creating a blended tax rate structure. These provincial and territorial taxes vary widely and can significantly affect your bottom line.

Here’s how it works:

- A regular corporation in Ontario might pay 15% (federal) + 11.5% (provincial) = 26.5% total.

- A qualifying small business may pay as little as 12.2% (after SBD).

Monitoring both federal changes and provincial and territorial taxes is critical. A shift in either can push your business into a higher tax bracket and increase your amount of tax owed year over year.

Are you confident your business tax filings are fully optimized and compliant?

Corporate Tax Rate in Ontario (2024)

Ontario’s general corporate tax rate remains 11.5% in 2024. However, for Canadian Controlled Private Corporations (CCPCs) under the $500,000 income threshold, the provincial rate is reduced to 3.2%.

Combined with the federal small business rate of 9%, the effective rate for these businesses is 12.2%. That said, if your income climbs and you lose SBD eligibility, you may move into a higher rate, significantly raising your amount of tax.

Ontario also offers credits for R&D, hiring, and energy investments. Factoring in these programs—alongside other provincial and territorial taxes—can yield long-term savings and streamline your tax administration.

CCPCs and the Small Business Deduction

CCPCs—private companies incorporated and controlled by Canadian residents—benefit from:

- A federal tax rate reduction from 15% to 9% on the first $500,000 of income.

- Reduced provincial and territorial taxes in most regions.

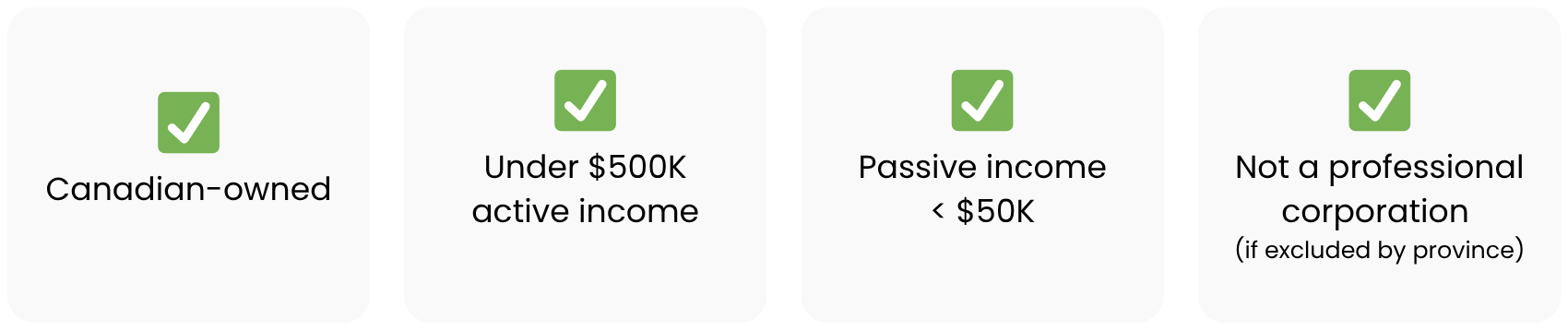

To qualify, a business must:

- Remain a CCPC for the full tax year

- Keep passive investment income below $50,000

- Operate as an active business

Failing to meet these can push income into a higher tax bracket or disqualify you from the lower SBD tax rates applied.

| Type of Business | Federal Rate | Ontario Rate | Combined Rate |

|---|---|---|---|

| CCPC (SBD) | 9% | 3.2% | 12.2% |

| General Corporation | 15% | 11.5% | 26.5% |

Understanding Marginal Tax Brackets

While businesses don’t follow marginal brackets like individuals, a similar effect applies when deductions phase out.

For instance, when a CCPC earns over $50,000 in passive income, access to the SBD is reduced. That means the tax rates applied to your income jump—effectively pushing you into a higher tax bracket.

This can trigger a spike in the amount of tax owed, especially when combined with investment income surcharges and integration rules. Strategic planning, like shifting investment assets to another corporation, can help businesses avoid jumping to a higher rate unnecessarily.

How to Calculate Your Corporate Tax Liability

Follow these steps:

Step 1: Calculate Net Taxable Income

Revenue − Allowable Expenses − Deductions = Net Income

Step 2: Determine eligibility for SBD

Step 3: Apply the relevant tax rates applied:

- 12.2% for CCPCs under $500K (Ontario)

- 26.5% for general corporations

Step 4: Multiply net income by applicable rate = Amount of tax owed

Tools & Graphics: Federal + Ontario Rate Table

| Income Type | Federal Rate | Ontario Rate | Combined |

|---|---|---|---|

| General Active Business | 15% | 11.5% | 26.5% |

| Small Business (CCPC) | 9% | 3.2% | 12.2% |

| Investment Income (CCPC) | 38.7% | Varies | ~50% |

This table helps clarify the tax rates applied to each income type, allowing you to estimate your amount of tax more accurately.

Key Tips to Minimize Business Taxes

- Split income among lower-income family members (within legal limits)

- Keep passive income under $50,000 to preserve SBD

- Maximize eligible deductions (salaries, rent, legal fees)

- Use a corporate tax calculator to simulate different scenarios

- Consider how salary vs dividend impacts your tax administration

Frequently Asked Questions

What is Canada’s corporate tax rate in 2024?

15% federally. The combined rate depends on provincial and territorial taxes.

What’s the corporate tax rate in Ontario for 2024?

11.5% for general corporations, 3.2% for CCPCs under $500K.

What is PTY tax?

Generally an Australian term. In Canada, confirm with a tax advisor.

Are capital gains taxed differently in corporations?

Yes. Only 50% is taxable, and the rest may be paid as tax-free capital dividends.

Do tax brackets apply to corporations?

Not directly, but deduction phase-outs create higher tax bracket effects.

Conclusion

Canada’s corporate tax system may seem straightforward on paper, but the real-world tax administration requires attention to detail. Knowing your eligibility for credits, how tax rates are applied, and how to manage provincial and territorial taxes can go a long way in minimizing your amount of tax.

✅ Tip: Work with a professional accountant to avoid being pushed into a higher rate or missing out on deductions that keep you in a lower bracket.

Legal Disclaimer: This post is for informational purposes only and does not constitute tax or legal advice. Always consult a licensed professional for advice tailored to your business.